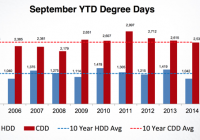

TECO Energy (NYSE: TE ) Q4 2014 Earnings Call February 09, 2015 10:00 am ET Executives Mark M. Kane – Director of Investor Relations Sandra W. Callahan – Chief Financial Officer, Chief Accounting Officer and Senior Vice President of Finance & Accounting John B. Ramil – Chief Executive Officer, President, Director and Member of Finance Committee Analysts Ali Agha – SunTrust Robinson Humphrey, Inc., Research Division Paul Zimbardo – UBS Investment Bank, Research Division Paul T. Ridzon – KeyBanc Capital Markets Inc., Research Division Andrew Bischof – Morningstar Inc., Research Division Scott Senchak Operator Good morning. My name is Keisha, and I will be your conference operator today. At this time, I would like to welcome everyone to TECO Energy’s Fourth Quarter Results and 2015 Outlook Conference Call. [Operator Instructions] I would now like to turn the call over to Mr. Mark Kane, Director of Investor Relations. You may begin, sir. Mark M. Kane Thank you, Keisha. Good morning, everyone, and welcome to the TECO Energy Fourth Quarter 2014 Results Conference Call. Our earnings, along with unaudited financial statements, were released and filed with the SEC earlier this morning. This presentation is being webcast; and our earnings release, financial statements and slides for this presentation are available on our website at tecoenergy.com. The presentation will be available for replay through the website approximately 2 hours after the conclusion of our presentation and will be available for 30 days. In the course of our remarks today, we will be making forward-looking statements about our expectations for 2015 and beyond and our integration of New Mexico Gas Company and the sale of TECO Coal. There are number of factors that could cause actual results to differ materially from those that we’ll discuss today. For a more complete discussion of these factors, we refer you to the risk factor discussion in our annual report on Form 10-K for the period ended December 31, 2013, and an updated and subsequent filings with the SEC. In the course of today’s presentation, we will be using non-GAAP results. There is a reconciliation between these non-GAAP measures and the closest GAAP measure in the Appendix to today’s presentation. The host for our call today is Sandy Callahan, TECO Energy’s Chief Financial Officer. Also with us today is John Ramil, TECO Energy’s CEO, to assist in answering your questions. Now let me turn it over to Sandy. Sandra W. Callahan Thank you, Mark. Good morning, everyone, and thank you for joining us today. We appreciate your flexibility with the revised date for our call, which was necessary in order to work through the accounting impact of amending our agreement to sell the coal company. We were in discussions with the purchaser, and it became clear that a revision to the selling price was necessary. And since the appropriate accounting was to reflect that impact in the fourth quarter, we rescheduled the call in order to make the required changes to our financial statements. Today, I’ll cover our financial results, what we’re seeing in the Florida and New Mexico economies, the sale of TECO Coal and 2015 guidance as well as the longer-term outlook. As usual, the Appendix to this presentation contains graphs on the Florida and New Mexico economies and reconciliations of non-GAAP to GAAP measures. In the fourth quarter, non-GAAP results from continuing operations were $45 million or $0.19 per share compared with $0.18 last year. GAAP net income was $10.8 million, which includes a loss in discontinued operations of $16.6 million reflecting impairment charges of $11.6 million and the operating results of TECO Coal. Net income from continuing operations were $27.4 million in 2014 and includes $17.6 million of charges, consisting of transaction and integration costs of $3 million related to the New Mexico Gas acquisition and the $14.6 million adjustment to deferred state income taxes related to the pending sale of TECO Coal. Excluding these items, the non-GAAP results for continuing operations were $0.19 per share. For the full year, non-GAAP results from continuing operations were $1.03 per share, 11% higher than 2013’s $0.91. GAAP net income of $130.4 million or $0.58 includes a loss in discontinued operations of $76 million, which largely reflects value impairments at TECO Coal. Net income from continuing operations was $206.4 million or $0.92 and includes $23.3 million of charges and net tax adjustments related to acquisition and sale activities. Excluding these items yields the non-GAAP results of $229.7 million or $1.03 per share. Tampa Electric reported slightly lower net income in the fourth quarter. While customer growth was a strong 1.6% and we had 1 additional month of higher revenues from a 2013 rate settlement, energy sales were lower due to milder weather resulting in fourth quarter revenues in 2014 about the same as the prior year. AFUDC increased this quarter with higher investment balances in the Polk conversion project and the related water project; and O&M expense was lower. The quarter-over-quarter increase in depreciation expense represented more than just the normal increase from additions to facilities. That’s because in 2013, fourth quarter depreciation had included the benefit of a full 12 months of lower amortization costs to retroactively reflect the change in software life agreed to a November 