Scalper1 News

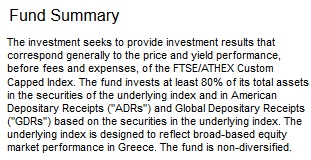

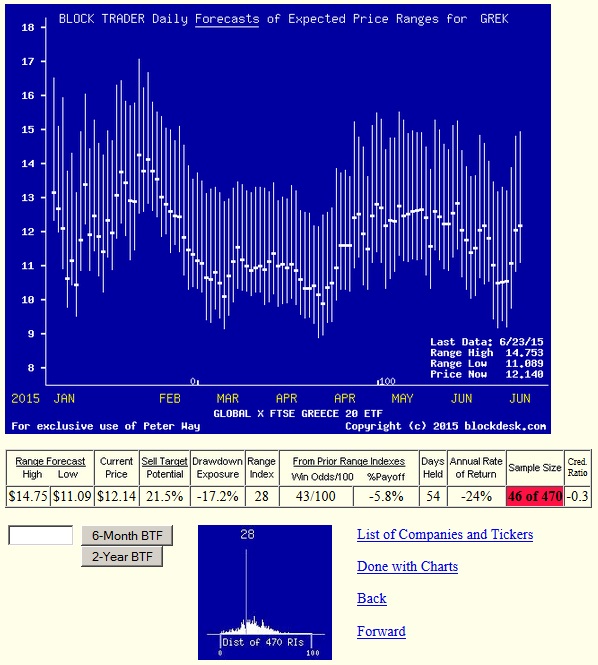

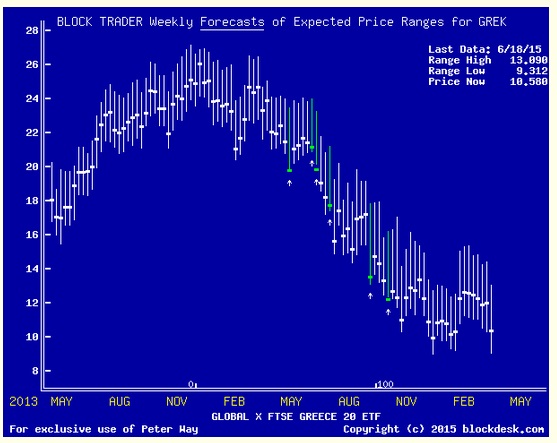

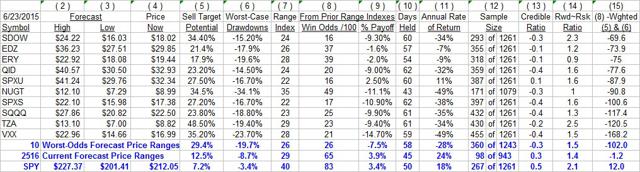

Summary Days ago our article identified an ETF ranked at the best end of the scale posed in the title above, drawing Seeking Alpha reader attention. The ongoing EU vs. Greece drama now reaching a moment of (possible) truth has as one (or more) possible outcome(s) capable of defining an immediate tragedy. Hence the question being raised. And if this is not the worst possible choice of a long ETF position, is (are) there more threatening one(s)? Market-makers have to appraise them all, to do their jobs. We use their hedging actions to tell us what they think. It’s beyond our ken. Way beyond. Value analysis requires comparisons. Without appraisal of the bad, how do we know good? Yin and Yang are both essential. How does GREK look to market-makers? The Global X FTSE Greece 20 ETF (NYSEARCA: GREK ) presents market-makers with a challenging task of appraisal. In our recent article we posed the question this way: From a population of some 350 actively-traded, substantial, and growing ETFs is this a currently attractive addition to a portfolio whose principal objective is wealth accumulation by active investing? We daily evaluate future near-term price gain prospects for quality, market-seasoned ETFs, based on the expectations of market-makers [MMs], drawing on their insights from client order-flows. Following that article’s format where possible, let’s look at their appraisal of GREK. Yahoo describes it this way: The fund currently holds assets of $310 million and has had a YTD price return of -9.1%. Its average daily trading volume of 899,906 produces a complete asset turnover calculation in 29 days at its current price of $11.77. (The Bank of Piraeus may wish it had as long on withdrawals.) Behavioral analysis of market-maker hedging actions while providing market liquidity for volume block trades in the ETF by interested major investment funds has produced the recent past (6 month) daily history of implied price range forecasts pictured in Figure 1. Figure 1 (used with permission) The vertical lines of Figure 1 are a visual history of forward-looking expectations of coming prices for the subject ETF. They are NOT a backward-in-time look at actual daily price ranges, but the heavy dot in each range is the ending market quote of the day the forecast was made. What is important in the picture is the balance of upside prospects in comparison to downside concerns. That ratio is expressed in the Range Index [RI], whose number tells what percentage of the whole range lies below the then current price. Today’s Range Index is used to evaluate how well prior forecasts of similar RIs for this ETF have previously worked out. The size of that historic sample is given near the right-hand end of the data line below the picture. The current RI’s size in relation to all available RIs of the past 5 years is indicated in the small blue thumbnail distribution at the bottom of Figure 1. The first items in the data line are current information: The current high and low of the forecast range, and the percent change from the market quote to the top of the range, as a sell target. The Range Index is of the current forecast. Other items of data are all derived from the history of prior forecasts. They stem from applying a T ime- E fficient R isk M anagement D iscipline to hypothetical holdings initiated by the MM forecasts. That discipline requires a next-day closing price cost position be held no longer than 63 market days (3 months) unless first encountered by a market close equal to or above the sell target. The net payoffs are the cumulative average simple percent gains of all such forecast positions, including