Tag Archives: alaska

Avista’s (AVA) CEO Scott Morris on Q4 2015 Results – Earnings Call Transcript

Operator Welcome to the Q4 2015 Avista Corporation Earnings Conference Call. My name is Cynthia, and I will be your operator for today’s call. At this time, all participants are in a listen-only mode. Later, we will conduct a question-and-answer session. Please note that this conference is being recorded. I will now turn the call over to Jason Lang, Investor Relations Manager. Mr. Lang, you may begin. Jason Lang Thank you, Cynthia, and good morning, everyone. Welcome to Avista’s fourth quarter and fiscal year 2015 earnings conference call. Our earnings and our 2015 Form 10-K were released pre-market this morning, now both available on our website at avistacorp.com. I have just have been informed that there are some issues going on with the webcast right now. So if you are having issues, they are trying to fix that. And also we will have a replay of this call, and so you’ll be able to see the slide then. Joining me this morning are Avista Corp. Chairman of the Board, President and CEO, Scott Morris; Senior Vice President and CFO, Mark Thies; Senior Vice President and the President of Avista Utilities, Dennis Vermillion; and the Vice President, Controller and Principal Accounting Officer, Ryan Krasselt. I would like to remind everyone that some of the statements that will be made today are forward-looking statements that involve assumptions, risks and uncertainties, which are subject to change. For reference to the various factors, which could cause actual results to differ materially from those discussed in today’s call, please refer to our Form 10-K for 2015 which is available on our website. To begin this presentation, I would like to recap the financial results presented in today’s press release. Our consolidated earnings for the fourth quarter of 2015 was $0.61 per diluted share compared to $0.51 for the fourth quarter of 2014. Results for the fourth quarter of 2015 included $0.07 per diluted share and the fourth quarter of 2014 included $0.03 per diluted share related to discontinued operations, which resulted from the sale of Ecova in 2014. For the full-year, consolidated earnings were $1.97 per diluted share for 2015, compared to $3.10 last year. Results for 2015 included $0.08 per diluted share and 2014 included $1.17 per diluted share related to discontinued operations, which resulted from the sale of Ecova in 2014. Now, I’ll turn the discussion over to Scott. Scott Morris Well, thank you, Jason, and good morning, everyone. We had a strong year and I’m pleased with our financial and operating performance in 2015. We made significant progress in achieving our goals of investing in our infrastructure, upgrading our technology, and preparing our utility to effectively and efficiently serve our customers. In 2015, weather played a significant role in our operations. On November 17, an historic windstorm occurred in our service territory, which caused severe damage to our electrical system. Included in our 2015 results are cause for power restoration of $22.9 million for capital repairs and $2.9 million for incremental utility operating and maintenance costs. I would like to take this opportunity to say thank you, again, to everyone involved in the storm restoration effort. This was a monumental task that took thousands of hours to complete, and I’m extremely proud of the way the company, the community, and our contract and mutual aid crews rallied together to make this historic recovery possible. Thankfully, we were able to restore power without one single safety incident. Turning back to the financial results, our Juneau operations at AEL&P had a strong year, and as a results met our expectations. We’re very pleased with how the company is performing. Now, I’d like to give you an update on the additional business opportunities we’re working on in Alaska. As we discussed in our last call, we have made progress in our evaluation of bringing natural gas to Juneau. Currently, we believe that lower, excuse me, lower oil prices may make it more difficult for our customers to justify converting to natural gas. In addition, we have yet to secure a mechanism to provide funds that are needed to help customers with the conversion costs, thus challenging the economics of the project. We will continue to engage the community with the opportunity and evaluate the project. We will keep you updated each