Niska Gas Is Likely Undervalued Currently

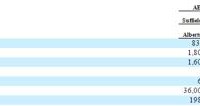

Summary NKA is being sold at a heavy discount to book value and free cash flows based on historical financial analysis. NKA will likely do quite well financially during the current volatile gas price environment. Even if NKA decides to cut dividends, the current price seems very attractive. Investors should not take a large position currently in the case that dividends are cut and the units become even more attractively priced. Niska Gas Storage Partners LLC (NYSE: NKA ) is a company that operates gas storage assets totaling roughly 250 Bcf of natural gas storage capacity in certain areas of North America. Being in the storage industry, the effects of supply and demand in the natural gas industry may not affect NKA the same way as it affects other oil and natural gas concerns. While natural gas supply is relatively stable over the short term, demand may fluctuate quite a lot due to seasonal, weather or other reasons. Therefore, storage assets can be useful when prices are unduly low and used to save gas supplies for when prices rebound to higher levels. There are a few ways that NKA protects itself from the fluctuations in gas prices or perhaps more importantly, fluctuations in the usage of storage facilities by gas and utility companies. Storage might be thought of as a hedge against price volatility and therefore, it may even benefit from exceptionally low gas prices than normal. The company enters into long-term firm (LTF) contracts in which customers pay the company monthly reservation fees for the right to use the storage facilities over a multi-year agreement. These LTF fees must be paid regardless of the actually utilization of storage capacity by the customers. Then there are variable fees that are charged based on usage of the facilities but they represent a very small portion of the fees received under LTF contracts. Therefore, on a qualitative live, the greater part of NKA’s revenue stream should be relatively stable and constant under most circumstances regardless of the direction of gas prices. The extraordinary situation would be if the supply of natural gas were to actually become in danger of being disrupted or if NKA’s customers were to experience financial failure on a large scale. This would put severe stress on the company’s revenue stream and thus severely cripple its ability to service debt. This scenario would happen if gas prices stay below profitability levels for the producers over a prolonged period of time. In the short term, it may even positively impact NKA’s profitability as low prices would beckon more usage of storage capacity. (click to enlarge) NKA’s largest operation is in Alberta with a facility in each of Suffield and Countess which act as a single hub known as the AECO hub. The weighted average contract life of LTF storage contracts in the AECO hub was 2.3 years as of March 31, 2014. As long as those customer companies manage to stay solvent, NKA’s revenues from AECO should be able to weather a fairly long period of low oil prices. Especially since the fact that TransCanada, a large customer of NKA re-implemented its contract making the weighted average life 4.2 years. The weighted average contract life of the LTF storage contracts at Wild Goose is 2.0 years. Salt Plains is 3.0 years. While LTF contracts comprise of the larger part of NKA’s total revenues, they also have Short Term Firm (STF) contracts which also accounts for a material part of their revenues. The company uses a combination of LTF, STF and other revenue optimization techniques to obtain as high an amount of revenue as possible depending on the market situation. The nature of LTF contracts is that the revenue stream is set during the window of when the contracts expire and is renegotiated for the years going forward. Thus, the revenue from this stream have little to do with the day to day fluctuations of the gas markets and is determined by the conditions prevailing when the contract is being renegotiated. The STF contracts are negotiated on an opportunistic basis and this source is more susceptible to the shorter term fluctuations of the greater market. The current scenario The poor performance in the recent quarter was largely due to the inability of the company to find attractive STF contracts. This is partially attributable to the fact that there has been a lack of energy price volatility due to a moderately cool summer in the areas served by NKA. The trend has now reversed and storage capacity will likely be in high demand due to the recent fallout in oil and gas prices. NKA’s facilities will be in short supply when producers become very uncertain about the future prospects of oil prices since storage capacity basically acts as limited type of insurance protection against uncertain prices. In that sense, although I never like to depend on predictions for the future, NKA’s future prospects for both STF and LTF contracts are looking very bright at the moment. The greater the spread in energy prices, the more valuable will be NKA’s storage assets. Restrictive ownership structure The company is effectively controlled by its sponsor HoldCo and there really isn’t any effective control given to the general public shareholders. Furthermore, the company states that if the manager or any of their affiliates own 80% more of the outstanding units, then they have the right to purchase all of the remaining units from the public unit holders at the prevailing market price. This makes holding NKA very unattractive if you were to have paid the full price of $16.00 for the units. However, at $4.00 per unit, the potential risk is much lower and the reward potential is much greater and more attractive. Should the controlling sponsors decide to acquire the entire outstanding units, there is far less risk of selling it for lower than your acquisition price when purchased at $4.00 per unit. Financial analysis Reviewing the historical performance of NKA, it would seem that the current market cap of around $140 million is unduly cheap. The cash available for distribution metric that NKA discloses should be a rough approximation of free cash flow to equity. If we take the year over year results so far, the stock is trading at merely two times free cash flow. The stock was roughly $16.00 per share and has now dropped to less than $4.00 per share based only on one quarter of poor results due to a shortfall in STF business. The company pays out $1.40 in dividends per year which amounts to roughly $51 million in total. The 2nd quarter call conference suggested that the dividend may be reduced or cut altogether going forward which is what caused the collapse in share price. Analyzing the historical financial data along with the current drop in prices, NKA appears to be extremely cheap at the moment not only due to the free cash flow record, but it also trades at such a small fraction of book value. (click to enlarge) Conclusion Even if the dividends were to be cut completely, I believe the unit price should still be worth roughly $6.00 per share when taking into consideration all the risks. Indeed, the share price will likely drop if dividends were to be cut but the fundamentals of the company are sound and should even do quite well under the current volatile oil and gas price regime. The investment is certainly a portfolio of depreciating assets and the maintenance capital expenditures will increase to roughly $10 million per annum going forward. However, this will not affect the fundamental cash flows to equity going forward to warrant a 70-80% drop in the price. There is ample protection in terms of discount to book value as well as the historical free cash flow performance to warrant a small purchase for me at the current prevailing market price. I’ve only taken on a small position because I want to have a lot of dry powder left over if they should actually cut the dividend and the price would fall further. However, I believe that at the current price, NKA is attractive even if it does cut its dividends.