losses. Days held are average market rather than calendar days held in the sample positions. Drawdown exposure indicates the typical worst-case price experience during those holding periods. Win odds tells what percentage proportion of the sample recovered from the drawdowns to produce a gain. The cred(ibility) ratio compares the sell target prospect with the historic net payoff experiences. Figure 2 provides a longer-time perspective by drawing a once-a week look from the Figure 1 source forecasts, back over (almost) two years. Figure 2 (used with permission) What does this ETF hold, causing such price expectations? Figure 3 is a table of securities held by the subject ETF, indicating its concentration in the top ten largest holdings, and their percentage of the ETF’s total value. Figure 3 (click to enlarge) Well, maybe that’s what is causing such price expectations, but it seems more likely that international politics has more to do with it. So let’s depart from GRKZF, the Greek Organization of Football Prognostics SA, and turn to the Wall Street organization of stock price prognostics, or market-makers [MMs]. Sport is where you find it. Just how bad is the GREK outlook? We use the MMs forecasts for stock and ETF prices, implied by their self-protective hedging actions, plus the accumulated actuarial history of market price events following such prior forecasts as are seen today, to rank each subject. Figure 4 is a table of how the worst-ranking ten ETFs appear. Please remember, our ranking interest is in wealth-building, not wealth destruction. What works well in one direction may not work in the opposite. Shorting is not recommended. Figure 4 (click to enlarge) When we compare the wealth-building prospects for GREK (ranked 270th out of 340) it doesn’t come close to the terrors inherent in these last ten. Remember, the MMs role is to build a balance between buyers and sellers in every trade, so they have to find acceptable expectations at each end of an actionable array of prices. The actions produce the trade, the expectations are what produce the actions. Check the row of data beneath the top illustration of Figure 1. Its forecast upper end is 23.7% above the then-current price of $10.58. That compares to the ten-ETF average of Figure 4 of +29.4% in column (5). What of the risk exposure? When GREK in the past has been seen by MMs to have an outlook like today’s (a Range Index of 33, meaning twice as much upside as downside) its typical worst-case price drawdown experienced was but -16.3%. The worst-ten ETFs of Figure 4 managed -19.7% — a fifth of their capital gone, not just less than a sixth. And on top of that GREK had 42 out of 100 chances of seeing its price recover back into profit territory, while those other ETFs had but one chance in four of that happening (column 8 blue average). And they started, on average, from prior forecasts with Range Indexes of 26, with three times as much upside as down. See? GREK could be worse. ‘Course it could (needs to) be better. The average equity today offers a 29 Range Index with +12.5% upside. There is real credibility to that population forecast, since prior similar forecast hypothetical positions produced gains of +3.9% (net of 35/100 losses, not 58/100). GREK actually had prior net losses of -6.5% and negative credibility ratio (like the other worst ten ETFs) comparing upside forecasts to actual TERMD payoffs. Conclusion But those are historical comparisons. The past may not be prologue. Buyers must hope so. Besides, there is less than two years of GREK pricing for us to work with. Maybe Greece has just had a bad recent two years. We keep a ten-foot long pole at hand for just such occasions. Hope we don’t have to use it, not sure we would. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Scalper1 News

