Complete List Of 79 ETP Closures For 2014

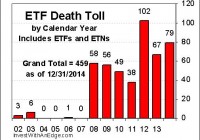

Seventy-nine exchange traded products bit the dust in 2014, marking the second highest annual death toll in the history of the ETF industry. The 72 ETF and 7 ETN closures were second only to the 102 closures of 2012. Broken down by major categories, the closures of 2014 consisted of 22 sector, 15 style and strategy, 14 global and international, 13 bond, 7 inverse, 4 leveraged, and 4 commodity. Of the 2,121 U.S. ETPs launched since the dawn of the industry in 1993, only 1,662 remain listed while 459 have closed. Said another way, the historic probability of ETP survivability is 78.4%. Closures affected 15 brands and sponsors in 2014. Pax World was the only sponsor to exit the ETF space completely, and it did so in a very strange fashion. ETF pundits have long discussed the possibility of a large quantity of mutual funds converting to ETFs. However, no one ever thought conversions might go the other direction, but that is exactly what happened when all $64 million of the assets in the Pax MSCI EAFE ESG Index ETF (NYSEARCA: EAPS ) suddenly became Institutional Class shares of the Pax World International ESG Index Fund (MUTF: PXNIX ), a traditional mutual fund. See ‘ This Wasn’t Supposed To Happen: ETF Converts To Mutual Fund ‘ for additional details. Goldman Sachs is highly regarded on Wall Street, and it is often thought of as a firm that can do no wrong when it comes to making money. However, it hasn’t figured out the ETF space yet. Goldman (NYSE: GS ) attached its name and investment strategies to four ETFs sponsored by ALPS in 2012. Apparently, the Goldman name carries no weight in ETF land , and all four ETFs closed in 2014 with combined assets of less than $11 million. For a number of reasons, the most notable closures of the year belong to iShares. First, 29 iShares ETFs had their last day of listed trading in 2014, giving iShares a 37% market share of closures. No other brands came close to this figure, with Direxion and EGShares tying for second-place “honors” with just six closures each. Second, iShares raised the bar on ETF survivability , as its 18 closings in October averaged more than $18 million in assets and two had about $70 million each. At the time, 49% of all listed ETFs and ETNs had fewer assets. Third, two of the liquidated funds (NY and NYC) had been on the market more than ten years. Longevity does not assure survival. Last, I can recall a BlackRock (NYSE: BLK ) representative questioning why there were iShares funds on ETF Deathwatch when none had ever closed. I reminded him that iShares practically invented ETF closures with three such occurrences in 2002. He rebutted that Barclays owned the iShares brand at that time, and BlackRock had never closed an ETF. Never say never. Some ETPs have maturation dates, namely target-date maturity bond ETFs and all ETNs. At their time of launch, these products inform investors of their likely closure and liquidation dates. For example, the Guggenheim BulletShares series of target maturity bond ETFs retire a couple of funds at the end of each calendar year. The two 2014 BulletShares ETFs (BSCE and BSJE) had their last day of trading on December 30, and next year we can expect the 2015 funds (BSCF and BSJF) to do the same. These are planned from the time of inception and are not indicative of unhealthy or failing products. Every ETN is also issued with a maturity date. Typically, ETNs are launched with 30-year or 20-year maturities. Since the first ETNs didn’t come to market until 2006, most investors thought they wouldn’t have to deal with ETN maturation for another 10 or 20 years. However, in 2009 there were five ETNs issued as 5-year notes scheduled to mature in 2014. Three of these five triggered early terminations, including Barclays ETN+ S&P 500 Short B ETN (NYSEARCA: BXDB ) last April. The two that escaped early termination, BXUC and BXUB, matured in November and were liquidated. Most of 2014’s closures had become Zombie ETFs, and 58 of the 79 (73%) were on ETF Deathwatch at the time of their closure announcements. The major exceptions included the maturing products discussed above and many of the iShares with large amounts of assets. The average age of funds that closed in 2014 was 45.8 months (3.8 years). This is greater than the 31.4-month average lifespan of all 459 closed products, suggesting sponsors are willing to subsidize these non-profitable products longer than in years past. The table below is currently sorted by product name. # Ticker Name Last Day Deathwatch Notes 1 GSAX ALPS/GS Momentum Builder Asia x-Japan Eq/US-T 08/27/2014 Yes 2 GSGO ALPS/GS Momentum Builder Growth Markets Eq/US-T 08/27/2014 Yes 3 GSMA ALPS/GS Momentum Builder Multi-Asset 08/27/2014 Yes 4 GSRA ALPS/GS Risk-Adjusted