Capitalize On Rising Interest Rates With KRE

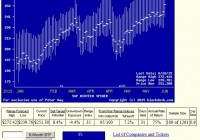

ETF investing, portfolio strategy, special situations “}); $$(‘#article_top_info .info_content div’)[0].insert({bottom: $(‘mover’)}); } $(‘article_top_info’).addClassName(test_version); } SeekingAlpha.Initializer.onDOMLoad(function(){ setEvents();}); Summary Interest Rates Are Going to Rise. Regional Banks Perform Well When Interest Rates Rise. Invest In KRE To Avoid Overexposure To Individual Stocks. Introduction I have harped on and on and on about the inevitability of rising interest rates, so I’ve determined that this will be my last article forewarning investors to prepare their portfolios for the day, or drawn out period (Remember ” Be Patient “) that interest rates rise. Capital appreciation is a daunting task when industry experts believe a sudden rise in interest rates could lead to a market correction of 20 percent . I find it prudent for investors to find an equity that will inherently perform better under projected future market conditions. Like credit default swaps in 2008 or corporate lawyers after the BP oil spill, I believe the SPDR S&P Regional Banking ETF (NYSEARCA: KRE ) will perform exceptionally when rates finally go up. Why Regional Banks? Regional banks tend to be less widespread and more reliant on net interest margins than their larger corporate adversaries. The theory is that regional banks focus more on lending and less on areas like capital markets and treasury services. A diversified large cap bank such as Bank of America (NYSE: BAC ) will have around 48 percent of its income broken into net interest income. While 48% is clearly significant, many regional banks have an average net interest income around 55%. Other regional banks have net interest incomes as high as 60-65%. Five such stocks are Comerica (NYSE: CMA ), SunTrust Banks (NYSE: STI ), MB Financial (NASDAQ: MBFI ), M&T Bank Corporation (NYSE: MTB ), and Huntington Bancshares (NASDAQ: HBAN ). A more comprehensive list of regional banks for the inquisitive investor include can be found on the bull sector . Due to a prolonged low interest rate environment, many banks are relying on fees and low margins from loans to maintain profitability. Gradually rising rates will benefit regional banks. Why KRE? Choosing a good ETF is a remarkably efficient way to spread risk across an industry. By reducing exposure, one can avoid the pitfalls associated with the poor performance of an individual equity. For any ETF, the three metrics that I place the most value on are: diversification, dividends, and its expense ratio. KRE is well diversified with 94 holdings (none weighted over 1.3%). KRE has an annualized dividend yield of 1.54%, and finally KRE has a very low expense ratio at .35% compared to an industry average .5%. It should also be noted that KRE has returned 9.30% YTD and it is by far the most actively traded ETF with an average volume of 4,051,374. The second most traded regional banking ETF is the iShares U.S. Regional Banks ETF (NYSEARCA: IAT ) with a measly 218,517 average volume. I believe the voice of the market has spoken loudly in favor of KRE. In addition, investing in KRE over another ETF helps one avoid the risks associated with low volume (illiquidity, volatility, etc.). For aesthetic purposes, I included a three year chart that compares 10 year treasury yields to KRE’s year to year performance. I included the chart to drive home the point that interest rates and the regional banks are correlated and interconnected. Conclusion Interest rates are going to rise. Regional banks perform well when interest rates rise. Avoid the pitfalls associated with investing in individual stocks by investing in an ETF. The best regional banking ETF, in my opinion, is KRE. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Share this article with a colleague