quarter on our progress. In addition, our subsidiary Salix was notified by Alaska Industrial Development and Export Authority in December 2015 that has proposal to build an LNG liquefaction plant to serve the interior energy project, specifically to serve Fairbanks, Alaska, was selected as one of two finalists, a decision by the AIDEA Board is expected in the first quarter of 2016. With respect to regulatory matters in December, the Idaho Commission approved an all-party settlement in our Idaho electric and natural gas general rate cases that resulted in new rates beginning January 1. The Idaho agreement includes electric and natural gas decoupling mechanism similar to Washington. In January, the Washington Commission issued an order that concluded our electric and natural gas rate cases that were originally filed with the UTC in February of 2015. New electric and natural gas rates were effective on January 11. Subsequent to the UTC order approving our new rates, three motions were filed by interested parties for the UTC to consider. On February 19, the UTC issued an order denying those motions filed by the interested parties and affirmed their original January order approving new rates. Also, on February 19, we filed electric and natural gas general rate cases in Washington, primarily to cover increased capital costs, the request for an 18-month rate plan. As for Oregon, we continue to work through the general rate case process related to our case filed in 2015. I’m pleased to report that earlier this month, Avista’s Board of Directors raised the quarterly common stock dividend by 3.8%. This marks the 14th consecutive year the Board has raised the dividend for our shareholders. And lastly, I believe we are well-positioned to continue our long-term earnings growth. We’re initiating our 2016 earnings guidance with a consolidated range of $1.96 to $2.16 per diluted share. So at this time, I’m going to turn the call over to Mark. Mark Thies Thank you, Scott. Good morning, everyone. And consistent with past practice, I do try to wear a jersey during these calls. So today I have my Peyton Manning jersey on honor of his and the Broncos, more the Broncos defense win in the Super Bowl. So for 2015, Avista utilities contributed $1.81 per diluted share, which is down slightly from $1.83 last year. The 2015 earnings per share decreased primarily due to weather that was warmer than normal in the first and fourth quarters. And that was all partially offset by decoupling mechanisms in Washington. We do expect to have decoupling mechanisms, as Scott mentioned for 2016 in Washington and Idaho, and we requested that mechanism in Oregon. We also had higher operating expenses, depreciation and amortization, and taxes other than income all of which were expected. During the fourth quarter of 2015, Avista Utilities contributed $0.51 per diluted share, compared to $0.45 in 2014. Those earnings increased primarily due to a general rate increase in Washington, and this was partially offset by decreased heating loads, as I mentioned due to warmer weather and an increase for provision for earning sharing and all of the weather was offset by decoupling mechanisms. We continue to be committed, as Scott mentioned to updating and maintaining our utility systems. We expect Avista Utilities capital expenditures to be about $375 million in 2016, and we expect about $17 million at AEL&P in 2016. A significant portion of AEL&P’s capital are for construction of an additional backup generation plant that is expected to be completed in 2016. I’ll turn to liquidity and financing plans now. As of December 31, there were – we had $105 million of cash borrowings and $45 million of letters of credit outstanding leaving $250 million of available liquidity under our committed line of credit. There were no borrowings or letters of credit outstanding as of 12/31 under AEL&P’s line. In December of 2015, we issued $100 million of 30-year first mortgage bonds for Avista Corp. In 2016, we expect to issue about $155 million of long-term debt and approximately $55 million of common equity in order to fund our capital expenditures and maintain a prudent capital structure. As Scott mentioned, we’re initiating our 2016 guidance for consolidated earnings to be in the range of $1.96 to $2.16 per diluted share. We expect Avista Utilities to contribute in the range of $1.91 to $2.05 per diluted share. Our range for Avista Utilities encompasses the expected