Scalper1 News

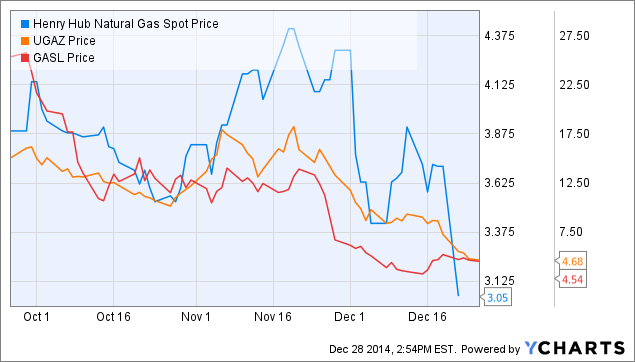

Summary As a young investor my portfolio is filled with risk. In 2015 I will be looking to limit my exposure to big risks. My portfolio was weighted heavily in oil and gas, which did not make for a pretty 2014. Thomas Jefferson once said “With great risk comes great reward.” This certainly is not always the case and my portfolio did most definitely did not agree with this statement in 2014. Since I’m quite young I can afford to have a large amount of risky plays in my portfolio which led to an interesting and ultimately dismal 2014. In 2015 I plan to, as best I can, de-risk my holdings, while still incorporating the right amount of risk for my age. A Few Current Positions For starters, in addition to covering the oil and gas sector heavily, my portfolio has been weighted toward the industry more than any other. You can imagine what this weight has done since the summer. One of my holdings in the industry is small cap Bakken producer Emerald Oil (NYSEMKT: EOX ). The company has operationally and financially improved dramatically since I first added shares but still remains an extremely risky play, especially with the current oil environment. I have averaged down on the name as the company has greatly scaled back its operations in this environment which should enable it to survive the downturn. On a different note, one of my other oil and gas names is a far less risky play. Gran Tierra Energy (NYSEMKT: GTE ) is a Canadian company with operations mainly in Colombia and Peru. The reason I say this is a significantly less risky play is the fact that at the end of Q3 the company continued to have no debt and $360M in cash. Its revised 2015 capex plan only calls for $310M. So while oil is at these depressed levels, Gran Tierra might just be in one of the best positions to ride it out. Along with that the company has several other catalysts. The company should announce soon, or with Q4/FY results, how the initial drilling in Peru is coming along. This will result in significant additions to the company’s reserves and ultimately will add a lot to its overall value. My only main concern with Gran Tierra while I have held it has been the ongoing conflict in Colombia. The FARC rebel group targets lots of infrastructure, including pipelines and rail lines which have in the past disrupted operations. This concern however has been quelled for the time being as the FARC announced a unilateral ceasefire that started December 20th. In 2015 I plan to maintain my current position in energy as I do not need to add more weight to my portfolio and to exit underwater positions would not make sense. Another risky portion of my portfolio includes a sizeable position in J.C. Penney (NYSE: JCP ). I’ve been playing the turnaround for some time now, and in the time I have held it the company has improved its quarterly results greatly. While I do believe in the turnaround working to some extent, depending on Q4 results, I may opt to close this position. Safer plays have become far more attractive than the troubled retailer, and I believe I’m ready to add more practical holdings. A position that I will most definitely be holding onto is Sirius XM (NASDAQ: SIRI ). I have held this position longer than any other, and it was in fact one of the first things I bought when I first began investing a few years ago. The company continues to perform well and I for one am a fan of the buybacks the company has been doing. Earlier in the year I was pleased that the deal with Liberty fell through because I see far greater upside without a buyout for a company with little comparable competition. One last higher risk name I also own is Synta Pharmaceuticals (NASDAQ: SNTA ). It is a small biotech that is engaged in many trials of various drugs, in particular its leading candidate, Ganetespib, which fights cancer. While obviously this further adds diversification to my holdings, Synta is only in trial stages of its drugs, and expects itself to have cash just through Q4 of 2015. This is worrisome because if the results from the trials in 2015 are poor it could see the shares free fall. Don’t get me wrong, I still believe in all of my current holdings. I’m just worried about how balanced I am between safer more reliable plays and high risk plays. In 2014 the market was quite good and that can be seen from the various indexes being up nicely. I’m sure you’ve heard the famous Warren Buffett quote a million times before but here it is once more: “Be fearful when others are greedy and greedy when others are fearful.” Now I can’t tell you where the market will go in 2015 and I’m not saying be fearful or greedy. I’m just highlighting the uncertainty and what my plans are for 2015. Positions I’m Considering When looking at my holdings going into 2015 I see one major problem that I want to fix: no companies I own pay dividends. I did for some time own Bank of America (NYSE: BAC ), but sold it part way through the year (a position in hindsight I wished I kept). My new strategy in 2015 will most definitely include a few and maybe many strong dividend payers. The first of which I am considering would be AT&T (NYSE: T ). With a 5.5% yield it is very enticing. The company continues to deliver some dividend growth announcing yet another increase a couple of weeks ago. I see the acquisition of DIRECTV (NASDAQ: DTV ), which is still pending, as a strong catalyst for further growth going forward. Another mega cap I’m considering is Pfizer (NYSE: PFE ). The company sports a 3.5% yield and also just announced that it was increasing its dividend yet again. In late October the company announced that it would buyback another $11 billion worth of its shares. A couple of other dividend paying names that I am considering adding include Flowers Foods (NYSE: FLO ), Ford (NYSE: F ), and Middlesex Water (NASDAQ: MSEX ). Some Risky Additions in 2015? Although I want to balance my holdings to safer plays that does not mean I won’t add some further risk to it. Over the past two weeks natural gas has been hammered and I see a possible very enticing risk vs. reward opportunity playing natural gas at these levels. This could turn out especially rewarding if we see bitter weather in late January or February. Henry Hub Natural Gas Spot Price data by YCharts Another position I may consider would be one in Twitter (NYSE: TWTR ). In 2015 the company is expected to become consistently profitable after many quarters of losses. The shares are trading 46% down from its 52 week high and the last time the shares were trading around this level they went on a 50% run. A short term catalyst for the shares may be the rumors that current CEO Dick Costolo may be canned. Costolo has lost investor confidence and replacing him could lead to a nice pop in the shares. Conclusion Being so young I can afford to have lots of risk and make mistakes (and learn from them). In 2015 I want to be more cautious and reasonable. Since beginning investing my holdings have always overwhelmingly been dominated by high risk names. To start 2015 I have saved enough to change this and will not only be adding more reliable and safe names, but will also be getting rid of some of the current risky names I hold. In particular I am going to add extremely financially sound companies that also pay dividends which should reward even if 2015 turns sour for the markets. Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks. Additional disclosure: Always do your own research before investing. Keep in mind that everyone, especially by age group, has different investment goals and aims. Most of my investments remain long term but I also dabble in short term trading occasionally. I may initiate long positions in T, PFE, UGAZ, GASL, F, FLO, MSEX, TWTR. Scalper1 News

Summary As a young investor my portfolio is filled with risk. In 2015 I will be looking to limit my exposure to big risks. My portfolio was weighted heavily in oil and gas, which did not make for a pretty 2014. Thomas Jefferson once said “With great risk comes great reward.” This certainly is not always the case and my portfolio did most definitely did not agree with this statement in 2014. Since I’m quite young I can afford to have a large amount of risky plays in my portfolio which led to an interesting and ultimately dismal 2014. In 2015 I plan to, as best I can, de-risk my holdings, while still incorporating the right amount of risk for my age. A Few Current Positions For starters, in addition to covering the oil and gas sector heavily, my portfolio has been weighted toward the industry more than any other. You can imagine what this weight has done since the summer. One of my holdings in the industry is small cap Bakken producer Emerald Oil (NYSEMKT: EOX ). The company has operationally and financially improved dramatically since I first added shares but still remains an extremely risky play, especially with the current oil environment. I have averaged down on the name as the company has greatly scaled back its operations in this environment which should enable it to survive the downturn. On a different note, one of my other oil and gas names is a far less risky play. Gran Tierra Energy (NYSEMKT: GTE ) is a Canadian company with operations mainly in Colombia and Peru. The reason I say this is a significantly less risky play is the fact that at the end of Q3 the company continued to have no debt and $360M in cash. Its revised 2015 capex plan only calls for $310M. So while oil is at these depressed levels, Gran Tierra might just be in one of the best positions to ride it out. Along with that the company has several other catalysts. The company should announce soon, or with Q4/FY results, how the initial drilling in Peru is coming along. This will result in significant additions to the company’s reserves and ultimately will add a lot to its overall value. My only main concern with Gran Tierra while I have held it has been the ongoing conflict in Colombia. The FARC rebel group targets lots of infrastructure, including pipelines and rail lines which have in the past disrupted operations. This concern however has been quelled for the time being as the FARC announced a unilateral ceasefire that started December 20th. In 2015 I plan to maintain my current position in energy as I do not need to add more weight to my portfolio and to exit