2013 rate case settlement. Weather patterns resulted in retail net energy per load in the fourth quarter that was 2.8% below 2013. Looking at degree days, which were 10% below normal and 12% below last year, you might expect energy sales to be off more than they were even with the customer growth we saw. In Tampa, we actually have both heating and cooling degree days in the fourth quarter. In this quarter, heating degree days were about normal and cooling degree days were well below normal, and that combination produced a milder impact on energy usage than the 10% and 12% degree days variances would suggest. Peoples Gas experienced strong customer growth of 2.3% in the fourth quarter, which was higher than our full year estimates. That was due to robust growth in several of the southwest Florida markets that had been the most impacted in the economic downturn, as well as substantial growth in northeast Florida. We saw higher therm sales to all customer segments, residential, commercial and industrial, as a result of the periods of cold weather in the quarter, as well as continued economic growth. On the expense side, O&M was lower in 2014 while depreciation was up. New Mexico Gas fourth quarter results benefited from customer growth and the start of the winter heating season even though it was actually milder than normal and milder than 2013. New Mexico Gas is much more seasonal than Peoples Gas, and the fourth quarter is a very strong quarter for them, which resulted in about $0.03 of accretion to our consolidated fourth quarter earnings. The other net segment is what we used to refer to as parent other. The net cost in this segment was higher in the fourth quarter compared to last year driven by interest expense at New Mexico Gas Intermediate, which is a parent of New Mexico Gas Company; and the interest that we no longer allocated to TECO Coal following its classification as a discontinued operation. The Florida economy continues to be a good story. Statewide unemployment at the end of the fourth quarter was 5.6%, an improvement of 7/10 from a year ago. At the same time, the state has added more than 233,000 new jobs over the past year, with the largest number of new jobs occurring in business services, trade transport and utilities and leisure and hospitality. The biggest percentage gain occurred again this quarter in the construction sector, which has posted 8% to 10% employment gains every quarter this year. Hillsborough County, Tampa Electric’s primary service territory, also continues to do well. We appear to be back to the pattern that was normal before the economic downturn, with Tampa area unemployment being better than both the state and national level. The employment rate in local area is down to 5.2%, 6/10 below where it was a year ago, and it is not a function of people leaving the workforce, as workforce grew by 0.5% in the same time frame. Over the past year, the Tampa-St. Pete area added more than 14,000 jobs, with the largest gains in business services followed by trade transport and utilities. Supported by the oil and gas industries and the large presence of governmental facilities in the state, the unemployment rate in New Mexico never came close to the levels we saw in Florida, where job losses in the construction and financial services sectors were severe due to the housing market crash. The largest gains in New Mexico’s 2014 job growth of 13,000 came in trade transport and utilities and education and health services. To put some perspective on the job numbers here, it’s interesting to note that the population of New Mexico of about 2.1 million was actually less than the population of the Tampa-St. Pete MSA, which has a population of about 2.8 million. Taxable sale, both in Florida and in Hillsborough County, continue to grow at the strong pace we’ve seen pretty consistently over the last 4 years. We don’t have that statistics here for New Mexico, as we haven’t yet found a ready source of similar information. On the housing front, more than 5,000 single-family building permits were issued in Tampa Electric service territory in 2014, and existing homes continue to sell at a strong pace. The January Case-Shiller report shows that selling prices in the Tampa market increased 6.8% year-over-year, which doesn’t seem to have dampened sales, and the housing inventory remains at a healthy level of 4 months. The New Mexico housing market saw 5,500 building permits issued statewide in 2014, which was an 8% increase over 2013. In Albuquerque, the state’s largest metro area, existing home resales have trended up steadily although slowly since the downturn, and the housing inventory is about 6 months. You can see all of these trends on the graphs in the Appendix. I’m not going to cover all of the details on the New Mexico Gas acquisition, but I do want to point to a few important takeaways. Consistent with the outlook we provided in our third quarter call, the acquisition was accretive to fourth quarter earnings by $0.03; and for the full year, $0.01. You’ll recall that it diluted EPS $0.02 in the third quarter as we had the associated shares outstanding in the entire quarter and 1 month of ownership during the typical seasonal loss period. With our 2015 business plans in place and with the rapid progress implementing our integration plan, we expect the acquisition to be accretive to full year 2015 earnings, and that’s earlier than we originally anticipated. Last