Scalper1 News

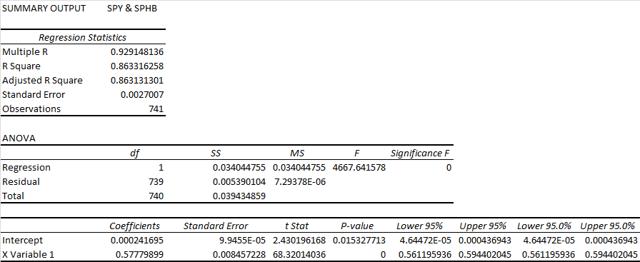

Summary I’m taking a look at SPHB as a candidate for inclusion in my ETF portfolio. The risk level makes me uncomfortable for anything over 5%. The ETF is very well diversified, just not into the kind of companies I want to hold. I’m not assessing any tax impacts. Investors should check their own situation for tax exposure. Investors should be seeking to improve their risk adjusted returns. I’m a big fan of using ETFs to achieve the risk adjusted returns relative to the portfolios that a normal investor can generate for themselves after trading costs. I’m working on building a new portfolio and I’m going to be analyzing several of the ETFs that I am considering for my personal portfolio. One of the funds that I’m considering is the PowerShares S&P 500 High Beta Portfolio (NYSEARCA: SPHB ). I’ll be performing a substantial portion of my analysis along the lines of modern portfolio theory, so my goal is to find ways to minimize costs while achieving diversification to reduce my risk level. What does SPHB do? SPHB attempts to track the total return of the S&P 500® High Beta Index. At least 90% of funds are invested in companies that are part of the index. SPHB falls under the category of “Mid-Cap Blend”. Does SPHB provide diversification benefits to a portfolio? Each investor may hold a different portfolio, but I use (NYSEARCA: SPY ) as the basis for my analysis. I believe SPY, or another large cap U.S. fund with similar properties, represents the reasonable first step for many investors designing an ETF portfolio. Therefore, I start my diversification analysis by seeing how it works with SPY. I start with an ANOVA table: (click to enlarge) The correlation is about 86%. It is low enough to provide some diversification benefits relative to holding SPY, but the benefits won’t be huge so if the standard deviation of returns is too high it may still be difficult to fit SPHB into a portfolio. Standard deviation of daily returns (dividend adjusted, measured since January 2012) The standard deviation is terrible. For SPHB it is 1.1739%. For SPY, it is 0.7300% for the same period. SPY usually beats other ETFs in this regard, but that is a very high standard deviation. Granted, it should be assumed that a high beta portfolio would have a high standard deviation of returns. Under CAPM (Capital Asset Pricing Model) the level of expected return should be easily determined by the beta of the stock. I think high beta stocks frequently more risk than they compensate for with returns. Therefore, I have a bias towards lower levels of beta. In the context of an entire portfolio, I can see the potential for benefits from using a small position in higher beta ETFs with free rebalancing to limit the amount of risk being created. Mixing it with SPY I also run comparisons on the standard deviation of daily returns for the portfolio assuming that the portfolio is combined with the S&P 500. For research, I assume daily rebalancing because it dramatically simplifies the math. With a 50/50 weighting in a portfolio holding only SPY and SPHB, the standard deviation of daily returns across the entire portfolio is 0.9359%. If we drop the position to 20% the standard deviation goes down to .8068%. In my opinion, that’s still too high. Once we drop it down to a 5% position the standard deviation is .7484%. I think 5% is about the largest position I’d consider here. Why I use standard deviation of daily returns I don’t believe historical returns have predictive power for future returns, but I do believe historical values for standard deviations of returns relative to other ETFs have some predictive power on future risks and correlations. Yield & Taxes The distribution yield is 0.88%. The ETF isn’t designed to cover the living expenses of retirees and in my opinion the risk level of the ETF combined with the low yield should encourage retirees to only consider positions even smaller than 5%. With the right level of diversification the ETF can still be used, but it isn’t built to meet those needs. I’m not a CPA or CFP, so I’m not assessing any tax impacts. If I were using SPHB, I would want it to be in a tax exempt account to remove any headaches associated with frequent rebalancing. Expense Ratio The ETF is posting .25% for an expense ratio. I want diversification, I want stability, and I don’t want to pay for them. In my opinion, a .25% expense ratio is higher than I want to pay for equity investments. It’s still low relative to many other methods of investing, but I’m looking for long term holdings and I don’t want to give my investments away. Market to NAV The ETF is at a .03% premium to NAV currently. In my opinion, that’s not worth worrying about. It is practically trading right on top of NAV. However, premiums or discounts to NAV can change very quickly so investors should check prior to putting in an order. Largest Holdings The portfolio is very well diversified. Despite my lack of interest in holding higher beta portfolios, I still appreciate the great level of diversification. The top holding is barely over 1.5% of the portfolio. That is great. Check out the chart below: (click to enlarge) Conclusion I’m currently screening a large volume of ETFs for my own portfolio. The portfolio I’m building is through Schwab, so I’m able to trade SPHB with no commissions. I have a strong preference for researching ETFs that are free to trade in my account, so most of my research will be on ETFs that fall under the “ETF OneSource” program. At this point I’m a little skeptical, but I’ll have to test the impacts of the ETF in a heavily diversified portfolio. If I do include SPHB, it will probably be a position of 5% or less. The most likely result is that I will decide to exclude SPHB from my portfolio. Scalper1 News

