3 Small Cap Value ETFs For Every Type Of Investor

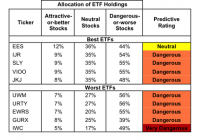

I’ve surveyed the small cap ETF universe and found 3 ETFs I like. I narrowed them down for aggressive investors, conservative investors and average investors. Each ETF has a reasonable expense ratio and is broadly diversified. I am a value investor, meaning I look for stocks that the market hasn’t discovered yet or that are out of favor for some reason. My favorite area for value stocks is the small-cap arena. My best picks over the years have been those that started as small-caps and grew due to their success. It’s these overlooked stocks whose stories I like that I spend most of my time on. However, I can’t spend all my time on them, and that’s why I’ve been hunting down 3 small-cap ETFs to share with aggressive investors, conservative investors, and the average investor. Why own a small-cap ETF? Other than the fact that small-cap stocks have historically outperformed their larger brethren and offer the best chances of obtaining a multi-bagger return, you must have diversification in your portfolio. Sector outperformance occurs all the time, and the more diversification you have, the better. If you don’t have diversification, then you risk seeing your overall portfolio fall more in bad times by having your money overly concentrated. For the aggressive investor, consider the WisdomTree SmallCap Earnings ETF (NYSEARCA: EES ) . This may sound like a silly criteria, but this ETF only invests in earnings generating small-cap companies. Sure, an aggressive investor may not care if a company is generating earnings or not, but I’d argue that’s only true of GROWTH stocks. Value stocks need to be making money to be a value play. EES happens to be a fundamentally weighted index fund, taking the smallest 25% of companies in the universe of profitable small-cap companies, after removing the 500 largest companies. Since the weighting is earnings based, the companies with the largest profits get weighted the most heavily. Now, let’s be sure the ETF is defining “earnings” as what we’d expect it to. The ETF refers to “core earnings,” as defined by Standard & Poor’s, to include expenses, income and activities that reflect the actual profitability of the company. So that’s just fine by me. It’s also broadly diversified with 957 holdings and, as I’d hope for in a small-cap fund, 90% of them are under $2 billion in market cap. Sure enough, even this fund has a 26% weighting in financials, with 18% in industrials, 18% in consumer discretionary, 12% in IT, 9.5% in health care, 6% in energy and 4% in materials. I consider EES to be for the aggressive investor because it is quasi-actively managed. The assumption is that actively managed funds will be a bit more aggressively directed because investors assume management is designed to outperform. That doesn’t necessarily mean there will be greater risk, but that’s often the case. Since its inception on 2/23/07, the fund’s total returns have been 53%, and it has been outperforming its benchmark in the most recent 3-year and under periods. A basic small-cap value ETF choice for the average investor is always going to be found in the Vanguard family of funds. In this case, I look at the Vanguard Small Cap Value ETF (NYSEARCA: VBR ) . Vanguard’s approach toward value securities is to evaluate them based on price-to-book, forward earnings-to-price, historical earnings-to-price, dividend-to-price and sales-to-price ratios. It is a passively managed fund that carries 843 stocks, and the top 10 only account for 4.8% of the total asset base. I like that kind of broad diversification, and like the weighting even more. Financials account for 30.7%, industrials are 20%, consumer services at 13%, technology comes in at 7%, consumer goods is also at 7%, health care at 7%, and energy at 4%. I consider Vanguard for the average investor since it seeks to mirror the benchmark with low fees. Nothing special here. It has essentially matched the Russell 2000 Value index for a 37% return since February 2007. It has a 114% total return over the past ten years, and 104% over the past five years. For the more conservative investor, the iShares Russell 2000 Value ETF (NYSEARCA: IWN ) . This $5.61 billion market cap ETF was launched in 2000, so there’s a long enough track record for me to evaluate it as being appropriate for this class of investor. It is very well diversified with 1,314 holdings. The ETF basically takes the Russell 2000 index and pulls out companies that have value characteristics in the broadest possible sense. The average price-to-earnings ratio is 14.19, which is quite a bit lower than in recent months, making it particularly attractive. Financials account for 43% of the ETF, which is a bit more than I’d like, but the vast number of holdings offsets it to some degree. Industrials account for 12%, consumer discretionary comes in at 10.74%, information technology at 10.25%, utilities at 7%, materials at 3%, energy at 4.6% and the rest falls into health care, consumer staples and derivatives. As a conservative fund, it aims for true value plays so that downside risk is limited, but upside gains can take longer to develop. For example, it only has a 12% return since February of 2007. However, it has a 172% return over fifteen years. As with any article regarding investments, you should never rely on information you read without doing your own due diligence. My articles contain my honest, forthright and carefully considered personal opinion, and conclusions, containing information derived from my own research. This may include discussions with management. I do not repeat “talking points” but may quote management from an interview. I am never influenced by third parties in arriving at my conclusions. Do not solely rely on my articles or anyone else’s when making an investment decision. Always contact your financial advisor before investing in any security. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.