Return U.S. Large Cap 08/27/2014 Yes 5 BXUB Barclays ETN+ S&P 500 Long B Leveraged ETN 11/20/2014 Yes 2 6 BXUC Barclays ETN+ S&P 500 Long C Leveraged ETN 11/20/2014 – 2 7 BXDB Barclays ETN+ S&P 500 Short B Leveraged ETN 04/10/2014 Yes 3 8 BRZS Direxion Daily Brazil Bear 3x Shares 09/23/2014 Yes 9 EURZ Direxion Daily FTSE Europe Bear 3x Shares 09/23/2014 Yes 4 10 BARS Direxion Daily Gold Bear 3x Shares 12/26/2014 Yes 4 11 JPNS Direxion Daily Japan Bear 3x Shares 09/23/2014 Yes 12 GASX Direxion Daily Natural Gas Related Bear 3x 09/23/2014 – 13 KORZ Direxion Daily South Korea Bear 3x Shares 09/23/2014 Yes 14 CHXX EGShares China Infrastructure 09/29/2014 Yes 15 EMDG EGShares Emerging Markets Dividend Growth 12/24/2014 Yes 16 EMHD EGShares Emerging Markets Dividend High Income 12/24/2014 Yes 17 IEMF EGShares TCW EM Intermediate Term IG Bond 09/29/2014 Yes 4 18 LEMF EGShares TCW EM Long Term IG Bond 09/29/2014 Yes 4 19 SEMF EGShares TCW EM Short Term IG Bond 09/29/2014 Yes 4 20 OFF ETRACS Fisher-Gartman Risk Off ETN 05/18/2014 Yes 21 ONN ETRACS Fisher-Gartman Risk On ETN 05/18/2014 Yes 22 GASZ ETRACS Natural Gas Futures Contango ETN 01/22/2014 – 23 OILZ ETRACS Oil Futures Contango ETN 01/22/2014 Yes 24 CNPF Global X Canada Preferred 10/16/2014 Yes 25 GGGG Global X Pure Gold Miners 10/16/2014 Yes 26 BSCE Guggenheim BulletShares 2014 Corp Bond 12/30/2014 – 2 27 BSJE Guggenheim BulletShares 2014 HY Corp Bond 12/30/2014 – 2 28 GIY Guggenheim Enhanced Core Bond 03/07/2014 Yes 1 29 MUAC iShares 2014 AMT-Free Muni Term 08/15/2014 – 2 30 NUCL iShares Global Nuclear Energy 10/14/2014 Yes 31 FNIO iShares Industrial/Office Real Estate Capped 10/14/2014 Yes 32 AXDI iShares MSCI ACWI ex US Consumer Discretionary 03/25/2014 Yes 33 AXSL iShares MSCI ACWI ex US Consumer Staples 03/25/2014 Yes 34 AXEN iShares MSCI ACWI ex US Energy 03/25/2014 Yes 35 AXFN iShares MSCI ACWI ex US Financials 03/25/2014 Yes 36 AXHE iShares MSCI ACWI ex US Healthcare 03/25/2014 Yes 37 AXID iShares MSCI ACWI ex US Industrials 03/25/2014 Yes 38 AXIT iShares MSCI ACWI ex US Information Technology 03/25/2014 Yes 39 AXMT iShares MSCI ACWI ex US Materials 03/25/2014 Yes 40 AXTE iShares MSCI ACWI ex US Telecom Services 03/25/2014 Yes 41 AXUT iShares MSCI ACWI ex US Utilities 03/25/2014 Yes 42 EMFN iShares MSCI Emerging Markets Financials 10/14/2014 Yes 43 EMMT iShares MSCI Emerging Markets Materials 10/14/2014 Yes 44 FEFN iShares MSCI Far East Financials 10/14/2014 Yes 45 NY iShares NYSE 100 ETF 10/14/2014 – 46 NYC iShares NYSE Composite ETF 10/14/2014 – 47 RTL iShares Retail Real Estate Capped 10/14/2014 Yes 48 TZD iShares Target Date 2010 10/14/2014 – 49 TZE iShares Target Date 2015 10/14/2014 – 50 TZG iShares Target Date 2020 10/14/2014 – 51 TZI iShares Target Date 2025 10/14/2014 – 52 TZL iShares Target Date 2030 10/14/2014 – 53 TZO iShares Target Date 2035 10/14/2014 – 54 TZV iShares Target Date 2040 10/14/2014 – 55 TZW iShares Target Date 2045 10/14/2014 Yes 56 TZY iShares Target Date 2050 10/14/2014 – 57 TGR iShares Target Date Retirement Income 10/14/2014 – 58 RKH Market Vectors Bank and Brokerage 12/12/2014 Yes 59 COLX Market Vectors Colombia 12/12/2014 Yes 60 GERJ Market Vectors Germany Small-Cap 12/12/2014 Yes 61 LATM Market Vectors Latin America Small-Cap 12/12/2014 Yes 62 CHLC Market Vectors Renminbi Bond 12/12/2014 Yes 63 EAPS Pax MSCI EAFE ESG Index ETF 03/21/2014 – 5 64 AUD PIMCO Australia Bond Index 09/26/2014 – 65 TRSY PIMCO Broad U.S. Treasury Index 03/10/2014 Yes 66 BABZ PIMCO Build America Bond 09/26/2014 – 1 67 CAD PIMCO Canada Bond Index 09/26/2014 – 68 BUND PIMCO Germany Bond Index 09/26/2014 Yes 69 PIQ PowerShares Dynamic Magniquant 02/18/2014 Yes 70 KBWX PowerShares KBW International Financial 02/18/2014 Yes 71 PXN PowerShares Lux Nanotech 02/18/2014 Yes 72 PMNA PowerShares MENA Frontier Countries 02/18/2014 Yes 73 GEMS PureFunds ISE Diamonds/Gemstone 01/23/2014 Yes 74 MSXX PureFunds ISE Mining Service 01/23/2014 Yes 75 NAGS Teucrium Natural Gas 12/18/2014 Yes 76 CRUD Teucrium WTI Crude Oil 12/18/2014 Yes 77 ASDR VelocityShares Emerging Asia DR ETF 11/20/2014 Yes 78 EMDR VelocityShares Emerging Markets DR ETF 11/20/2014 Yes 79 RUDR VelocityShares Russia DR ETF 11/20/2014 Yes Notes: 1) actively managed, 2) reached planned maturity, 3) hit early termination trigger, 4) launched in 2014 and less than 1 year old at time of closure, 5) converted to mutual fund. All exchange traded notes are identified with “ETN” as part of their name description. Disclosure covering writer, editor, publisher, and affiliates: No positions in any of the securities mentioned. No positions in any of the companies or ETF sponsors mentioned. No income, revenue, or other compensation (either directly or indirectly) received from, or on behalf of, any of the companies or ETF sponsors mentioned.