Update On American Express And Investing Tips

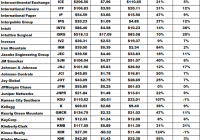

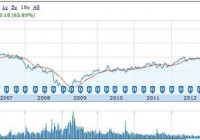

American Express is down $10 a share from our entry price. Nevertheless we are staying the course and holding this stock long term. We will not be shorting stocks in our 1% portfolio. There are many more “long” millionaires than “short.” Our new position, BND, is performing well. It will be a good anchor for our portfolio as its volatility seems to be very low. So finally the ECB has decided to resort to quantitative easing like the U.S. It actually is going to spend 60 billion euros a month instead of the 50 billion figure leaked yesterday. Will it work? Has quantitative easing worked in the U.S.? The bulls would say yes with 5% GDP and low unemployment. The bears would say no with trillions of extra debt and an upcoming dollar crisis. I’m with the bears on this one. All throughout history printing money has always lead to inflation and a weak currency. Would you prefer to live in Switzerland where the Swiss central bank has decided to stop printing money (finally) or Spain where the ECB is going to print 720 billion euro this year alone? The “unintended consequences” will soon start to emerge as all fiat currencies will begin to lose substantial purchasing power. At this inflection point, the public will rush into hard assets such as Gold and Silver. Our portfolio is doing well with now close to $400k invested. I want to touch on American Express Company (NYSE: AXP ) as a follower asked me about its validity going forward. We bought the stock at $94 and currently the stock is trading at around $84 a share. Also the portfolio received a dividend payment of $69 last week. The stock is selling off today due to earnings that were announced in the last 24 hours. Furthermore the company announced recently that it is cutting at least 4000 jobs. Irrespective of the negativity surrounding American Express lately, we are not selling our position. Yes the dividend yield is low at 1.2% but the company has committed to increased dividends and subsequently has increased its dividend for the last three years. However there are many more reasons to hold this stock long term. First of all it dominates its industry and when a company has this much market share, it recovers from recessions quicker than other companies ( see its recovery in the chart below since 2008). The company is still well-priced at these levels and its market cap just continues to grow over time. Have the courage to hold it. In the long term it will do very well. We as fundamental investors who will continue to collect dividends and option premium and wait for the stock price to recover. (click to enlarge) The follower is fearful the stock may drop ( and it may do – in the short term). As investors we need to invest with the end goal in mind. We can’t be taken off course just because of sharp movements in our underlyings. We stay the course and we stick to our plan. Fear also exists on the way up. One such example is the gold market. Long term gold investors are long and will stay long for the long haul. Gold is up 10% already this year. Do these long investors sell and take their profits? No way. These gold bulls are in it for the long haul and that’s how the big profits are made. In one way, holding physical gold is better than holding an ETF or stock. You can’t sell your asset as easily as you can sell an ETF that tracks the Gold price like the SPDR Gold Trust ETF (NYSEARCA: GLD ). Here lack of liquidity is an advantage. Therefore If you believe in your investment, have the courage to hold it through thick and thin. Be prepared to “ride the bull” as that’s where the big profits are in a healthy bull market. Shorting stocks or ETFs also wont happen in this portfolio. There are many distinct disadvantages when shorting underlyings in your portfolio. You are borrowing shares from your broker. You do not have 100% control and sometimes your broker will “call away” your shares at very short notice because the lender wants his stock back. This happens especially when many investors are shorting the same stock. Losses can be infinite (multiple times your initial trade). You need a margin account to short so you pay monthly interest on your bet. Finally I mentioned the other day that the portfolio bought the Vanguard Total Bond Market ETF (NYSEARCA: BND ). I must say that I like its action. Its going to be a good anchor for this portfolio (at least in the short term until the bond trend changes). This ETF tracks 3000 U.S. bonds (all types) and has a 2% annual yield. What’s interesting today is that the iShares 20+ Year Treasury Bond ETF (NYSEARCA: TLT ) and the iShares 7-10 Year Treasury Bond ETF (NYSEARCA: IEF ) are down but our ETF is unchanged. I believe this is the best place to be in the bond sector but we will be watching closely for a trend change and at that point we will put more capital to work in this sector. Automatic profits were taken on positions in McDonald’s Corporation (NYSE: MCD ) and IBM (NYSE: IBM ) this week and new positions were opened (see the screen shot below). (click to enlarge) Current Balances – Making Progress – Slow & Steady wins the race. Now that you’ve read this, are you Bullish or Bearish on ? Bullish Bearish Sentiment on ( ) Thanks for sharing your thoughts. Why are you ? Submit & View Results Skip to results » Share this article with a colleague