October, we announced that we had entered into an agreement to sell TECO Coal to Cambrian Coal Corporation, a subsidiary of Booth Energy, a central Appalachian coal producer with operations in the same general areas as TECO Coal. The sale was contingent upon the purchasers obtaining financing. The coal markets have continued to weaken for several months now. And last week, we amended the agreement to adjust the selling price to reflect market condition and to extend the closing date to March 13. Under the amended agreement, we will receive $80 million at closing and have the opportunity to receive an additional $60 million over the next 5 years if benchmark coal prices reach certain levels. The purchaser launched financing activities last week after the amended agreement was executed. In the third quarter, we classified TECO Coal’s operations as discontinued operation and its assets as assets held for sale. At that time, we recorded noncash impairment charges of $64.8 million after-tax. We recorded additional impairment of $11.6 million in the fourth quarter, and the $16.6 million fourth quarter loss in discontinued operations includes that additional charge and the operating result of TECO Coal. Those operating results were impacted by costs related to preparing the company for the sale, such as severance and other employee termination costs. As we’ve disclosed previously, the actual closing of the sale will trigger an additional liability-related charge, which we estimate at $7 million. Turning to guidance. We expect 2015 earnings from continuing operations in a range of $1.08 to $1.11 excluding non-GAAP charges or gain. This is a tighter range than we’ve provided in the past, and that’s because our business mix is now all regulated utilities. And while weather is always a variable that can affect utility performance, our operating companies have typically been successful responding to weather variation within a reasonably normal range. We expect Tampa Electric to earn in the upper half of its allowed ROE range. That’s driven by customer growth that we expect will be in line with 2014; energy sales to retail customers other than phosphate, off an estimated 1%; higher AFUDC as we enter a peak spending year for the full conversion project; and an additional $7.5 million of higher base rate that became effective November 1 last year. On the expense side, continued investment in facilities to serve customers will drive higher depreciation and interest costs. We’re projecting lower O&M expense, however, in part, as we realize benefits from acquisition-related synergies and also from lower employee-related expenses including pension and retiree medical costs. 2015 changes to the retiree medical program and growth in planned assets are among the factors contributing to the lower expense. And because the acquisition of New Mexico Gas and sale of TECO Coal caused us to remeasure pension expense last year, that remeasurement captured the negative impact of lower discount rates and mortality improvement in 2014. We expect Peoples Gas also to earn above its allowed mid-point return, which is 10 3/4%. Like Tampa Electric, we expect the customer growth trends we saw last year to continue into 2015 and expect continued interest in vehicle fleet conversion to compress natural gas as well. Although current gasoline prices are helpful, the economics are still favorable, and there are environmental benefits that users like to promote. At the end of 2014, Peoples Gas had 31 CNG filling stations on its system, and the annual volume was the equivalent of about 60,000 Florida residential customers. We expect that number to grow again in 2015. And finally, the Peoples Gas expense profile should be similar to what I described for Tampa Electric. 2015 will represent our first full year of ownership of New Mexico Gas Company. And as I said, we expect it to be accretive in that first full year. And I’d like to be clear that there’s no creative math in that statement as I’m taking into account the performance of the regulated company, NMGI interest costs and the shares we issued. We expect customer growth to start the year at about the same levels as 2014 and trend up through the course of the year with growth in therm sales largely in line with customer growth. We expect lower O&M from acquisition synergies, and we also have the REIT credit of $2 million in the first 12 months post-closing and $4 million in each subsequent 12-month period, which have the effect of sharing some of the synergies with customers. Since we only have 4 months of ownership with New Mexico Gas in 2014, the slide shows some information on previous years to provide some full year context. The Form 2 filed with the New Mexico Commission reported New Mexico Gas Company net income of $23.7 million in 2013, which was a strong weather year with heating degree days about 5% above normal; and $18 million in 2012, when heating degree days were well below normal; and higher rates approved by the commission became effective after the January peak load that already occurred. This slide is just to remind us to show the normal seasonal earnings pattern we expect from NMGC. They make their money in the cold weather in the first and fourth quarters, a fairly normal pattern for a gas LDC that’s heavily residential. It actually complements our existing earnings pattern nicely as Tampa Electric’s strongest quarters are typically the second