Summary Days ago our article identified an ETF ranked at the best end of the scale posed in the title above, drawing Seeking Alpha reader attention. The ongoing EU vs. Greece drama now reaching a moment of (possible) truth has as one (or more) possible outcome(s) capable of defining an immediate tragedy. Hence the question being raised. And if this is not the worst possible choice of a long ETF position, is (are) there more threatening one(s)? Market-makers have to appraise them all, to do their jobs. We use their hedging actions to tell us what they think. It’s beyond our ken. Way beyond. Value analysis requires comparisons. Without appraisal of the bad, how do we know good? Yin and Yang are both essential. How does GREK look to market-makers? The Global X FTSE Greece 20 ETF (NYSEARCA: GREK ) presents market-makers with a challenging task of appraisal. In our recent article we posed the question this way: From a population of some 350 actively-traded, substantial, and growing ETFs is this a currently attractive addition to a portfolio whose principal objective is wealth accumulation by active investing? We daily evaluate future near-term price gain prospects for quality, market-seasoned ETFs, based on the expectations of market-makers [MMs], drawing on their insights from client order-flows. Following that article’s format where possible, let’s look at their appraisal of GREK. Yahoo describes it this way: The fund currently holds assets of $310 million and has had a YTD price return of -9.1%. Its average daily trading volume of 899,906 produces a complete asset turnover calculation in 29 days at its current price of $11.77. (The Bank of Piraeus may wish it had as long on withdrawals.) Behavioral analysis of market-maker hedging actions while providing market liquidity for volume block trades in the ETF by interested major investment funds has produced the recent past (6 month) daily history of implied price range forecasts pictured in Figure 1. Figure 1 (used with permission) The vertical lines of Figure 1 are a visual history of forward-looking expectations of coming prices for the subject ETF. They are NOT a backward-in-time look at actual daily price ranges, but the heavy dot in each range is the ending market quote of the day the forecast was made. What is important in the picture is the balance of upside prospects in comparison to downside concerns. That ratio is expressed in the Range Index [RI], whose number tells what percentage of the whole range lies below the then current price. Today’s Range Index is used to evaluate how well prior forecasts of similar RIs for this ETF have previously worked out. The size of that historic sample is given near the right-hand end of the data line below the picture. The current RI’s size in relation to all available RIs of the past 5 years is indicated in the small blue thumbnail distribution at the bottom of Figure 1. The first items in the data line are current information: The current high and low of the forecast range, and the percent change from the market quote to the top of the range, as a sell target. The Range Index is of the current forecast. Other items of data are all derived from the history of prior forecasts. They stem from applying a T ime- E fficient R isk M anagement D iscipline to hypothetical holdings initiated by the MM forecasts. That discipline requires a next-day closing price cost position be held no longer than 63 market days (3 months) unless first encountered by a market close equal to or above the sell target. The net payoffs are the cumulative average simple percent gains of all such forecast positions, including losses. Days held are average market rather than calendar days held in the sample positions. Drawdown exposure indicates the typical worst-case price experience during those holding periods. Win odds tells what percentage proportion of the sample recovered from the drawdowns to produce a gain. The cred(ibility) ratio compares the sell target prospect with the historic net payoff experiences. Figure 2 provides a longer-time perspective by drawing a once-a week look from the Figure 1 source forecasts, back over (almost) two years. Figure 2 (used with permission) What does this ETF hold, causing such price expectations? Figure 3 is a table of securities held by the subject ETF, indicating its concentration in the top ten largest holdings, and their percentage of the ETF’s total value. Figure 3 (click to enlarge) Well, maybe that’s what is causing such price expectations, but it seems more likely that international politics has more to do with it. So let’s depart from GRKZF, the Greek Organization of Football Prognostics SA, and turn to the Wall Street organization of stock price prognostics, or market-makers [MMs]. Sport is where you find it. Just how bad is the GREK outlook? We use the MMs forecasts for stock and ETF prices, implied by their self-protective hedging actions, plus the accumulated actuarial history of market price events following such prior forecasts as are seen today, to rank each subject. Figure 4 is a table of how the worst-ranking ten ETFs appear. Please remember, our ranking interest is in wealth-building, not wealth destruction. What works well in one direction may not work in the opposite. Shorting is not recommended. Figure 4 (click to enlarge) When we compare the wealth-building prospects for GREK (ranked 270th out of 340) it doesn’t come close to the terrors inherent in these last ten. Remember, the MMs role is to build a balance between buyers and sellers in every trade, so they have to find acceptable expectations at each end of an actionable array of prices. The actions produce the trade, the expectations are what produce the actions. Check the row of data beneath the top illustration of Figure 1. Its forecast upper end is 23.7% above the then-current price of $10.58. That compares to the ten-ETF average of Figure 4 of +29.4% in column (5). What of the risk exposure? When GREK in the past has been seen by MMs to have an outlook like today’s (a Range Index of 33, meaning twice as much upside as downside) its typical worst-case price drawdown experienced was but -16.3%. The worst-ten ETFs of Figure 4 managed -19.7% — a fifth of their capital gone, not just less than a sixth. And on top of that GREK had 42 out of 100 chances of seeing its price recover back into profit territory, while those other ETFs had but one chance in four of that happening (column 8 blue average). And they started, on average, from prior forecasts with Range Indexes of 26, with three times as much upside as down. See? GREK could be worse. ‘Course it could (needs to) be better. The average equity today offers a 29 Range Index with +12.5% upside. There is real credibility to that population forecast, since prior similar forecast hypothetical positions produced gains of +3.9% (net of 35/100 losses, not 58/100). GREK actually had prior net losses of -6.5% and negative credibility ratio (like the other worst ten ETFs) comparing upside forecasts to actual TERMD payoffs. Conclusion But those are historical comparisons. The past may not be prologue. Buyers must hope so. Besides, there is less than two years of GREK pricing for us to work with. Maybe Greece has just had a bad recent two years. We keep a ten-foot long pole at hand for just such occasions. Hope we don’t have to use it, not sure we would. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Scalper1 News

Scalper1 News