Scalper1 News

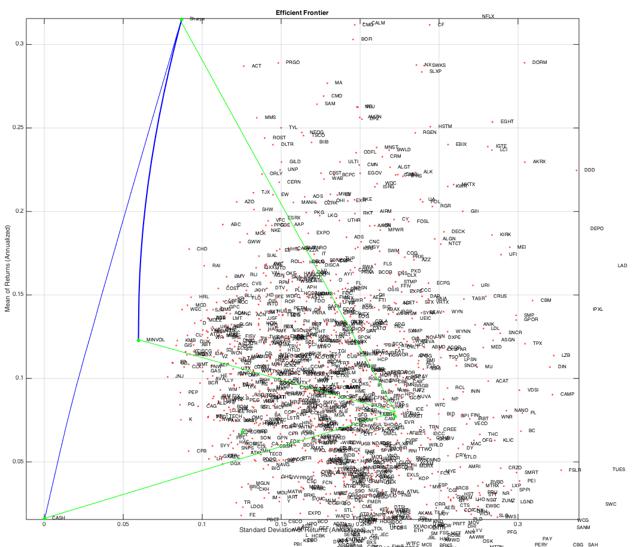

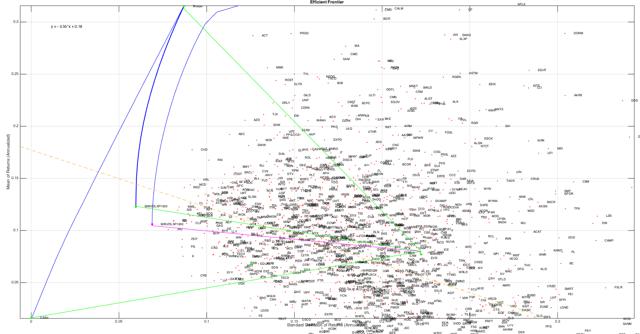

Summary Minimum volatility strategies have outperformed in the U.S. markets. A minimum volatility portfolio may make a good “skeleton” for a concentrated equity allocation. USMV appears to be a good implementation of the strategy. In my last article , we looked at several types of portfolios for U.S. domestic equity. We saw that broad-based static allocations limit alpha , and tend to track the wider market in terms of returns. Nevertheless, we did see that momentum-value, minimum variance, as well as stock-based portfolio with slack had an edge over the market portfolio (as proxied by the Vanguard Total Stock Market ETF (NYSEARCA: VTI )) in terms of returns, inverse beta, drawdown, and mean-variance efficiency. The minimum variance strategy, as proxied by the iShares MSCI USA Minimum Volatility ETF (NYSEARCA: USMV ), scored especially well. We also saw how some allocation slack in the concentrated stock portfolio allows investors to potentially capture some alpha . In this article, we expand on the minimum variance strategy within the context of U.S. domestic equity, but extend the strategy to small-cap stocks in a more concentrated stock portfolio, which should be more conducive to generating potential alpha whilst maintaining some of the structure of a quantitative strategy. Data and Methods The S&P 1500 stocks were assembled from State Street’s SPDR S&P 500 Trust (NYSEARCA: SPY ), SPDR S&P MidCap 400 Trust (NYSEARCA: MDY ), SPDR S&P 600 Small Cap (NYSEARCA: SLY ) ETFs holdings disclosures. The S&P 1500 was chosen because it’s both familiar and covers most of the market; it also weeds out many less investable parts of the market by using liquidity, float, and financial considerations. The price and return data then were obtained from the data facility of Yahoo! Finance. Only stocks with about 7.5 years of history were retained so as to include the financial crisis in 2008. This full sample requirement was to make the estimates more comparable, and left 1348 equities. The market benchmark portfolio, as proxied by VTI, was calculated for the same period, along with the ETF implementation of the strategy, USMV. The continuous logged total returns for the portfolios are computed from their split and volume-adjusted prices using the quantmod package for R . The dividends are accrued daily over the observed period. The daily return and standard deviation statistics are then made monthly using 21 trading days. The 1-year forward earnings estimates stem from Thomson Reuters fundamentals; a few missing estimates were complemented with either numbers from Yahoo or last year’s earnings. The real risk-free rate is assumed to be 1.62% comparable to some margin rates offered. The data were then imported into MATLAB in order to use the well-documented financial toolbox (The same exercise is possible in R, just much less comfortable). The minimum-variance portfolio from the sample is then computed using quadratic programming, no short-selling, no leverage, and constrained to ensure that no fewer than 10 stocks are chosen. Figure 1 gives an overview of both the assets and the minimum variance portfolio, visible in green at the nadir of the blue radial curve. Green lines emanate from the market portfolio, VTI, to the risk-free rate, minimum variance, and the mean-variance efficient portfolios. (click to enlarge) Figure 1: Risk vs. Return Efficiency Frontier for S&P 1500 Figure 1 reveals that the minimum variance portfolio has vastly outperformed the market in the last 8 years as evidenced by the upward sloping angle that connects its risk/return with that of the market portfolio in the swarm of assets. One might expect that the performance ought to be below that of the market return and above that of the risk-free rate, i.e. somewhere near the lower line segment that connects the risk-free rate with the market return where the equal weighted portfolio now lies (green point). I’m not versed in the financial literature on volatility, but I am skeptical whether such outperformance can continue – my pet theory is that the phenomenon is attributable to an uncompetitive bond market. Central banks have artificially lowered the discount rate by about half since the beginning of this sample period. This would