How To Find The Best Style Mutual Funds: Q2’15 In Review

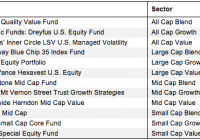

Summary Finding the best mutual funds is an increasingly difficult task in a world with so many to choose from. Performance of a mutual fund’s holdings equals the performance of the fund. Our coverage of mutual funds leverages the diligence we do on each stock by rating mutual funds based on the aggregated ratings of their holdings. Finding the best mutual funds is an increasingly difficult task in a world with so many to choose from. How can you pick with so many choices available? Don’t Trust Mutual Fund Labels There are at least 904 different Large Cap Value mutual funds and at least 6391 mutual funds across twelve styles. Do investors need 500+ choices on average per style category? How different can the mutual funds be? Those 904 Large Cap Value mutual funds are very different. With anywhere from 17 to 1003 holdings, many of these Large Cap Value mutual funds have drastically different portfolios, creating drastically different investment implications. The same is true for the mutual funds in any other style, as each offers a very different mix of good and bad stocks. Large Cap Value ranks first for stock selection. Small Cap Blend ranks last. Details on the Best & Worst mutual funds in each style are here . A Recipe for Paralysis By Analysis We firmly believe mutual funds for a given style should not all be that different. We think the large number of Large Cap Value (or any other) style mutual funds hurts investors more than it helps because too many options can be paralyzing. It is simply not possible for the majority of investors to properly assess the quality of so many mutual funds. Analyzing mutual funds, done with the proper diligence, is far more difficult than analyzing stocks because it means analyzing all the stocks within each mutual fund. As stated above, that can be as many as 1003 stocks, and sometimes even more, for one mutual fund. Any investor worth his salt recognizes that analyzing the holdings of a mutual fund is critical to finding the best mutual fund. Figure 1 shows our top rated mutual fund for each style. Figure 1: The Best Mutual Fund in Each Style Sources: New Constructs, LLC and company filings How To Avoid “The Danger Within” Why do you need to know the holdings of mutual funds before you buy? You need to be sure you do not buy a fund that might blow up. Buying a fund without analyzing its holdings is like buying a stock without analyzing its business and finances. No matter how cheap, if it holds bad stocks, the mutual fund’s performance will be bad. PERFORMANCE OF FUND’S HOLDINGS = PERFORMANCE OF FUND If Only Investors Could Find Funds Rated by Their Holdings The Eaton Vance Hexavest U.S. Equity Fund (MUTF: EHUIX ) is the top-rated Large Cap Value mutual fund and the overall best fund of the 6391 style mutual funds that we cover. The worst mutual fund in Figure 1 is the Royce Special Equity Fund (MUTF: RSEIX ), which gets our Neutral rating. One would think mutual fund providers could do better for this style. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.