Is SCHC The Right ETF For International Exposure?

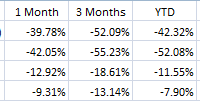

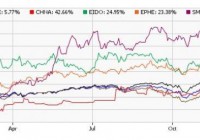

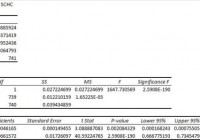

Summary I’m taking a look at SCHC as a candidate for inclusion in my ETF portfolio. The risk level is fairly acceptable for an international ETF. The ETF’s favorable risk profile is driven by the extremely diversified holdings and strong dividend yield. I’m not assessing any tax impacts. Investors should check their own situation for tax exposure. Investors should be seeking to improve their risk adjusted returns. I’m a big fan of using ETFs to achieve the risk adjusted returns relative to the portfolios that a normal investor can generate for themselves after trading costs. I’m working on building a new portfolio and I’m going to be analyzing several of the ETFs that I am considering for my personal portfolio. One of the funds that I’m considering is the Schwab International Small-Cap Equity ETF (NYSEARCA: SCHC ). I’ll be performing a substantial portion of my analysis along the lines of modern portfolio theory, so my goal is to find ways to minimize costs while achieving diversification to reduce my risk level. What does SCHC do? SCHC attempts to track the total return of FTSE Developed Small Cap ex-US Liquid Index. At least 90% of funds are invested in companies that are part of the index. SCHC falls under the category of “Foreign Small/Mid Blend”. Does SCHC provide diversification benefits to a portfolio? Each investor may hold a different portfolio, but I use (NYSEARCA: SPY ) as the basis for my analysis. I believe SPY, or another large cap U.S. fund with similar properties, represents the reasonable first step for many investors designing an ETF portfolio. Therefore, I start my diversification analysis by seeing how it works with SPY. I start with an ANOVA table: (click to enlarge) The correlation is about 69%, which is low enough to provide some solid diversification benefits so long as the ETF does not have an innately high level of risk. I measure risk with the standard deviation of daily returns. It isn’t perfect, but it works fairly well for my purposes and seems to hold up over time. Standard deviation of daily returns (dividend adjusted, measured since January 2012) The standard deviation is pretty good for foreign investments. For SCHC it is 0.8657%. For SPY, it is 0.7300% for the same period. Since SPY usually beats other ETFs in this regard, I’d look at that standard deviation level as being fairly favorable for an ETF that is competing for selection as a “Foreign Markets” ETF in my portfolio. Mixing it with SPY I also run comparison on the standard deviation of daily returns for the portfolio assuming that the portfolio is combined with the S&P 500. For research, I assume daily rebalancing because it dramatically simplifies the math. With a 50/50 weighting in a portfolio holding only SPY and SCHC, the standard deviation of daily returns across the entire portfolio is 0.7636%. Even in developed markets, I think 50% of a portfolio is way too high. When I drop the exposure to 20% in SCHC the standard deviation drops to .7342%. That’s a clear improvement, but I’d still like to see it a little lower. At 5%, the standard deviation is down to .7299% and diminishing returns are strongly in effect. Relative to other international investments, SCHC seems like a viable candidate for a larger position. I still wouldn’t consider going over 20%, but I think 5% to 10% is within reason. Why I use standard deviation of daily returns I don’t believe historical returns have predictive power for future returns, but I do believe historical values for standard deviations of returns relative to other ETFs have some predictive power on future risks and correlations. Yield & Taxes The distribution yield is 2.98%. The SEC 30 day yield is 2.11%. The ETF invests in foreign securities and I’m not a CPA or CFP. Investors concerned about tax consequences should seek advice from someone knowledgeable about their tax situation. If taxes are not a factor, the distribution yield is reasonable for producing income. Expense Ratio The ETF is posting .19% for an expense ratio. This is higher than the last few ETFs I have considered, but not high enough to stop me from considering it as a significant part of a portfolio. Market to NAV The ETF is trading right on NAV currently. However, premiums or discounts to NAV can change very quickly so investors should check prior to putting in an order. Largest Holdings The diversification within the ETF is excellent, as shown by the following chart: (click to enlarge) I don’t like including a significant position of U.S. dollars within an investment portfolio, but it is less than 2% and the portfolio of investments is phenomenally diversified. Since this ETF invests in smaller companies it is very important for the ETF to have extremely high levels of diversification. As long as the ETF trades near NAV, the ETF’s high level of diversification should continue to lead to relatively low levels of standard deviations. If there was a black swan even or investors soured heavily on international markets it could create an impact that would reach a large portion of the portfolio. Outside of those major events, the extreme diversification should help to stabilize the fund. Investing in the ETF is largely relying on modern portfolio theory. Making an investment requires a belief that markets are at least somewhat efficient so that the companies within the portfolio will be reasonably priced. Conclusion I’m currently screening a large volume of ETFs for my own portfolio. The portfolio I’m building is through Schwab, so I’m able to trade SCHC with no commissions. I have a strong preference for researching ETFs that are free to trade in my account, so most of my research will be on ETFs that fall under the “ETF OneSource” program. SCHC looks pretty good to me so far and is a leading candidate for inclusion in the portfolio.