approximately double the discounted present value of the company even with static earnings. Since the market return of 8.4% is essentially in line with historical averages (7-10% depending on the period and methods), I thus also suspect the momentum has drawn in participants from the other more volatile segments of the market. Beyond my empirical musings, many of you are most likely interested in the component stocks. Table 1 compares the holdings of the solution with those of the USMV. Note that the weights do not quite tally to 100% as many of the miniscule positions (i.e. < 0.5%) were omitted. Table 1 shows the weights of the solution compared with the USMV ETF. Table 1: Large/mid-Cap Minimum Volatility Portfolio (S&P1500) Symbol Company Index Index Weight Sector MinVolSP1500 Weights USMV Weights Ratio of Portfolio Weights FW Earnings Yield JNJ Johnson & Johnson SP500 1.62% Health Care 5.1% 1.4% 3.63 5.8% PEP PepsiCo Inc. SP500 0.79% Consumer Staples 2.8% 1.4% 1.97 5.0% WMT Wal-Mart Stores Inc. SP500 0.76% Consumer Staples 5.3% 1.5% 3.47 5.9% MO Altria Group Inc. SP500 0.54% Consumer Staples 2.0% 0.8% 2.51 5.5% MCD McDonald's Corporation SP500 0.50% Consumer Discretionary 5.2% 1.4% 3.64 5.8% SO Southern Company SP500 0.25% Utilities 10.0% 1.4% 7.30 6.0% GIS General Mills Inc. SP500 0.18% Consumer Staples 10.0% 1.3% 7.67 5.2% BDX Becton Dickinson and Company SP500 0.15% Health Care 1.8% 1.6% 1.11 4.8% ED Consolidated Edison Inc. SP500 0.11% Utilities 6.9% 1.3% 5.45 6.0% CAG ConAgra Foods Inc. SP500 0.08% Consumer Staples 5.5% 0.0% - 6.3% DLTR Dollar Tree Inc. SP500 0.08% Consumer Discretionary 0.9% 0.2% 3.83 4.5% BCR C. R. Bard Inc. SP500 0.07% Health Care 3.2% 0.7% 4.81 5.4% CLX Clorox Company SP500 0.07% Consumer Staples 8.5% 0.3% 25.13 4.3% LH Laboratory Corporation of America Holdings SP500 0.05% Health Care 1.4% 0.5% 2.61 6.8% CPB Campbell Soup Company SP500 0.04% Consumer Staples 1.9% 0.3% 7.73 5.5% HRL Hormel Foods Corporation SP500 0.04% Consumer Staples 8.6% 0.3% 29.85 4.8% CHD Church & Dwight Co. Inc. SP400 0.65% Consumer Staples 5.4% 0.6% 8.59 4.2% AJG Arthur J. Gallagher & Co. SP400 0.47% Financials 1.7% 0.0% - 5.9% RGLD Royal Gold Inc. SP400 0.27% Materials 3.0% 0.0% - 2.0% TECH Bio-Techne Corporation SP400 0.21% Health Care 0.9% 0.0% - 4.2% LDOS Leidos Holdings Inc. SP400 0.16% Information Technology 1.5% 0.0% - 5.9% FCN FTI Consulting Inc. SP400 0.10% Industrials 1.9% 0.0% - 5.3% BOFI BofI HOLDING INC. SP600 0.15% Financials 2.8% - - 6.1% HSTM HealthStream Inc. SP600 0.09% Health Care 1.1% - - 1.5% SENEA Seneca Foods Corporation Class A SP600 0.03% Consumer Staples 1.8% - - 4.7% Expected Earnings Yield: 5.2% As expected, the resultant portfolio has many of the same members as USMV. It is, however, much more focused than USMV, which operates under several other sector and weight constraints. Nevertheless, this tighter collection of stocks would be more manageable for an individual investor's portfolio. The stocks are not exactly cheap trading at 19.23x forward earnings vs. about 14.67 historical average for the S&P 500. Including the small-caps does reveal some interesting small-caps like Leidos, which is a specialized IT outfit with government contracts, or Royal Gold, which owns a variety of stakes in precious metals. The latter has an interesting business model that assembles cash-flow stakes in precious metal interests, but is not exposed to the operational risk like a miner would be. In this sense, the minimum volatility portfolio solution might help to identify unique stocks that might otherwise pass through a standard stock screen. I suspect that many of you may already have either large-cap funds or stocks within your portfolio, so I performed the same exercise by looking at just the S&P 1000, which would complement those putative holdings. Figure 2 reveals that limiting the equity space reduces the efficiency of the portfolio as evidenced by the frontier shifting right in the (horizontal) risk space, and down in the (vertical) return space. The magenta line connects the moments of the S&P 1000 volatility portfolio to those of the market portfolio. The orange dotted line is a regression of risk, as measured by the annualized standard deviation of returns, versus annualized total returns; the negative slope counter-intuitively is telling us that more risk