IHD: A Tough Sell Based On Performance

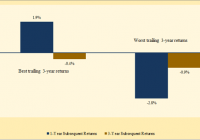

Summary IHD invests in emerging markets, which has been a tough market of late. That said, it offers investors a large yield. The problem is the yield is eating away at the CEF’s NAV. The Voya Emerging Markets High Dividend Equity Fund (NYSE: IHD ) is an interesting closed-end fund, or CEF, for those seeking an emerging market play. Essentially, it allows you to add a high-yield investment ( around 11% ) in emerging markets, a key asset allocation basket, to your portfolio. That’s not easy to find. For example, The Vanguard Emerging Markets Stock Index Fund (MUTF: VEIEX ) is yielding around 2.65% based on trailing distributions. But, IHD’s income comes at a cost you may not be willing to pay. What it does IHD’s objective is total return from a mixture of dividends, capital gains, and capital appreciation. It invests, as its name suggests, in emerging market equities. Typically, the portfolio will hold between 60 and 120 securities. On top of that, IHD will sell options on as much as 50% of the portfolio’s value. The options can be on individual stocks but also on indexes and exchange traded funds. Presumably that’s to increase the opportunities for option writing since options on some holdings may not exist or be liquid enough to trade. When looking for stocks, IHD starts with filters based on dividend yield and liquidity to create a universe from which to select individual holdings. It then takes the top-ranked stocks from this list and does fundamental research, evaluating such things as dividend sustainability and growth potential. At the end of the day, IHD is looking to create a portfolio of attractively valued companies with sustainable dividend yields and the potential for growth. The fund’s expenses aren’t outlandish at around 1.4%, according to the Closed-End Fund Association. The fund is, after all, providing active management in areas of the world that are often difficult to invest in, let alone find information about. You probably couldn’t do what they do, even if you wanted to. And that’s before trying to sell options. What about performance So far so good, but… the fund’s performance is middling at best. According to Morningstar, IHD’s trailing three-year annualized net asset value, or NAV, return through January of -1.3% falls at about the 65th percentile of its diversified emerging markets category grouping. Note that Morningstar’s figures include the reinvestment of dividends. The broader category effectively broke even over that span and Vanguard Emerging Market Index Fund posted an annualized gain of roughly 0.75%. So, IHD’s performance is a little below par, but a fat 11% yield might entice you to overlook this fact. That would likely be a mistake here. When IHD came public in early 2011, its NAV was $19.06 a share. The CEF’s NAV fell consistently through February of last year (its fiscal years end in February), bringing the NAV down to $12.50 a share. Sure it paid distributions of around $4 a share over that time, but the NAV decline was precipitous. The NAV is currently around $11.50 a share, which means it’s still going down. You’ll need a rally To be fair, emerging markets haven’t been the most hospitable place to invest in recent years. But this is clearly a case where the large dividend is doing a disservice to shareholders. That’s particularly true if you are using those distributions to live off of. Worse, you’d still be losing money even if you reinvested those distributions. I could go into the fund’s discount (roughly 8%, notably below the fund’s three-year average of about 3%), its country allocations (China is its largest weighting at 20% of assets), sector allocations (finance is around 30% of the portfolio), and individual holdings, but at this point all of that pales in comparison to the distribution’s impact on NAV. Even the chance of the discount closing isn’t particularly enticing in my book compared to the NAV issue. I would avoid IHD unless you think emerging markets are on the verge of a major bull market. That’s the only way you’ll likely see the NAV turn higher. Disclosure: The author has no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) The author wrote this article themselves, and it expresses their own opinions. The author is not receiving compensation for it (other than from Seeking Alpha). The author has no business relationship with any company whose stock is mentioned in this article.