Best Multi-Asset ETFs For 2015

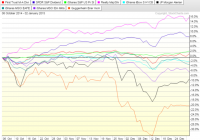

Summary MDIV remains the go to choice for a multi-asset ETF. Actively managed INKM saw its first test during a down market and it passed the test, outperforming the competition and emerging with an increased cash position. IYLD could find itself at the top of the heap at the end of 2015 if volatility remains elevated throughout the year. In last year’s article, The Best Multi-Asset ETF , I looked at which multi-asset ETFs were best under different conditions. Since the October 6 date of publication, there’s been a lot of volatility in the energy and currency markets, and several multi-asset ETFs were negatively impacted. For those who want a background on an individual fund, each of the seven ETFs was covered separately: Performance in Q4 2014 First, let’s look at a chart of the underlying assets held by most multi-asset ETFs. In the chart below are ETFs directly held by some multi-asset funds, or proxies which cover asset classes found in multi-asset funds. Along with MDIV are the SPDR S&P Dividend (NYSEARCA: DVY ), the iShares S&P U.S. Preferred Stock (NYSEARCA: PFF ), the iShares Cohen & Steers Realty Majors (NYSEARCA: ICF ), the iShares iBoxx $ High Yield Corporate Bond (NYSEARCA: HYG ), the JPMorgan Alerian MLP Index (NYSEARCA: AMJ ), the iShares MSCI EAFE (NYSEARCA: EFA ), the iShares MSCI Emerging Markets (NYSEARCA: EEM ) and the Guggenheim Canadian Energy Income (NYSEARCA: ENY ). (click to enlarge) That is a wide range of returns for a three-month period, partially because the start of the chart occurs during the early autumn sell-off in global markets. ICF doubled the return of its nearest competitor, which was dividend paying stocks. MDIV is in the middle of the pack along with preferred shares, junk bonds, and the EAFE. The big losses came from MLPs and Canroys, victims of the collapse in oil prices. Here’s a chart showing how multi-asset ETFs performed since October 6. (click to enlarge) Performance Review MDIV was given the title of Best Multi-Asset ETF because it spreads investments across asset classes such as REITs, MLPs, common stocks, preferred stocks, and junk bonds. The fund doesn’t take on extra risk to bump up its yield, incorporates some volatility factors in its model to reduce volatility, and should generally fall in the middle of the multi-asset ETF pack. MDIV gained 8.07 percent in 2014, and it mainly went sideways from October 6 on, gaining about 1.5 percent. MLPs are 20 percent of the portfolio and they under performed by a wide margin over the past three months, but REIT shares are also 20 percent of assets and they rallied more than MLPs fell. Overall, MDIV performed as expected, falling in the middle of the pack while delivering a positive return. GYLD was named the runner-up because it takes a global approach to the multi-asset model. However, enhanced risk was highlighted: GYLD used exposure to Venezuelan bonds and Canroys to achieve a higher yield. These assets were among the worst performers over the past three months and it led to a roughly 6 percent loss for the ETF. GYLD also fell 3.48 percent in 2014. As long as the U.S. dollar remains in a bull market, GYLD will struggle relative to domestic multi-asset ETFs, but energy is having a bigger impact on the portfolio. If energy remains weak, GYLD will lag the field. CVY was dubbed the “not-so-multi-asset-ETF” due to its hefty weight in common stocks, but it also made use of Canroys and MLPs to boost the portfolio’s total yield. The result was a heavy energy tilt: as of September 30, the most recent sector breakdown, CVY had 27 percent of assets in energy. This cost the fund over the past three months, and lowered CVY’s 2014 return to negative 4.33 percent. YDIV was the other poor performer over the past three months due to it being an international fund holding non-U.S. dollar assets. Australian and Canadian assets made up nearly 40 percent of assets back in September and 39 percent of the fund was in the two countries as of January 2, 2015. Australia and Canada are influenced by commodity prices, and Australian resource exports are hurt by the slowing Chinese economy. YDIV also has some assets in Chinese banks and Hong Kong companies, which raises the potential exposure to a China slowdown to more than 40 percent of assets. YDIV was going to underperform domestic multi-asset funds in 2014 no matter what simply due to being an international fund holding non-dollar assets, but