equates to fewer returns in the recent equity market. (click to enlarge) Figure 2: Minimum Volatility Portfolios and Risk versus Return Table 2 displays the weights and holdings of that minimum variance portfolio, we see a fair amount of overlap in the portfolios with health care, staples, and utilities playing a large role. Interestingly, we see a few more of the pro-cyclical industrials, financials, and technology firms represented. As prime example, Synopsys is a small engineering and development outfit that looks like an interesting, reasonably priced tech-play if U.S. capital expenditures pick up. Table 2: Mid/Small-cap Minimum Volatility Portfolio (S&P1000) Symbol Company Index Index Weight Sector MinVolSP1000 Weights FW Earnings Yield CHD Church & Dwight Co. Inc. SP400 0.65% Consumer Staples 10.00% 4.2% AJG Arthur J. Gallagher & Co. SP400 0.47% Financials 7.55% 5.9% SNPS Synopsys Inc. SP400 0.41% Information Technology 2.01% 6.2% UTHR United Therapeutics Corporation SP400 0.37% Health Care 1.41% 6.9% ATO Atmos Energy Corporation SP400 0.34% Utilities 4.34% 5.5% WCN Waste Connections Inc. SP400 0.34% Industrials 1.46% 4.6% GXP Great Plains Energy Incorporated SP400 0.27% Utilities 2.85% 6.2% RGLD Royal Gold Inc. SP400 0.27% Materials 4.33% 2.0% CPRT Copart Inc. SP400 0.26% Industrials 0.56% 4.7% ATK Alliant Techsystems Inc. SP400 0.23% Industrials 2.00% 10.4% RNR RenaissanceRe Holdings Ltd. SP400 0.23% Financials 3.50% 8.8% VVC Vectren Corporation SP400 0.23% Utilities 0.54% 5.5% FLO Flowers Foods Inc. SP400 0.22% Consumer Staples 5.90% 5.1% THS TreeHouse Foods Inc. SP400 0.22% Consumer Staples 6.35% 5.1% TECH Bio-Techne Corporation SP400 0.21% Health Care 8.57% 4.2% HE Hawaiian Electric Industries Inc. SP400 0.21% Utilities 10.00% 5.1% LDOS Leidos Holdings Inc. SP400 0.16% Information Technology 6.52% 5.9% FCN FTI Consulting Inc. SP400 0.10% Industrials 3.00% 5.3% HAE Haemonetics Corporation SP600 0.28% Health Care 4.81% 4.9% MGLN Magellan Health Inc. SP600 0.24% Health Care 2.20% 3.9% ICUI ICU Medical Inc. SP600 0.16% Health Care 0.79% 3.3% BOFI BofI HOLDING INC. SP600 0.15% Financials 3.68% 6.1% HSTM HealthStream Inc. SP600 0.09% Health Care 0.91% 1.5% ANIK Anika Therapeutics Inc. SP600 0.08% Health Care 0.80% 3.9% SENEA Seneca Foods Corporation Class A SP600 0.03% Consumer Staples 3.23% 4.7% Expected Earnings Yield: 5.03% Having seen the content of the portfolios, we now compare their performance attributes. Portfolios are evaluated using: annualized returns, Sharpe ratio (return efficiency), Calmar ratio (drawdown efficiency), and inverse beta (systemic risk). These four statistics are then computed relative to the market portfolio, and their geometric mean is taken to arrive at a general score (last column). Table 3 reports the results. Table 3: Portfolios Compared PORTFOLIO* DATA (years) Portfolio Stats Benchmark Relative Stats (stat_portfolio/stat_benchmark) R SD Sharpe Calmar Beta R SD Sharpe Calmar R Sharpe Calmar Beta^-1 Score MinVolSP1500 7.4 14.4% 13% 1.141 0.353 0.648 8.4% 22.3% 0.38 0.11 1.72 3.03 3.30 1.54 2.27 MinVolSP1000 7.4 11.0% 14% 0.757 0.353 0.648 8.2% 22.0% 0.37 0.11 1.35 2.04 3.30 1.54 1.93 MinVolSP900 7.4 16.7% 13% 1.312 0.353 0.648 8.1% 21.9% 0.37 0.17 2.06 3.55 2.08 1.54 2.20 Mid-Cap 8.0 9.7% 25% 0.394 0.119 1.076 8.4% 22.2% 0.38 0.11 1.17 1.05 1.06 0.93 1.05 Market 8.0 8.4% 22% 0.376 0.113 1 8.4% 22.2% 0.38 0.11 1.00 1.00 1.00 1.00 1.00 S&P500 8.0 7.9% 22% 0.358 0.106 0.989 8.4% 22.2% 0.38 0.11 0.95 0.95 0.95 1.01 0.96 Dividend 8.0 8.4% 24% 0.348 0.104 1.041 8.4% 22.2% 0.38 0.11 1.01 0.93 0.92 0.96 0.95 Sectors 8.0 8.1% 23% 0.353 0.104 1.014 8.4% 22.2% 0.38 0.11 0.96 0.94 0.92 0.99 0.95 Market Cap 8.0 8.4% 24% 0.345 0.099 1.079 8.4% 22.2% 0.38 0.11 1.01 0.92 0.88 0.93 0.93 "Cramer" 8.0 8.5% 26% 0.325 0.096 1.073 8.4% 22.2% 0.38 0.11 1.02 0.86 0.85 0.93 0.91 Random Stock 7.2 1%^ 32% 0.032 -0.036 1.25 8.2% 23.0% 0.36 0.11 0.13 0.09 -0.33 0.8 NaN^ *The other portfolios are explained in my previous article . ^Due to the slight difference in how returns are calculated between the method outlined and the Calmar ratio in the performance analytics package for R, an imaginary solution is produced when the geometric mean is taken. We see that the annualized returns of the minimum variance portfolios have dominated the other domestic portfolio strategies in recent