variability and power supply costs and the application of the ERM to that power supply cost variability. The midpoint of our guidance does not include any benefit or expense under the ERM. In 2016, we currently expect to be in a benefit position with the ERM within the $4 million dead-band. Our outlook for Avista Utilities assumes, among other variables, normal precipitation, temperatures, hydroelectric generation for the remainder of the year, and includes the expected impact from decoupling. We estimate that our 2016 Avista Utilities guidance range encompasses a return on equity of approximately 8.6% at the bottom end of the range to 9.2% at the top end of the range. For 2016, we expect AEL&P to contribute in the range of $0.09 to $0.13 per diluted share. Our outlook for AEL&P assumes, among other variables, normal precipitation, and hydroelectric generation for the remainder of the year. We expect our other businesses to be between a loss of $0.04 and a loss of $0.02. That includes the costs associated with exploring strategic opportunities. As always, our guidance generally includes only normal operating conditions and does not include unusual items such as settlement transactions, impairments or acquisitions or dispositions until the effects are known. So I’ll now turn the call back to Jason. Jason Lang Thank you, Mark. Cynthia, we’d now like to open up the call up for questions. Question-and-Answer Session Operator Thank you. We will now begin the question-and-answer session. [Operator Instructions] And our first question comes from Michael Weinstein with UBS. You may begin. Michael Weinstein Hi, guys. How are you doing? Scott Morris Good morning, Mike. Mark Thies Good morning, Mike. Michael Weinstein Good morning, good morning. I was wondering if – so I guess for the – with the low-end of the dead-band around the ERM, you’re expecting up to $4 million of earnings, but you’re not expecting to go into the sharing areas at this point? Scott Morris [Multiple Speakers] Michael Weinstein Yes. Scott Morris Go ahead, Mike. I’m sorry. Michael Weinstein I was wondering, if you could tell what the hydro levels are at this moment? Scott Morris Well, currently the hydro levels, look, okay for us, as of February 22. So Monday, the Northwest River Forecast Center shows the water supply or the runoff from April through September, for the Clark Fork River at 86%, and the Spokane River is at 80%. And remember that on an average annual basis, we get about roughly 75% of our generation from the Clark Fork River. So, we’re in pretty good shape I think right now. And you also need to remember that we from this point in time probably have, at least, six good weeks of high-level of snow accumulation possible. So winter is not over at the higher elevation, so a lot of things can change between now and then . Michael Weinstein All right. Have the temperatures been unusually cold or warm? I know I think two years ago, it was very cold, so there wasn’t a lot of melt and the ERM was in a low – a very high – let’s see in 2014, it was a very low position for first quarter. And in 2015, it was in a very high position because of its heavy melt. I was wondering if which one of those kinds of conditions seem to be shaping up this year? Scott Morris Well, we have had warmer temperatures as of late. If you have been following our snowpack, it has come down somewhat over the last couple of weeks. And largely that’s the lower elevation snow, so that’s not unusual. As we start to see spring weather come in, the lower elevation obviously goes first. One of the other key things to remember is the price of natural gas being so low in our – in the Pacific Northwest that, that’s a significant benefit to our overall generation fleet as well. So the impacts of lower than normal generation aren’t felt as much basically. Mark Thies And Mike just to be clear, I’m not sure. I thought you said, we’re at the low-end of the range. We expect to be in a benefit position under the ERM for 2016, just to clarify that in case you’re thinking of what the other way. We expect to be in a benefit for the year within the $4 million dead-band. Michael Weinstein Yes, that’s what I meant, low-end of the benefit side. The new rate case that you just filed in Washington state, that’s going to be – is this the first time you’ve filed a multi-year rate case? Scott Morris No, a couple of years ago, we filed in 2012 – in 2012, we filed for 2013 and 2014, in