and third quarters with summer air-conditioning load. The segment we refer to us Other net includes interest at the unrelated finance company, interest at NMGI, certain unallocated corporate level expenses and consolidated tax impacts and smaller operating companies, the only one of note being TECO’s pipeline. We anticipate that the net cost in 2015 will be slightly higher than last year because of a full year of interest expense at New Mexico Gas Intermediate. Although we won’t be allocating any interest expense to TECO Coal as we have in the past, the negative impact from that will be offset by the benefit of refinancing a maturing note series that has a coupon of 6.75%. I would summarize our longer-term outlook in this way. Our regulated businesses are investing in infrastructure to serve customers in our growing rate base 5% to 7%. Our target is to deliver ratable earnings growth that’s in line with rate base growth. The challenges in 2016, recognizing that Tampa Electric’s rate base growth is heavily influenced by full conversion projects while an additional $110 million of annual revenue will become effective when that project goes into service at the beginning of ’17, the base rate increase that benefits 2016 is only $5 million. So a key to delivering earnings growth in 2016 will be effective management of cost across the organization. You can see this on the graphic representation of Tampa Electric’s rate base, which shows it stepping up significantly in ’17 when Polk goes in service. The base revenue pattern is very aligned with the rate base growth you see here. The 2013 rate settlement provided additional base revenues of $57.5 million effective November 1, 2013, which coincided with 2014 rate base growth; $7.5 million at November 1, 2014; $5 million at the same date in ’15; and then $110 million when Polk goes in service in ’17. This graph shows average rate base, and it excludes the assets that we earn on separately through the environmental cost recovery clause and the construction work in progress that earns AFUDC above a threshold amount that is included in rate base. As a reference point, at the end of September of ’14, actual average rate base was $4.1 billion, the environmental assets were about $400 million and that clip was about $200 million. Also, with our upcoming Investor communications schedule, we expect to file our 10-K at the end of this month, and we will be at the UBS and Morgan Stanley conferences the following week and at the Barclays conference in Atlanta in the middle of March. And now I will turn it over to the operator to open up the lines for your questions. Question-and-Answer Session Operator [Operator Instructions] And your first question comes from the line of Ali Agha with SunTrust. Ali Agha – SunTrust Robinson Humphrey, Inc., Research Division A couple of questions. One is, you recently raised your dividend by 2.3%. And I wanted to just get a sense of what is the philosophy on the dividend and growth going forward. I know we’ve talked previously about the NOLs, but they’ll go away in a few years. So can you just remind us again how you’re looking at the dividend? And ultimately what’s the payout ratio, and when do you expect to be in that payout ratio? John B. Ramil This is John Ramil, and I appreciate you asking that question. When we look at our payout ratio versus our guidance for next year, it’s a little bit above 80% as opposed to our kind of normalized target of 60% to 70%. And we expect over time with the 5% to 7% earnings per share growth, coupled with a modest dividend growth that we will work ourselves back into that more normalized range as we work ourselves out of the NOL position, and that’s expected to be in about 2019. Ali Agha – SunTrust Robinson Humphrey, Inc., Research Division Understood. Great effort. Second question, John, as you, I think, pointed out on the coal sale, the buyer, I guess, started their financing plans last week as well. Any concern at all about their ability to raise the financing? I know that’s the contingency left to close this. John B. Ramil Well, you’re right, they did kick off their financing on Friday of last week, and we’ve been working very closely with them on where they are in their financing, what the markets are doing and in working with them with the objective of getting this deal closed and moving the coal business out of our portfolio. That’s why we agreed to an amended deal to really strengthen the ability for them to get the financing for this transaction to close. Ali Agha – SunTrust Robinson Humphrey, Inc., Research Division Okay, and you’re very confident that, that financing will close. I mean, there’s no — I mean, from your perspective as the seller, any concerns? John B. Ramil All the indications we have and the advice that we’re getting is where we’re at in pricing and where the markets are expected to be, that transaction can close. Ali Agha – SunTrust Robinson Humphrey, Inc., Research Division And my last question. On New Mexico, as we think about calendar 2015, you were talking about your expectations for Tampa Electrics on the ROE and Peoples Gas on the ROE. How should we think about New Mexico’s on the ROE? I believe their authorize is 10%, if memory serves me right. So how should we think about what — where — roughly where they should be earning in the order of magnitude? John B. Ramil That’s correct. And with all of our people doing very, very good cost control