years, not only with double digit returns, but they also score much better in terms of risk-efficiency as measured by the Sharpe and Calmar ratios. Furthermore, the portfolios exhibit considerably less systematic risk as measured by beta , which implies they could be significantly leveraged to reach even higher returns without taking more aggregate systemic risk than the other portfolios. We now compare the focused do-it-yourself portfolio to the benchmark ETF USMV over a common period. Table 4: Portfolios vs. USMV Parent Index S&P 1500 S&P 900 S&P 1000 Period (years) 2.644 2.644 2.644 Portfolio Stats R 0.177 0.167 0.11 SD 0.127 0.127 0.145 Sharpe 1.396 1.312 0.757 Calmar 0.353 0.353 0.353 Beta 1.025 1.025 1.025 Benchmark R 0.191 0.191 0.191 SD 0.097 0.097 0.097 Sharpe 1.982 1.982 1.982 Calmar 3.074 3.074 3.074 Relative Stats (port/bench) R 0.923 0.873 0.574 Sharpe 0.704 0.662 0.382 Calmar 0.115 0.115 0.115 Beta^-1 0.976 0.976 0.976 Score 0.519 0.504 0.396 A bit to my own surprise, we see that USMV outperformed the other minimum variance stock portfolios. I would have thought the S&P 1500 and S&P 1000 portfolios would outperform in that the former incorporates more equities, and the latter is optimized on a class of equities, which have traditionally exhibited larger risk premia. Even optimized on a similar large and mid-cap space, USMV outperforms. Moreover, USMV has more constraints on its portfolio construction, such as turnover restrictions or an upper bound of 1.5% on any given asset. Furthermore, it has an expense ratio. It does have three advantages that spring to mind. The first is that it dynamically adjusts every 6 months, whereas the results presented here are computed as an ab initio allocation held for the entire period. The second is that as money pours into the strategy, the stocks in the ETF rise in the price - since the holdings are somewhat distinct, this might give the ETF an edge as money flows into it (but this also may run in the other direction…). Third, is the fact that the index providers may have a bit of secret sauce for how the index is constructed - this is not to say they are hiding something, merely that they may know what constraints provide a slight edge over my "dumb" optimization. That is to say, some smart quant on MSCI's index team may have a keen, but undisclosed, rationale for why no stock may be more than 20x the allocation in its parent index provides a slight edge. In this article, we have seen that minimum volatility strategies have outperformed in the recent period, but that both on a fundamental and theoretical level, this outperformance may be transitory. Nevertheless, the strategy does have some conceptual merit, and might be a good initial skeleton for retail investors who are known to choose riskier higher beta and smaller cap stocks. Beyond a basic industry diversification, retail investors are unlikely to be in a position to exploit the covariance amongst the assets. Some of these correlations are not immediately obvious - for example, my miner, Vale (NYSE: VALE ), is linked to my utility by virtue of the fact that they are both Brazilian. My Australian stocks seem subservient to the whims of Chinese GDP reports, and my gold miner tracks my iron stock. In short, unless you have done the work ahead of time it is fairly easy to inadvertently put together a very volatile portfolio that looks on paper to be very diversified, but trades very wonky. As we saw in Figures 1 and 2, the advantage of the minimum volatility approach is that it at least should keep your equity portfolio somewhere in the triangle between the risk-free-rate, risk-optimal return, and the market portfolio; staying out of the dangerous southern hemisphere and wild eastern reaches of the risk-return chart should prevent your portfolio from getting totally wracked on the low-return high-variance shoals of the equity markets. If you are less-risk averse and do not want to use margin, the strategy at least leaves you with some risk-budget to squander, err.., "deploy" on high-octane biotechs or Internet IPOs. For those who do not seek the venerated alpha or who do not want to do-it-yourself, USMV looks like a good implementation of the allocation strategy where its expense ratio vs. VTI might be just good value, rather than a wealth-destroying violation of the Bogleheads' sacred low-fee doctrine. Scalper1 News