both Idaho and Washington. And in both of those cases, we did get a two-year rate plan. The last one, the one we filed before was just a one year, and so then this one is an 18-month plan. So it’s not outside of the realm of normal or possibility. We just have to work with the commission on that and the staff and all the parties. Michael Weinstein Do they help you with regulatory lag? Any structural regulatory lag eliminated from that? Scott Morris I don’t think, it has any impact necessarily on regulatory lag. It helps us to get a longer-term plan, so we’re not having back-to-back rate cases. Michael Weinstein Right. And just one last question before I give it to somebody else. Could you talk a little more about Juneau, and I guess more about the timing of when you think you might get or of the ability to make decisions there and what’s going on with the LNG import? Scott Morris Well, I’ll let Dennis weigh in here, because Dennis has done a tremendous job working with the Alaska communities to make this happen. But I just think a lot of it has to do quite frankly with market conditions. You see where oil prices are. We want to be prudent and smart about going to Juneau with oil under $30 a barrel. And with our LNG prices right now it’s about a break-even on a conversion costs and we have some work to do to make sure that our customers up there could have an opportunity to convert to natural gas, if we do choose to go in a way that is cost effective for them. So, Dennis, has a couple of plans. He is working on there. So I would just say that we’re still optimistic. It’s just some timing issues. And we’re going to be prudent and smart about it. And, yes, Dennis, I’ll let you kind of take it from there. Dennis Vermillion Well, that’s a good summary, Scott. The only thing I would really add also is, we continue to work with the local elected folks and state officials. And I’m sure you’re aware that just the overall budget situation for the state of Alaska with the price of oil, we have some pretty serious budget issues that they’re dealing with. So a lot of the focus and attention is elsewhere right now, as they try to wrestle with some of those issues that they’re dealing with. $30 oil is not a good thing. It’s a good thing if you’re a consumer yet, but for the state it has created quite a bit of problem. So we’re continuing to work through that as well and want to make sure that our plans are solid and lasting before we decide to move forward. Michael Weinstein All right, great. Thank you very much, guys. Scott Morris Thanks, Mike. Operator [Operator Instructions] Scott Morris So do we have any other question, Cynthia. Operator We have no further questions at this time. I will now turn the call back over to Jason Lang for closing remarks. Jason Lang I’d like to thank everyone for joining us today. We certainly appreciate your interest in our company. Have a great day. Operator Thank you, ladies and gentlemen. This concludes today’s conference. Thank you for participating. You may now disconnect. Copyright policy: All transcripts on this site are the copyright of Seeking Alpha. However, we view them as an important resource for bloggers and journalists, and are excited to contribute to the democratization of financial information on the Internet. (Until now investors have had to pay thousands of dollars in subscription fees for transcripts.) So our reproduction policy is as follows: You may quote up to 400 words of any transcript on the condition that you attribute the transcript to Seeking Alpha and either link to the original transcript or to www.SeekingAlpha.com. All other use is prohibited. THE INFORMATION CONTAINED HERE IS A TEXTUAL REPRESENTATION OF THE APPLICABLE COMPANY’S CONFERENCE CALL, CONFERENCE PRESENTATION OR OTHER AUDIO PRESENTATION, AND WHILE EFFORTS ARE MADE TO PROVIDE AN ACCURATE TRANSCRIPTION, THERE MAY BE MATERIAL ERRORS, OMISSIONS, OR INACCURACIES IN THE REPORTING OF THE SUBSTANCE OF THE AUDIO PRESENTATIONS. IN NO WAY DOES SEEKING ALPHA ASSUME ANY RESPONSIBILITY FOR ANY INVESTMENT OR OTHER DECISIONS MADE BASED UPON THE INFORMATION PROVIDED ON THIS WEB SITE OR IN ANY TRANSCRIPT. USERS ARE ADVISED TO REVIEW THE APPLICABLE COMPANY’S AUDIO PRESENTATION ITSELF AND THE APPLICABLE COMPANY’S SEC FILINGS BEFORE MAKING ANY INVESTMENT OR OTHER DECISIONS. If you have any additional questions about our online transcripts, please contact us at: transcripts@seekingalpha.com . Thank you!

