Will A Fidelity Select Funds Portfolio Perform Well In A Rising Interest Rates Environment?

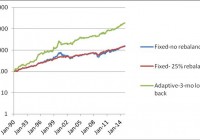

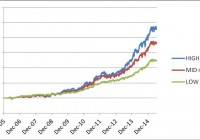

Summary Old portfolio: FBMPX, FSCHX, FSELX, FSPHX, FGMNX. New portfolio: FBMPX, FSCHX, FSELX, FSPHX, FIBIX, FSBIX. The new portfolio significantly outperforms the old one. In a previous article , we presented the performance of a portfolio made up of five Fidelity select mutual funds. That portfolio had a stellar performance over the whole 27-year period from 1987 to 2015, but we are concerned about its performance in a stock bear market within a rising interest rate environment. To increase its robustness for such events, we decided to replace the GNMA fund (MUTF: FGMNX ) with two high-quality government bonds. The portfolio is made up of the following funds: Fidelity Select Multimedia Portfolio No Load (MUTF: FBMPX ) Fidelity Select Chemicals Portfolio No Load (MUTF: FSCHX ) Fidelity Select Electronics Portfolio No Load (MUTF: FSELX ) Fidelity Select Medical Delivery Portfolio No Load (MUTF: FSHCX ) Fidelity Spartan Intermediate Trust Bond Index Fund Inv (MUTF: FIBIX ) Fidelity Spartan Short Term Trust Bond Index Fund Inv (MUTF: FSBIX ) Our old portfolio performed very well during the two big bear markets of 2000-03 and 2008-09. During those markets, the portfolio was invested mostly in the GNMA fund that experienced growth due to declining interest rates associated with economic contraction. But if a stock bear market happens while interest rates are rising, the GNMA fund most likely would not offer protection. We expect that a short-term government bond would allow the portfolio capital to be preserved during such adverse market environments. Due to their low sensitivity to interest rates, the short-term Treasury bonds act mostly as cash. Basic information about the funds was extracted from Yahoo Finance and is shown in the table below. Table 1 Symbol Inception date Net assets Yield% Category FSELX 7/29/1985 2.32B 0.47% Technology FBMPX 6/30/1986 803M 0.24% Consumer Cyclical FSPHX 7/14/1981 10.75B 1.90% Health FSCHX 7/29/1985 1.47B 1.02% Natural Resources FIBIX 12/20/2005 1.35B 1.90% Intermediate Term Treasuries FSBIX 12/20/2005 863M 0.76% Short Term Treasuries Since the historical price data of the bond funds is available only from December 2005 on, and we need 65 trading days for estimating market parameters, we were able to simulate our optimal allocation strategy starting with April 2006. We performed an analysis of the difference in performance of the old and the new portfolios. The data for the study were downloaded from Yahoo Finance , using the Historical Prices menu for FGMNX, FBMPX, FSCHX, FSELX, FSPHX, FIBIX, and FSBIX, respectively. We use the daily price data adjusted for dividend payments. The portfolio is managed as dictated by a variance-return optimization algorithm developed on the Modern Portfolio Theory ( Markowitz ). The allocation is rebalanced monthly at market closing of the first trading day of the month. In table 2 below, we present the performance of the new portfolio for three levels of risk. Table 2. Portfolio performance from April 2006 to June 2015 TotRet% CAGR% No. of trades maxDD% VOL% Sharpe Sortino Low risk 247.96 14.41 112 -8.02 8.81 1.63 2.27 Medium risk 363.25 18 108 -9.86 12.35 1.46 2.01 High risk 457.9 20.39 94 -13.26 15.01 1.36 1.9 SPY 91.37 7.26 0 -55.18 20.98 0.35 0.41 In figure 1, we show the graphs of the portfolio equities. (click to enlarge) Figure 1. Equity curves for three portfolios adaptively optimized for low-, medium- and high-risk targets. Source: This chart is based on EXCEL calculations, using the adjusted monthly closing share prices of securities. In figure 2 below, we show the time variation of the percentage allocation of the funds for medium risk. (click to enlarge) Figure 2. Asset allocations for the new portfolio adaptively optimized for the medium risk target Source: This chart is based on EXCEL calculations, using the adjusted monthly closing share prices of securities. In figure 2, it can be observed that during the bear market of 2008-09, most money was allocated to the intermediate-term bond fund, FIBIX. During the market corrections of 2010 and 2011, most money was allocated to the short-term bond fund, FSBIX. The current fund allocations are shown in table 3. Table 3. Asset allocations for July 2015 FSELX FBMPX FSPHX FSCHX FIBIX FSBIX Low risk 30% 70% 0% 0% 0% 0% Medium risk 0% 100% 0% 0% 0% 0% High risk 0% 100% 0% 0% 0% 0% We also simulated the performance of the old portfolio over the same time period from April 2006 to June 2015 and for the same risk levels. Consistently over the whole simulation period, the new portfolio outperformed the old one by about a 40% increase in annual returns and a 20% or more decrease in maximum drawdown. We compared the returns of the portfolios over the bear market of 2008 and the market corrections of 2010 and 2011. The results are shown in table 4. Table 4. Total returns of the portfolios during market downturns Time Period SPY Old Portfolio New Portfolio 12/2007 – 3/2009 -48.92 -11.08% 9.74% 3/2010 – 7/2010 -10.95 -5.75% -0.30% 4/2011 – 9/2011 -16.22 -1.59% 15.51% From table 4, it is clear that the new portfolio performs better than the old one, and that it is very robust to market downturns. Unfortunately, there were no long enough periods of rising interest rates to allow us to make any judgment about the behavior of the portfolios during such times. It is our belief that in a long period of rising interest rates, the new portfolio will suffer only small losses by parking the money in the short-term bond fund. Conclusion The modified Fidelity portfolio performed significantly better than the old one. It even made gains during the 2008 bear market and the 2011 market correction. While there is no empirical data to prove it, we believe that the new portfolio is robust and will perform well even during a prolonged period of rising interest rates. Disclosure: I am/we are long FSELX, FSPHX. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.