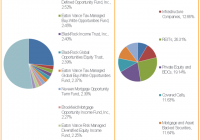

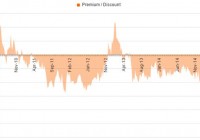

Summary Wave of investor outflows has created a significant dislocation. This provides an opportunity for those constructive on the Chinese market to obtain cheap exposure. For the rest of us, it also presents some potential to capture alpha through pair trades. Background on Closed-End Funds For those new to the space, a closed-end fund is a publicly traded investment company that raises a fixed amount of capital, and is then structured, listed and traded like a stock on a stock exchange. Whereas conventional mutual funds and ETFs frequently redeem/issue new shares to ensure that the price per share remains in line with the net asset value of the underlying holdings in the funds, this is not the case for CEFs. Rather the share price of CEFs is driven by the market forces of supply and demand, and can at times trade at either large discounts or premiums to NAV of the funds’ actual holdings. The Morgan Stanley China A Share Fund (NYSE: CAF ) is currently trading at one of the widest discounts in the CEF universe, due to a classic supply/demand imbalance. In particular, the Western media has inundated investors recently with headlines concerning the risks of a Chinese economic slowdown coupled with a potential bubble in the local equity market nearing its peak. The result is that the supply of CAF shares flooding the market from investors rushing to sell has overwhelmed demand, causing this CEF to now trade for a whopping ~20% below its NAV. In other words, for every $1 of net assets in the fund, investors now only need to pay ~80 cents to buy shares. (click to enlarge) Source: CEF Connect Morgan Stanley China A Share Fund Overview CAF is a reasonably large/liquid fund, with ~$936 million of total net asset value. The fund’s mandate is to invest at least 80% of its assets in A-shares of Chinese companies listed on the Shanghai and Shenzhen Stock Exchanges. Morgan Stanley is a longstanding/reputable CEF manager and the 3 executive/managing directors overseeing the fund each have more than a decade of experience in the Chinese market. The fund has a moderate annual expense ratio of 1.8%, and is currently relatively concentrated as shown in the table below. Also, the cash balance is now quite elevated (representing ~16% of NAV), which I view as a meaningful positive – after all, it’s hard to argue that cash in the hands of a reputable manager deserves a big discount. Plus, it gives the manager ammunition to take steps like share buybacks in the future to reduce the discount. Top 10 Holdings as of 5/31/15 % Of Portfolio Cash 16.1 Tsingtao Brewery Co., Ltd. Class A 10.0 China Resources Sanjiu Medical & Pharmaceutical Co., Ltd. Class 9.6 Industrial & Commercial Bank of China Ltd. Class A 8.7 Qingdao Haier Co., Ltd. Class A 5.2 China Pacific Insurance Group Co., Ltd. Class A 5.1 GoerTek, Inc. Class A 5.0 China Merchants Bank Co., Ltd. Class A 4.9 Kweichow Moutai Co., Ltd. Class A 4.4 Zhongbai Holdings Group Co., Ltd. Class A 3.7 Total 72.7 Source: Morgan Stanley CAF’s investor base is reasonably concentrated, with institutions holding approximately 37% of shares outstanding. Notably, Lazard holds ~$117mm or ~16% of total shares outstanding. This is also something I like to see when considering investing in a CEF that trades at a discount to NAV, as institutions holding major stakes are more likely than small individual/retail holders to pressure management to take steps to narrow the discount if this does not occur naturally over time. Source: NASDAQ So, What’s the Trade? For investors that want exposure to the local Chinese equity market, this CEF appears to be an attractive vehicle that is likely to deliver alpha from the discount reverting to more normalized levels over time. For others that have a more cautious view on the Chinese market (myself being one), there are also some potential opportunities to capture this alpha through pairing a long position in CAF with a short position in a Chinese equity ETF. There are several possible shorts to consider, but I present a couple below. CSOP FTSE China A50 ETF (NYSEARCA: AFTY ): This is a relatively small ETF with approximately $135mm of net assets. However, trading volume is reasonable, with ~$2.6mm/day in shares trading on average over the past 3 months. It is also currently relatively easy to borrow, with a cost under 2% through some retail brokers. The fund typically invests at least 80% of its total assets in the securities included in the FTSE China A50 index. This index is comprised of A-shares issued by the 50 largest companies in the China A-shares market. Direxion Daily FTSE China Bull 3X Shares ETF (NYSEARCA: YINN ): This alternative has more basis risk, but could also have the potential to produce more alpha. The fund has ~$181mm of net assets, with average daily trading volume of ~$20mm. YINN is not overly difficult to borrow, with a cost under 5.5% through some retail brokers currently. YINN seeks daily investment results, before fees and expenses, of 300% of the performance of the FTSE China 50 Index. This index consists of 50 of the largest and most liquid Chinese stocks (H Shares, Red Chips and P Chips) listed and trading on the Stock Exchange of Hong Kong, and is therefore a less tight match with CAF’s A share holdings. However, a potential benefit of shorting YINN is that one may benefit from the general tendency of levered ETFs to underperform over longer periods of time. There are several reasons for their underperformance including what is often referred to as a “leverage trap” (i.e., their tendency to decay in mean reverting markets from being forced to buy high/sell low), as well as elevated expenses that result from the higher trading activity needed to maintain these vehicles. The phenomenon is discussed in much more depth in academic literature (such as in this article ), as well as elsewhere on Seeking Alpha (such as here ). Risks/Considerations The main risk of this trade is that the timing of discount convergence is unclear, and if investors’ macro fears over China grow, there is a possibility that the discount could increase even further over the near term. The main mitigants are the facts that, as discussed above, the investor base is relatively concentrated with institutional investors, and the fund manager is reputable with dry powder in the form of excess cash to reduce the discount if it persists over time. Short selling of course also comes with added risks (e.g., possibility of force buy-ins, increasing borrow costs, etc.) and likely should not be attempted by those new to the market. Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in CAF over the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.