Avista Corp.: A 4% Yield With 4% Dividend Growth

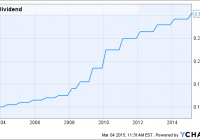

Currently, the shares sport a yield of 3.97%. For the last 13 years, the company has increased its dividend. Avista anticipates continuing to grow its dividend by 4-5% annually. My search for safe high-yield plays continues, and has brought me upon Avista Corp. (NYSE: AVA ). The diversified utilities player is in a solid spot right now, and boy, does its dividend look attractive. Avista’s operations consist of generation, transmission, and distribution of electricity in the Northwest US and Alaska. It’s common knowledge that utilities are a fairly stable sector, and this is one of the main things that drew me to Avista. A stable and safe industry is something I always look for in my search. The utilities sector, in particular, is my favorite place to search for good dividends, and with Avista, I believe I have found just that. AVA Dividend data by YCharts The company currently pays out a quarterly dividend of 33 cents a share. That gives the shares a yield of 3.97% at current levels. As can be seen from the chart above, Avista has seen 13 years of dividend growth, most recently raising it about 4% on February 6th. The payout ratio sits at about 68%, which, by my standards, is more than acceptable. Most of the time, I look for anything under 70%, and depending on the industry, up to 80% may be acceptable. 2014 was somewhat of a transitional year for the company. It sold off its indirect subsidiary Ecova, Inc. to Cofely USA for $335 million. On the other side of the spectrum, Avista closed a deal during the year to acquire Alaska Electric Light and Power Company. Both of these threw a twist on earnings for 2014. In total, the company actually reported earnings per share of $3.10 for the year. However, earnings for the year were actually $1.93 from continuing ops. The earnings from the continuing ops is what is important here, as that will be the comparison for this year. The company reported FY 14 and Q4 results on February 25th that missed the mark by a little. EPS came in at 51 cents versus the consensus of 55 cents. This was mostly due to the mild winter. In the release, CEO Scott Morris blamed the Q4 miss on the weather being warmer than last year and warmer than it typically is. Clearly, the weather is a factor for the company, but it can be seen from the slight miss that it does not effect earnings drastically. Going forward, the acquisition of Alaska ELP should be a near-term growth catalyst. The company only realized earnings from it for the second half of 2014, so it should be a nice boost already to 2015 results. Guidance has the segment contributing 8 to 12 cents to earnings this year. The company sees this segment as a opportune area of growth in the future, and I expect over the next few years, the results from this segment will improve greatly. The guidance the company has set for 2015 calls for EPS between $1.86 and $2.06. This is pretty broad, but the mid-point of $1.96 points to modest earnings growth of 1.55%. However, estimates from analysts have the company positing EPS of $1.98. A slow growth year is not a concern, as the long-term growth of earnings looks headed in the right direction. According to the company’s long-term plan, it seeing earnings and dividend growth of between 4-5% in the future. Finviz also estimates the 5-year long-term annual growth rate of earnings to be 5%. (Source: Avista Update ) Even with a fairly weak 2015, I would not be concerned in the slightest about dividend growth. Earnings over the next few years are still anticipated to grow nicely, and the dividend has plenty of room to grow with it. Another thing is that the shares look fairly attractive at these levels as well. The company is trading at just about 17 times earnings, which is a good bit lower than its peers. Excluding the outliers, the average among domestic diversified utilities is about 20 times earnings. Looking at this year, if Avista were to meet estimates, it will be trading at less than 17 times earnings. While it may not be grossly undervalued, compared with peers based on earnings the shares do appear a little undervalued. The shares are currently trading about 12% off their 52-week highs as well. In conclusion, I like Avista’s dividend a lot. It is somewhat of a less covered name, and it is important to note a good recent history of dividend increases. The company seems committed to this dividend growth, and the dividend should see about 4% annual growth over at least the next few years. Anyone looking for a safer high-yielding dividend growth play should definitely take Avista into consideration. Disclosure: The author has no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) The author wrote this article themselves, and it expresses their own opinions. The author is not receiving compensation for it (other than from Seeking Alpha). The author has no business relationship with any company whose stock is mentioned in this article. Additional disclosure: Always do your own research before investing.