Summary I’m taking a look at SPHB as a candidate for inclusion in my ETF portfolio. The risk level makes me uncomfortable for anything over 5%. The ETF is very well diversified, just not into the kind of companies I want to hold. I’m not assessing any tax impacts. Investors should check their own situation for tax exposure. Investors should be seeking to improve their risk adjusted returns. I’m a big fan of using ETFs to achieve the risk adjusted returns relative to the portfolios that a normal investor can generate for themselves after trading costs. I’m working on building a new portfolio and I’m going to be analyzing several of the ETFs that I am considering for my personal portfolio. One of the funds that I’m considering is the PowerShares S&P 500 High Beta Portfolio (NYSEARCA: SPHB ). I’ll be performing a substantial portion of my analysis along the lines of modern portfolio theory, so my goal is to find ways to minimize costs while achieving diversification to reduce my risk level. What does SPHB do? SPHB attempts to track the total return of the S&P 500® High Beta Index. At least 90% of funds are invested in companies that are part of the index. SPHB falls under the category of “Mid-Cap Blend”. Does SPHB provide diversification benefits to a portfolio? Each investor may hold a different portfolio, but I use (NYSEARCA: SPY ) as the basis for my analysis. I believe SPY, or another large cap U.S. fund with similar properties, represents the reasonable first step for many investors designing an ETF portfolio. Therefore, I start my diversification analysis by seeing how it works with SPY. I start with an ANOVA table: (click to enlarge) The correlation is about 86%. It is low enough to provide some diversification benefits relative to holding SPY, but the benefits won’t be huge so if the standard deviation of returns is too high it may still be difficult to fit SPHB into a portfolio. Standard deviation of daily returns (dividend adjusted, measured since January 2012) The standard deviation is terrible. For SPHB it is 1.1739%. For SPY, it is 0.7300% for the same period. SPY usually beats other ETFs in this regard, but that is a very high standard deviation. Granted, it should be assumed that a high beta portfolio would have a high standard deviation of returns. Under CAPM (Capital Asset Pricing Model) the level of expected return should be easily determined by the beta of the stock. I think high beta stocks frequently more risk than they compensate for with returns. Therefore, I have a bias towards lower levels of beta. In the context of an entire portfolio, I can see the potential for benefits from using a small position in higher beta ETFs with free rebalancing to limit the amount of risk being created. Mixing it with SPY I also run comparisons on the standard deviation of daily returns for the portfolio assuming that the portfolio is combined with the S&P 500. For research, I assume daily rebalancing because it dramatically simplifies the math. With a 50/50 weighting in a portfolio holding only SPY and SPHB, the standard deviation of daily returns across the entire portfolio is 0.9359%. If we drop the position to 20% the standard deviation goes down to .8068%. In my opinion, that’s still too high. Once we drop it down to a 5% position the standard deviation is .7484%. I think 5% is about the largest position I’d consider here. Why I use standard deviation of daily returns I don’t believe historical returns have predictive power for future returns, but I do believe historical values for standard deviations of returns relative to other ETFs have some predictive power on future risks and correlations. Yield & Taxes The distribution yield is 0.88%. The ETF isn’t designed to cover the living expenses of retirees and in my opinion the risk level of the ETF combined with the low yield should encourage retirees to only consider positions even smaller than 5%. With the right level of diversification the ETF can still be used, but it isn’t built to meet those needs. I’m not a CPA or CFP, so I’m not assessing any tax impacts. If I were using SPHB, I would want it to be in a tax exempt account to remove any headaches associated with frequent rebalancing. Expense Ratio The ETF is posting .25% for an expense ratio. I want diversification, I want stability, and I don’t want to pay for them. In my opinion, a .25% expense ratio is higher than I want to pay for equity investments. It’s still low relative to many other methods of investing, but I’m looking for long term holdings and I don’t want to give my investments away. Market to NAV The ETF is at a .03% premium to NAV currently. In my opinion, that’s not worth worrying about. It is practically trading right on top of NAV. However, premiums or discounts to NAV can change very quickly so investors should check prior to putting in an order. Largest Holdings The portfolio is very well diversified. Despite my lack of interest in holding higher beta portfolios, I still appreciate the great level of diversification. The top holding is barely over 1.5% of the portfolio. That is great. Check out the chart below: (click to enlarge) Conclusion I’m currently screening a large volume of ETFs for my own portfolio. The portfolio I’m building is through Schwab, so I’m able to trade SPHB with no commissions. I have a strong preference for researching ETFs that are free to trade in my account, so most of my research will be on ETFs that fall under the “ETF OneSource” program. At this point I’m a little skeptical, but I’ll have to test the impacts of the ETF in a heavily diversified portfolio. If I do include SPHB, it will probably be a position of 5% or less. The most likely result is that I will decide to exclude SPHB from my portfolio. Scalper1 News

Scalper1 News