it only fell 0.79 percent in 2014, and only 3.38 percent in the past three months because it isn’t directly exposed to commodities, specifically energy. This helped it beat both GYLD and CVY last year, two funds that were much more exposed to energy. IYLD was one of the stronger performers over the past three months because it mainly invests in bonds, to the tune of 75 percent of assets. Domestic dividend paying equities make up 10 percent of assets, with another 10 percent in international dividend paying equities, plus 5 percent in international real estate. IYLD also benefited from declining interest rates at the long-end; its 5 percent holding in the iShares Barclays 20+ Year Treasury (NYSEARCA: TLT ) was up 27 percent in 2014. IYLD rallied 10.29 percent for the full year and it climbed 1.88 percent in the past three months. The last two funds covered were FDIV and INKM, both actively managed. INKM’s performance was sub-par from its inception in April 2012, but financial markets enjoyed mostly smooth sailing for most of its life. Since October, INKM has beaten the multi-asset competition, gaining 3.41 percent in the past three months and 8.80 percent in 2014. INKM’s managers have adjusted the portfolio since September 25 (when I covered it here ). The fund raised cash from near 0 percent to 4 percent. High yield bonds are up from 6 percent to 9 percent. Equity exposure was cut from near 42 percent to 37 percent. Among individual holdings, the SPDR Barclays Long Term Treasury (NYSEARCA: TLO ) has climbed from 5.15 percent in September to 6.21 percent exposure. The SPDR Emerging Markets Dividend (NYSEARCA: EDIV ) was cut from 5.82 percent to 2.84 percent. The SPDR Dow Jones International Real Estate (NYSEARCA: RWX ) was raised from 4.85 percent to 6.23 percent. The SPDR Barclays High Yield Bond (NYSEARCA: JNK ) was increased from 6.09 percent to 8.95 percent. The SPDR Barclays Emerging Markets Local Bond (NYSEARCA: EBND ) was cut from 4.00 percent to 2.96 percent. One of the big questions with a fund such as INKM was how it might perform if markets moved against high-yield assets, such as due to rising interest rates. Long-term rates didn’t rise in late 2014, but energy prices tumbled, the dollar rallied sharply and high-yield bonds sold off. INKM managers navigated the past three months well and if they can keep it up, this fund will be a serious contender for investor capital. The 30-day SEC yield is still one of the lowest of the group at 3.25 percent, but if managers are able to mitigate losses during unfavorable periods for multi-asset ETFs, it could turn into a long-term outperformer. The other actively managed multi-asset ETF has a short history of only 5 months, but FDIV delivered similar results to INKM in the past three months, gaining 1.77 percent. Interestingly, FDIV’s managers moved in the opposite direction of INKM’s managers. Back on September 29, FDIV had 16.30 percent of assets in high-yield bonds and senior loans. As of January 2, the portfolio exposure to high-yield bonds was cut to 12.48 percent, with exposure to international sovereign bonds increased about 2 percentage points, MLP exposure increased 1 percentage point and dividend paying equities increased 1.5 points. FDIV has a 30-day SEC yield of 3.88 percent. After a rough period for multi-asset ETFs, both actively managed funds look more attractive today than they did three months ago. Best Fund For The Start of 2015 Assuming the U.S. dollar continues to strengthen, emerging markets and commodities remain weak and long-term interest rates do not rise, the following multi-asset ETFs look most attractive. For investors not worried about rising rates or trouble in high-yield bonds, but concerned about weakness in equities or MLPs, IYLD is a solid choice. It has 75 percent exposure to fixed income and a 5.83 percent yield, with dividends paid monthly. MDIV remains the go-to option for long-term passive investors. It won’t deliver big returns, but it yields 5.93 percent and also pays dividends monthly. If energy recovers and equities climb in 2015, MDIV will likely outperform IYLD. Given its track record over the past three months, INKM also looks attractive for total return investors who want active management. Of course, if you expect a big rebound in energy, GYLD or CVY look more attractive. GYLD currently yields 6.70 percent, but beyond risk of capital losses, there’s also the risk of dividend cuts if energy prices continue on their present trajectories.