Portfolio Strategy For Someone Just Starting Out

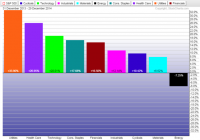

Summary This article is meant for folks who are just starting out in stock investing. It focuses on how to make a beginner’s portfolio, which is well diversified, relatively safe, but at the same time offers flexibility, a learning curve and room for growth. There are other simpler and passive alternatives, like buying a few diversified ETFs, but if you like to invest in individual stocks, please read on. This article is not for everyone. I know a vast majority of Seeking Alpha readers are by and large mature investors, considering how often we see a healthy debate in the comments section. But then there are others who are just starting out and not sure how to approach investing. It could be someone fresh out of college who just started working, or someone in their early 30s (or even later) who never thought of investing until now. The first-time investor often does not know where to start. Should they invest all of their capital at once, or should they invest over time? How much do they really need to save to have a diversified portfolio and how many stocks should they invest in? Most folks, who are just starting out, will buy few random stocks based on some article or tip, without a plan. Once they have bought a few stocks, they have no long-term or exit strategy either. This article will focus on the importance of a strategy, even when you are starting out with a relatively small amount of capital and how to form a starter portfolio. Where to start: First things first. a) Determine how much money you want to invest: How much do you want to start with and how much you are going to contribute on going-forward basis? I always prefer a staggered approach to investing. – Initial Capital – Monthly contribution b) Determine your risk profile: It will depend on your age, type of job/ employment you are in, your emergency funds situation and most importantly, your risk-tolerance (% of investment capital you can afford to lose in a worst case scenario). Based on all these factors, put yourself into one of these categories – High-risk, above-average risk, moderate risk, low-risk or extreme conservative. For the last category, though, investing in individual stocks is not advised. c) Decide on a brokerage company: There are several to choose from in terms of deposit requirements, features, trading commissions and fees. Some examples are Fidelity, TD Ameritrade, E*Trade, TradeKing, Interactive Brokers, Scottrade etc. If your account size is small (less than $10,000), you would probably be better off with an ultra-low commission broker like Interactive Brokers. d) What kind of account you would want to open: This depends on your overall goals and factors like, how long can you afford to keep this money locked in? The account-types can be a simple individual taxable brokerage account, or a retirement type account like an IRA or Roth-IRA. The IRA or Roth-IRA accounts come with certain restrictions like yearly contribution limits and income limits. Also, there are restrictions as to when and under what circumstances you can withdraw from an IRA account without penalty prior to the age of 59½. Most brokerage firms list them when you attempt to open an account. Be sure you are aware of them or read them carefully. e) Write your investment goals: Yes, write them. You can choose whichever medium you would like, paper or electronic. But please, write your short-term and long-term goals for the investment portfolio you are about to start. If you are still with me, let’s begin: We will assume that you are starting out with at least $5000 (or more) and then will add some money every month to bring your first year total investment capital to $10,000. Divide your money in four buckets of 25% each. – We will call the first bucket as “Core.” – The 2nd bucket will be “Income” bucket. – The 3rd will be “Growth.” – Lastly the 4th bucket will simply be called “Cash.” This will be the money sitting in cash most of the time. 1. “CORE” Bucket: Depending upon the size of your bucket, this money should be invested in “Dividend Champions” or “Dividend Aristocrats.” The best place to start is the list called Dividend Champions maintained by SA contributor “David Fish.” This list consists of over 100 well known companies who have paid and increased dividends for at least 25 years. Some well known examples are Coca-Cola (NYSE: KO ), ExxonMobil (NYSE: XOM ), Johnson & Johnson (NYSE: JNJ ), Procter & Gamble (NYSE: PG ) etc. You could also look at the Dividend Aristocrats that are S&P500 constituents and have paid growing dividends for 25 consecutive years. If your investment money in this bucket is only $2,500, you could still buy 4 or 5 individual stocks ($500 or $600 each), provided your trading commission is minimal (say $1 per trade). If your brokerage charges $5 or more, you will be restricted to fewer companies to keep your trading costs low. 2. Income Bucket: Why income? Some might argue, “Why should someone who is just starting out care for income from the investment portfolio?” There are a couple of important reasons why I am suggesting this. First, this will allow us to diversify into alternative assets like REITs, MLPs, Bonds and Munis etc., which typically offer higher yields than the ordinary stocks, including the dividend paying stocks like JNJ, KO, PG etc. Second, the income stream can either be reinvested in the same securities to compound or accumulated to invest into new stocks. Thirdly, it adds more stability (less volatility) to the portfolio. Lastly, let’s face it – everyone likes income; it simply adds to the motivation. Below are just some examples for further research. These are not recommendations, but just a place to start your own research. REITs (Real Estate Investment Trust): Realty Income (NYSE: O ), HCP, Inc. (NYSE: HCP ), Cohen & Steers Total Return Reality (NYSE: RFI ) MLPs: Kayne Anderson MLP Investment (NYSE: KYN ), Duff & Phelps Select Energy MLP fund (NYSE: DSE ) One can choose individual MLPs, but one should be aware of the tax implications. Bond/Utility/Munis/ Preferred funds: PIMCO Dynamic Credit (NYSE: PCI ), PIMCO Dynamic Income (NYSE: PDI ), Nuveen Muni High Inc (NYSEMKT: NMZ ), Cohen & Steers Infrastructure (NYSE: UTF ), iShares US Preferred Stock (NYSEARCA: PFF ) High Yield Div Stocks: AT&T (NYSE: T ) Verizon (NYSE: VZ ) It may be best to choose one name from each of the categories above. 