Will Iran Keep USO Down?

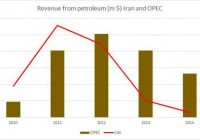

Iran’s potential nuclear deal could bring up its output in the coming years. Will this deal have a long-term impact on oil market and the price of USO? U.S. oil production keeps rising despite low rig count. The potential nuclear deal between Iran and the West, which could lift the sanctions on the country, has contributed to the decline in the price of The United States Oil ETF, LP (NYSEARCA: USO ) – the oil ETF lost over 6% on Monday and over 10% in the past month. Moreover, the weakness in China, high volatility in the foreign exchange markets over the Greek debt crisis and low oil rig counts in the U.S. also provided additional downward pressure on USO. But is Iran likely to have such a strong impact on the price of USO over the coming years? Despite the sharp rise in volatility in the oil market, the price of USO hasn’t deviated by much from the price of oil in the past couple of months – the roll decay due to the Contango wasn’t harsh. If the futures oil market keeps a low Contango or even move to backwardation, this could behoove USO investors. But the main problem remains on whether oil prices were to bounce back from its recent plunge. One factor to consider is the role of Iran in the oil market. As the EIA showed , Iran’s ability to resume its pre-sanctions oil output on the conditions of the oil fields and infrastructure – it could take time and investment to bring these fields online. Nonetheless, the potential impact of Iran’s higher output could result in low oil prices by $5 to $15 next year. These projections could be a bit too harsh considering the market conditions are harder to increase production and OPEC already exceeds its current quota. Also, the country is likely to face challenges and a more competitive oil market environment. Some of these challenges include rising oil yield of U.S. oil producers, slower growth in demand for oil in China, growing share of Saudi Arabia from OPEC’s total output, and stronger competition from Russia, which heavily relies on oil revenue and continues to face a weak currency. The market conditions have also cut down the oil exports (in U.S. dollar) of OPEC in general and Iran in particular in the past year. As I have already pointed out in the past, and based on OPEC statistical bulletin , in 2014, OPEC’s revenue from petroleum exports have gone down to $964 billion – a 12.6% fall, year on year. For Iran the revenue from output also declined, mainly between 2012 and 2013 on account of its sanctions. (click to enlarge) Source of data taken from OPEC So the potential end of the sanctions on Iran could bring back up the country’s oil revenue, even though, as presented above, the fall in revenue of OPEC also suggests it will be harder to increase oil exports in the current market conditions. Currently, Iran produces around 2.8 million barrels per day. Back in 2011, before the sanction, the country was able to produce roughly 3.6 million bbl/day – 28% higher than in 2015. Last year, it produced 3.1 million bbl per day of which only 1.1 million bbl/day were exported or 35% of total output. Over the next couple of years, assuming the sanctions are lifted, Iran could increase its total output by 700,000 bbl/day, according to the EIA . Considering the country’s energy demand keeps rising, the county is likely to partly use this added output towards its own energy needs. In the meantime, the output in the U.S. hasn’t contracted, despite the fall in rig counts in the past few months. Oil producers have also reduced their capex for 2015 and in some cases for 2016. But for now, the output hasn’t contracted and the EIA still projects the annual output will remain around 9.4 million bbl per day – only 2% lower than the current output level. (click to enlarge) Source of data taken from EIA and Baker Hughes Looking forward, the EIA estimates production will fall further in 2016 to 9.3 million bbl per day. The fall in output in the coming months could also bring back up oil prices or at the very least ease the downward pressure on oil prices. Even though Iran’s role in the oil market is very important and could have an adverse impact on the price of oil and USO, its impact could actually be less prominent considering the current market conditions and the country’s energy demands. (For more please see: ” USO Investors – Beware of The Contango! “) Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.