work, as you can see, that is continued in 2014. And with the synergies that all of our utilities are seeing from the integration, it’s helping improve all the ROEs. And New Mexico Gas has been low — earning closer to 9% ROE, and we expect to keep moving that up towards that 10%. Ali Agha – SunTrust Robinson Humphrey, Inc., Research Division Okay. Somewhere between 9% and 10% should be the expectation for ’15? John B. Ramil That’s correct. Operator And your next question comes from the line of Paul Zimbardo with UBS. Paul Zimbardo – UBS Investment Bank, Research Division I just had a question about what your thoughts are on possibility of rate base gas and solar opportunities. nexAir has talked about it on some of the recent calls. And just how do you think about that going forward for you? John B. Ramil Well, we’re watching what’s happening with Florida Power and Light very closely. They reached — got some approvals along the way, and there’s still more things to happen there. And with the proper regulatory treatment, it’s a reasonable investment for utilities to make. So we’re keeping our eyes closely on it. We’re also very interested in large-scale solar. We expect that over time, that’s going to make more and more sense. We think that the commission is receptive to the right projects. In fact, last year, late in the year, I think it was during the fourth quarter, we announced the plans to install a larger scale solar facility at the Tampa International Airport. So we’re moving in that direction. We looked ahead to our next capacity need after the Polk expansion, being in about 2020, and while we have that kind of penciled in as a combustion turbine at this point, we think it’s likely that through some combination of various size solar projects, we’d see that CT replaced with solar capacity. And we think that the commission, the economics and the realities of additional environmental requirements will make that good decision. Paul Zimbardo – UBS Investment Bank, Research Division Okay, so no real plans to do anything in the next 3, 4 years, take advantage of ITC or anything like that? John B. Ramil Well, I just mentioned we announced a project in the Tampa International Airport, and that will go into service in that time period. But beyond that, I mean, our immediate need is being met by the Polk expansion, which is driving our growth through 2016 — I’m sorry, through 2017. Paul Zimbardo – UBS Investment Bank, Research Division Okay, got it. And then one other last question. On the current refinancing of the 6.75% notes, are you able to quantify the magnitude if you plan on letting any of that roll off? Or will it just be a straight refinancing? Sandra W. Callahan We will likely refinance the whole maturing amount. Operator And your next question comes from the line of Paul Ridzon with KeyBanc. Paul T. Ridzon – KeyBanc Capital Markets Inc., Research Division If parent companies in Cambrian have issues, kind of can you talk about Plan B? John B. Ramil Sure. We’ve been working with them for quite a while. We have had other expressions of interest but feel that they are the most likely candidate to get this transaction done. If, for some reason, that doesn’t happen, we will look to others as possible buyers, and we’ll also look at other ways of selling the asset. Paul T. Ridzon – KeyBanc Capital Markets Inc., Research Division And given the lower economics, does that impact equity needs at all? John B. Ramil No. Paul T. Ridzon – KeyBanc Capital Markets Inc., Research Division Okay. And then lastly, can you kind of give the next couple of years’ CapEx schedule? Sandra W. Callahan Well, we will be filing a revised capital spending forecast in our 10-K. Paul T. Ridzon – KeyBanc Capital Markets Inc., Research Division At the end of this month? Sandra W. Callahan At the end of this month, right. Operator And your next question comes from the line of Andy Bischof with MorningStar. Andrew Bischof – Morningstar Inc., Research Division LI know the total potential future consideration came down as part of the amended coal deal. But can you speak to whether or not the benchmark pricing come down at all? John B. Ramil The future consideration actually went up to $60 million and the benchmark number stayed the same. Operator And your next question comes from the line of Scott Senchak with Cannon. Scott Senchak Just you have some debt maturities also in ’16 and ’17. I was just wondering what your plans were there. John B. Ramil Scott, would you repeat that? I’m not sure exactly what you asked. Scott Senchak Sorry, you have some debt maturities in 2016 and 2017. I was just wondering what your plans are for those as well. Should we expect a straight refinancing there or what the plan is there? Sandra W. Callahan For the most part, Scott, probably refinancing, but we may retire some portion of those maturities in those years. Operator [Operator Instructions] At this time, there are no further questions. I would like to turn the call back over to Mr. Mark Kane. Mark M. Kane Thank you, Keisha. Thank you, all, for joining us today. We know there are other activities occurring in this morning, so we appreciate you taking your time to join us on our call. And we look forward to seeing you at various Investor conferences in the future. This concludes our call. Thank you. Operator Thank you, all, for your time and participation. This does conclude today’s conference call. You may now disconnect.