Summary Minimum volatility strategies have outperformed in the U.S. markets. A minimum volatility portfolio may make a good “skeleton” for a concentrated equity allocation. USMV appears to be a good implementation of the strategy. In my last article , we looked at several types of portfolios for U.S. domestic equity. We saw that broad-based static allocations limit alpha , and tend to track the wider market in terms of returns. Nevertheless, we did see that momentum-value, minimum variance, as well as stock-based portfolio with slack had an edge over the market portfolio (as proxied by the Vanguard Total Stock Market ETF (NYSEARCA: VTI )) in terms of returns, inverse beta, drawdown, and mean-variance efficiency. The minimum variance strategy, as proxied by the iShares MSCI USA Minimum Volatility ETF (NYSEARCA: USMV ), scored especially well. We also saw how some allocation slack in the concentrated stock portfolio allows investors to potentially capture some alpha . In this article, we expand on the minimum variance strategy within the context of U.S. domestic equity, but extend the strategy to small-cap stocks in a more concentrated stock portfolio, which should be more conducive to generating potential alpha whilst maintaining some of the structure of a quantitative strategy. Data and Methods The S&P 1500 stocks were assembled from State Street’s SPDR S&P 500 Trust (NYSEARCA: SPY ), SPDR S&P MidCap 400 Trust (NYSEARCA: MDY ), SPDR S&P 600 Small Cap (NYSEARCA: SLY ) ETFs holdings disclosures. The S&P 1500 was chosen because it’s both familiar and covers most of the market; it also weeds out many less investable parts of the market by using liquidity, float, and financial considerations. The price and return data then were obtained from the data facility of Yahoo! Finance. Only stocks with about 7.5 years of history were retained so as to include the financial crisis in 2008. This full sample requirement was to make the estimates more comparable, and left 1348 equities. The market benchmark portfolio, as proxied by VTI, was calculated for the same period, along with the ETF implementation of the strategy, USMV. The continuous logged total returns for the portfolios are computed from their split and volume-adjusted prices using the quantmod package for R . The dividends are accrued daily over the observed period. The daily return and standard deviation statistics are then made monthly using 21 trading days. The 1-year forward earnings estimates stem from Thomson Reuters fundamentals; a few missing estimates were complemented with either numbers from Yahoo or last year’s earnings. The real risk-free rate is assumed to be 1.62% comparable to some margin rates offered. The data were then imported into MATLAB in order to use the well-documented financial toolbox (The same exercise is possible in R, just much less comfortable). The minimum-variance portfolio from the sample is then computed using quadratic programming, no short-selling, no leverage, and constrained to ensure that no fewer than 10 stocks are chosen. Figure 1 gives an overview of both the assets and the minimum variance portfolio, visible in green at the nadir of the blue radial curve. Green lines emanate from the market portfolio, VTI, to the risk-free rate, minimum variance, and the mean-variance efficient portfolios. (click to enlarge) Figure 1: Risk vs. Return Efficiency Frontier for S&P 1500 Figure 1 reveals that the minimum variance portfolio has vastly outperformed the market in the last 8 years as evidenced by the upward sloping angle that connects its risk/return with that of the market portfolio in the swarm of assets. One might expect that the performance ought to be below that of the market return and above that of the risk-free rate, i.e. somewhere near the lower line segment that connects the risk-free rate with the market return where the equal weighted portfolio now lies (green point). I’m not versed in the financial literature on volatility, but I am skeptical whether such outperformance can continue – my pet theory is that the phenomenon is attributable to an uncompetitive bond market. Central banks have artificially lowered the discount rate by about half since the beginning of this sample period. This would approximately double the discounted present value of the