3. Growth Bucket: This is your money to invest in “growth,” or even somewhat speculative names, based on your individual experience, age, comfort level and risk profile. Just make sure your position sizes are small. For example, if the bucket size was $2500, do not invest more than $500 in any one stock. Basically, this is the money you can use to develop your learning curve. This is not the “buy and hold” bucket, so don’t be afraid to trade a little more frequently. Don’t be shy to sell when you can realize substantial profits. However, before you invest, always keep in mind your risk-profile, small position-sizing and due diligence. Below is one rather relatively safe strategy that you can deploy in a Bull Market. However, this will not work very well in a prolonged downturn. This is also called “momentum” trading. Every 4 to 6 months, pick the 3 most favored sectors (ETFs) of the market during the previous 3 months, and invest equal amounts in each of them. Repeat the process every 3 to 6 months. For example, in the last 3 months, the most favored sectors have been Consumer Staples, Healthcare and Technology. 4. CASH Bucket: This is your 25% cash position. In practical terms, this will vary between 15 to 20% of the total portfolio. Ideally, in a late Bull Market like we have today, this bucket should be overflowing, whereas in a downturn it can be used selectively to make good use of the opportunities that the market may offer (this means loaning money to other 3 buckets). As soon as it falls below 10-15%, a conscious effort should be made to bring it back to 20-25% level by way of diverting dividends/income or by adding fresh money. Now let’s see how well this portfolio will fare based on certain parameters: Safety: Investing can never be risk-free. However, we can manage the risk, by diversifying into different type of assets. Our (above) portfolio will have almost 50% of the capital in Cash and Core stocks. Another 25% is in alternative assets to some degree. This will provide the relative safety and low volatility during a down market. Growth: For anyone who is just starting out, “growth” is very important. Some would argue that for early stage investing (especially younger folks), 90-100% of the money should be invested in growth stocks. Theoretically this may be true, but it is easier said than done. Most folks do not have tolerance for high volatility and large drawdowns (the kind we saw in 2008) and they often end up exiting the market at just the wrong time. In contrast, this portfolio strategy is focused on investing discipline and asset diversification. The 25% cash position will provide the confidence to face any serious downturn, as it will provide opportunities to buy good companies at discounted prices. In addition, the CORE bucket should provide significant growth over a long period of time, assuming the dividends are re-invested. The 25% growth-bucket will provide better growth with time as the investor gets over the learning curve and becomes more experienced. Risks: The first risk is of course the market risk, which is true with any investment. Secondly, if you happen to invest at the tail end of the Bull Market, you are likely to face some headwinds. But one can only know this in hindsight. One way to mitigate this risk is to stagger your investments over a period of time. If you plan to contribute a regular amount on a monthly basis, this will automatically stagger your purchases. The third risk is that this portfolio is likely to underperform in a raging Bull Market (like we saw in 1990s or even in 2013), but at the same time, this will outperform in a down or sideways market. Concluding Remarks: For some, this strategy may look a little complicated for a small portfolio. However if your plan is long term and you would like to grow this into a large portfolio with regular contributions and portfolio growth, I believe this is the right approach. There are, of course, simpler and passive alternatives like buying a few diversified ETFs and these would be perfectly fine for someone who has no time or interest to study and research individual stocks. However, if you want to be an active investor, you need to have a strategy. I believe any strategy is better than none at all, since investing based on a well-defined strategy forces the investor to be more disciplined. The strategy outlined above is not perfect or complete by any means. Over time, as you develop your skills, you can make improvements and make it perform better to suit your individual temperament and needs. Full Disclaimer: The information presented in this article is for informational purposes only and in no way should be construed as financial advice or recommendation to buy or sell any stock. Every effort has been made to present the data/information accurately; however, the author does not claim 100% accuracy.