underwater positions would not make sense. Another risky portion of my portfolio includes a sizeable position in J.C. Penney (NYSE: JCP ). I’ve been playing the turnaround for some time now, and in the time I have held it the company has improved its quarterly results greatly. While I do believe in the turnaround working to some extent, depending on Q4 results, I may opt to close this position. Safer plays have become far more attractive than the troubled retailer, and I believe I’m ready to add more practical holdings. A position that I will most definitely be holding onto is Sirius XM (NASDAQ: SIRI ). I have held this position longer than any other, and it was in fact one of the first things I bought when I first began investing a few years ago. The company continues to perform well and I for one am a fan of the buybacks the company has been doing. Earlier in the year I was pleased that the deal with Liberty fell through because I see far greater upside without a buyout for a company with little comparable competition. One last higher risk name I also own is Synta Pharmaceuticals (NASDAQ: SNTA ). It is a small biotech that is engaged in many trials of various drugs, in particular its leading candidate, Ganetespib, which fights cancer. While obviously this further adds diversification to my holdings, Synta is only in trial stages of its drugs, and expects itself to have cash just through Q4 of 2015. This is worrisome because if the results from the trials in 2015 are poor it could see the shares free fall. Don’t get me wrong, I still believe in all of my current holdings. I’m just worried about how balanced I am between safer more reliable plays and high risk plays. In 2014 the market was quite good and that can be seen from the various indexes being up nicely. I’m sure you’ve heard the famous Warren Buffett quote a million times before but here it is once more: “Be fearful when others are greedy and greedy when others are fearful.” Now I can’t tell you where the market will go in 2015 and I’m not saying be fearful or greedy. I’m just highlighting the uncertainty and what my plans are for 2015. Positions I’m Considering When looking at my holdings going into 2015 I see one major problem that I want to fix: no companies I own pay dividends. I did for some time own Bank of America (NYSE: BAC ), but sold it part way through the year (a position in hindsight I wished I kept). My new strategy in 2015 will most definitely include a few and maybe many strong dividend payers. The first of which I am considering would be AT&T (NYSE: T ). With a 5.5% yield it is very enticing. The company continues to deliver some dividend growth announcing yet another increase a couple of weeks ago. I see the acquisition of DIRECTV (NASDAQ: DTV ), which is still pending, as a strong catalyst for further growth going forward. Another mega cap I’m considering is Pfizer (NYSE: PFE ). The company sports a 3.5% yield and also just announced that it was increasing its dividend yet again. In late October the company announced that it would buyback another $11 billion worth of its shares. A couple of other dividend paying names that I am considering adding include Flowers Foods (NYSE: FLO ), Ford (NYSE: F ), and Middlesex Water (NASDAQ: MSEX ). Some Risky Additions in 2015? Although I want to balance my holdings to safer plays that does not mean I won’t add some further risk to it. Over the past two weeks natural gas has been hammered and I see a possible very enticing risk vs. reward opportunity playing natural gas at these levels. This could turn out especially rewarding if we see bitter weather in late January or February. Henry Hub Natural Gas Spot Price data by YCharts Another position I may consider would be one in Twitter (NYSE: TWTR ). In 2015 the company is expected to become consistently profitable after many quarters of losses. The shares are trading 46% down from its 52 week high and the last time the shares were trading around this level they went on a 50% run. A short term catalyst for the shares may be the rumors that current CEO Dick Costolo may be canned. Costolo has lost investor confidence and replacing him could lead to a nice pop in the shares. Conclusion Being so young I can afford to have lots of risk and make mistakes (and learn from them). In 2015 I want to be more cautious and reasonable. Since beginning investing my holdings have always overwhelmingly been dominated by high risk names. To start 2015 I have saved enough to change this and will not only be adding more reliable and safe names, but will also be getting rid of some of the current risky names I hold. In particular I am going to add extremely financially sound companies that also pay dividends which should reward even if 2015 turns sour for the markets. Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks. Additional disclosure: Always do your own research before investing. Keep in mind that everyone, especially by age group, has different investment goals and aims. Most of my investments remain long term but I also dabble in short term trading occasionally. I may initiate long positions in T, PFE, UGAZ, GASL, F, FLO, MSEX, TWTR. Scalper1 News

Scalper1 News