company even with static earnings. Since the market return of 8.4% is essentially in line with historical averages (7-10% depending on the period and methods), I thus also suspect the momentum has drawn in participants from the other more volatile segments of the market. Beyond my empirical musings, many of you are most likely interested in the component stocks. Table 1 compares the holdings of the solution with those of the USMV. Note that the weights do not quite tally to 100% as many of the miniscule positions (i.e. < 0.5%) were omitted. Table 1 shows the weights of the solution compared with the USMV ETF. Table 1: Large/mid-Cap Minimum Volatility Portfolio (S&P1500) Symbol Company Index Index Weight Sector MinVolSP1500 Weights USMV Weights Ratio of Portfolio Weights FW Earnings Yield JNJ Johnson & Johnson SP500 1.62% Health Care 5.1% 1.4% 3.63 5.8% PEP PepsiCo Inc. SP500 0.79% Consumer Staples 2.8% 1.4% 1.97 5.0% WMT Wal-Mart Stores Inc. SP500 0.76% Consumer Staples 5.3% 1.5% 3.47 5.9% MO Altria Group Inc. SP500 0.54% Consumer Staples 2.0% 0.8% 2.51 5.5% MCD McDonald's Corporation SP500 0.50% Consumer Discretionary 5.2% 1.4% 3.64 5.8% SO Southern Company SP500 0.25% Utilities 10.0% 1.4% 7.30 6.0% GIS General Mills Inc. SP500 0.18% Consumer Staples 10.0% 1.3% 7.67 5.2% BDX Becton Dickinson and Company SP500 0.15% Health Care 1.8% 1.6% 1.11 4.8% ED Consolidated Edison Inc. SP500 0.11% Utilities 6.9% 1.3% 5.45 6.0% CAG ConAgra Foods Inc. SP500 0.08% Consumer Staples 5.5% 0.0% - 6.3% DLTR Dollar Tree Inc. SP500 0.08% Consumer Discretionary 0.9% 0.2% 3.83 4.5% BCR C. R. Bard Inc. SP500 0.07% Health Care 3.2% 0.7% 4.81 5.4% CLX Clorox Company SP500 0.07% Consumer Staples 8.5% 0.3% 25.13 4.3% LH Laboratory Corporation of America Holdings SP500 0.05% Health Care 1.4% 0.5% 2.61 6.8% CPB Campbell Soup Company SP500 0.04% Consumer Staples 1.9% 0.3% 7.73 5.5% HRL Hormel Foods Corporation SP500 0.04% Consumer Staples 8.6% 0.3% 29.85 4.8% CHD Church & Dwight Co. Inc. SP400 0.65% Consumer Staples 5.4% 0.6% 8.59 4.2% AJG Arthur J. Gallagher & Co. SP400 0.47% Financials 1.7% 0.0% - 5.9% RGLD Royal Gold Inc. SP400 0.27% Materials 3.0% 0.0% - 2.0% TECH Bio-Techne Corporation SP400 0.21% Health Care 0.9% 0.0% - 4.2% LDOS Leidos Holdings Inc. SP400 0.16% Information Technology 1.5% 0.0% - 5.9% FCN FTI Consulting Inc. SP400 0.10% Industrials 1.9% 0.0% - 5.3% BOFI BofI HOLDING INC. SP600 0.15% Financials 2.8% - - 6.1% HSTM HealthStream Inc. SP600 0.09% Health Care 1.1% - - 1.5% SENEA Seneca Foods Corporation Class A SP600 0.03% Consumer Staples 1.8% - - 4.7% Expected Earnings Yield: 5.2% As expected, the resultant portfolio has many of the same members as USMV. It is, however, much more focused than USMV, which operates under several other sector and weight constraints. Nevertheless, this tighter collection of stocks would be more manageable for an individual investor's portfolio. The stocks are not exactly cheap trading at 19.23x forward earnings vs. about 14.67 historical average for the S&P 500. Including the small-caps does reveal some interesting small-caps like Leidos, which is a specialized IT outfit with government contracts, or Royal Gold, which owns a variety of stakes in precious metals. The latter has an interesting business model that assembles cash-flow stakes in precious metal interests, but is not exposed to the operational risk like a miner would be. In this sense, the minimum volatility portfolio solution might help to identify unique stocks that might otherwise pass through a standard stock screen. I suspect that many of you may already have either large-cap funds or stocks within your portfolio, so I performed the same exercise by looking at just the S&P 1000, which would complement those putative holdings. Figure 2 reveals that limiting the equity space reduces the efficiency of the portfolio as evidenced by the frontier shifting right in the (horizontal) risk space, and down in the (vertical) return space. The magenta line connects the moments of the S&P 1000 volatility portfolio to those of the market portfolio. The orange dotted line is a regression of risk, as measured by the annualized standard deviation of returns, versus annualized total returns; the negative slope counter-intuitively is telling us that more risk equates to fewer returns in the recent equity market. (click to enlarge) Figure 2: Minimum Volatility Portfolios and Risk versus Return Table 2 displays the weights and holdings of that minimum variance portfolio, we see a fair amount of overlap in the portfolios with health care, staples, and utilities playing a large role. Interestingly, we see a few more of the pro-cyclical industrials, financials, and technology firms represented. As prime example, Synopsys is a small engineering and development outfit that looks like an interesting, reasonably priced tech-play if U.S. capital expenditures pick up. Table 2: Mid/Small-cap Minimum Volatility Portfolio (S&P1000) Symbol Company Index Index Weight Sector MinVolSP1000 Weights FW Earnings Yield CHD Church & Dwight Co. Inc. SP400 0.65% Consumer Staples 10.00% 4.2% AJG Arthur J. Gallagher & Co. SP400 0.47% Financials 7.55% 5.9% SNPS Synopsys Inc. SP400 0.41% Information Technology 2.01% 6.2% UTHR United Therapeutics Corporation SP400 0.37% Health Care 1.41% 6.9% ATO Atmos Energy Corporation SP400 0.34% Utilities 4.34% 5.5% WCN Waste Connections Inc. SP400 0.34% Industrials 1.46% 4.6% GXP Great Plains Energy Incorporated SP400 0.27% Utilities 2.85% 6.2% RGLD Royal Gold Inc. SP400 0.27% Materials 4.33% 2.0% CPRT Copart Inc. SP400 0.26% Industrials 0.56% 4.7% ATK Alliant Techsystems Inc. SP400 0.23% Industrials 2.00% 10.4% RNR RenaissanceRe Holdings Ltd. SP400 0.23% Financials 3.50% 8.8% VVC Vectren Corporation SP400 0.23% Utilities 0.54% 5.5% FLO Flowers Foods Inc. SP400 0.22% Consumer Staples 5.90% 5.1% THS TreeHouse Foods Inc. SP400 0.22% Consumer Staples 6.35% 5.1% TECH Bio-Techne Corporation SP400 0.21% Health Care 8.57% 4.2% HE Hawaiian Electric Industries Inc. SP400 0.21% Utilities 10.00% 5.1% LDOS Leidos Holdings Inc. SP400 0.16% Information Technology 6.52% 5.9% FCN FTI Consulting Inc. SP400 0.10% Industrials 3.00% 5.3% HAE Haemonetics Corporation SP600 0.28% Health Care 4.81% 4.9% MGLN Magellan Health Inc. SP600 0.24% Health Care 2.20% 3.9% ICUI ICU Medical Inc. SP600 0.16% Health Care 0.79% 3.3% BOFI BofI HOLDING INC. SP600 0.15% Financials 3.68% 6.1% HSTM HealthStream Inc. SP600 0.09% Health Care 0.91% 1.5% ANIK Anika Therapeutics Inc. SP600 0.08% Health Care 0.80% 3.9% SENEA Seneca Foods Corporation Class A SP600 0.03% Consumer Staples 3.23% 4.7% Expected Earnings Yield: 5.03% Having seen the content of the portfolios, we now compare their performance attributes. Portfolios are evaluated using: annualized returns, Sharpe ratio (return efficiency), Calmar ratio (drawdown efficiency), and inverse beta (systemic risk). These four statistics are then computed relative to the market portfolio, and their geometric mean is taken to arrive at a general score (last column). Table 3 reports the results. Table 3: Portfolios Compared PORTFOLIO* DATA (years) Portfolio Stats Benchmark Relative Stats (stat_portfolio/stat_benchmark) R SD Sharpe Calmar Beta R SD Sharpe Calmar R Sharpe Calmar Beta^-1 Score MinVolSP1500 7.4 14.4% 13% 1.141 0.353 0.648 8.4% 22.3% 0.38 0.11 1.72 3.03 3.30 1.54 2.27 MinVolSP1000 7.4 11.0% 14% 0.757 0.353 0.648 8.2% 22.0% 0.37 0.11 1.35 2.04 3.30 1.54 1.93 MinVolSP900 7.4 16.7% 13% 1.312 0.353 0.648 8.1% 21.9% 0.37 0.17 2.06 3.55 2.08 1.54 2.20 Mid-Cap 8.0 9.7% 25% 0.394 0.119 1.076 8.4% 22.2% 0.38 0.11 1.17 1.05 1.06 0.93 1.05 Market 8.0 8.4% 22% 0.376 0.113 1 8.4% 22.2% 0.38 0.11 1.00 1.00 1.00 1.00 1.00 S&P500 8.0 7.9% 22% 0.358 0.106 0.989 8.4% 22.2% 0.38 0.11 0.95 0.95 0.95 1.01 0.96 Dividend 8.0 8.4% 24% 0.348 0.104 1.041 8.4% 22.2% 0.38 0.11 1.01 0.93 0.92 0.96 0.95 Sectors 8.0 8.1% 23% 0.353 0.104 1.014 8.4% 22.2% 0.38 0.11 0.96 0.94 0.92 0.99 0.95 Market Cap 8.0 8.4% 24% 0.345 0.099 1.079 8.4% 22.2% 0.38 0.11 1.01 0.92 0.88 0.93 0.93 "Cramer" 8.0 8.5% 26% 0.325 0.096 1.073 8.4% 22.2% 0.38 0.11 1.02 0.86 0.85 0.93 0.91 Random Stock 7.2 1%^ 32% 0.032 -0.036 1.25 8.2% 23.0% 0.36 0.11 0.13 0.09 -0.33 0.8 NaN^ *The other portfolios are explained in my previous article . ^Due to the slight difference in how returns are calculated between the method outlined and the Calmar ratio in the performance analytics package for R, an imaginary solution is produced when the geometric mean is taken. We see that the annualized returns of the minimum variance portfolios have dominated the other domestic portfolio strategies in recent years, not only with double digit returns, but they also score much better in terms of risk-efficiency as measured by the Sharpe and Calmar ratios. Furthermore, the portfolios exhibit considerably less systematic risk as measured by beta , which implies they could be significantly leveraged to reach even higher returns without taking more aggregate systemic risk than the other portfolios. We now compare the focused do-it-yourself portfolio to the benchmark ETF USMV over a common period. Table 4: Portfolios vs. USMV Parent Index S&P 1500 S&P 900 S&P 1000 Period (years) 2.644 2.644 2.644 Portfolio Stats R 0.177 0.167 0.11 SD 0.127 0.127 0.145 Sharpe 1.396 1.312 0.757 Calmar 0.353 0.353 0.353 Beta 1.025 1.025 1.025 Benchmark R 0.191 0.191 0.191 SD 0.097 0.097 0.097 Sharpe 1.982 1.982 1.982 Calmar 3.074 3.074 3.074 Relative Stats (port/bench) R 0.923 0.873 0.574 Sharpe 0.704 0.662 0.382 Calmar 0.115 0.115 0.115 Beta^-1 0.976 0.976 0.976 Score 0.519 0.504 0.396 A bit to my own surprise, we see that USMV outperformed the other minimum variance stock portfolios. I would have thought the S&P 1500 and S&P 1000 portfolios would outperform in that the former incorporates more equities, and the latter is optimized on a class of equities, which have traditionally exhibited larger risk premia. Even optimized on a similar large and mid-cap space, USMV outperforms. Moreover, USMV has more constraints on its portfolio construction, such as turnover restrictions or an upper bound of 1.5% on any given asset. Furthermore, it has an expense ratio. It does have three advantages that spring to mind. The first is that it dynamically adjusts every 6 months, whereas the results presented here are computed as an ab initio allocation held for the entire period. The second is that as money pours into the strategy, the stocks in the ETF rise in the price - since the holdings are somewhat distinct, this might give the ETF an edge as money flows into it (but this also may run in the other direction…). Third, is the fact that the index providers may have a bit of secret sauce for how the index is constructed - this is not to say they are hiding something, merely that they may know what constraints provide a slight edge over my "dumb" optimization. That is to say, some smart quant on MSCI's index team may have a keen, but undisclosed, rationale for why no stock may be more than 20x the allocation in its parent index provides a slight edge. In this article, we have seen that minimum volatility strategies have outperformed in the recent period, but that both on a fundamental and theoretical level, this outperformance may be transitory. Nevertheless, the strategy does have some conceptual merit, and might be a good initial skeleton for retail investors who are known to choose riskier higher beta and smaller cap stocks. Beyond a basic industry diversification, retail investors are unlikely to be in a position to exploit the covariance amongst the assets. Some of these correlations are not immediately obvious - for example, my miner, Vale (NYSE: VALE ), is linked to my utility by virtue of the fact that they are both Brazilian. My Australian stocks seem subservient to the whims of Chinese GDP reports, and my gold miner tracks my iron stock. In short, unless you have done the work ahead of time it is fairly easy to inadvertently put together a very volatile portfolio that looks on paper to be very diversified, but trades very wonky. As we saw in Figures 1 and 2, the advantage of the minimum volatility approach is that it at least should keep your equity portfolio somewhere in the triangle between the risk-free-rate, risk-optimal return, and the market portfolio; staying out of the dangerous southern hemisphere and wild eastern reaches of the risk-return chart should prevent your portfolio from getting totally wracked on the low-return high-variance shoals of the equity markets. If you are less-risk averse and do not want to use margin, the strategy at least leaves you with some risk-budget to squander, err.., "deploy" on high-octane biotechs or Internet IPOs. For those who do not seek the venerated alpha or who do not want to do-it-yourself, USMV looks like a good implementation of the allocation strategy where its expense ratio vs. VTI might be just good value, rather than a wealth-destroying violation of the Bogleheads' sacred low-fee doctrine. Scalper1 News

Scalper1 News