The Emerald Economy

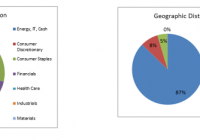

Ireland has the top growth rate in the EU. Ireland has an extraordinarily friendly business environment. EIRL one of the few ways to invest the Irish economy. The approval of the referendums in Northern Ireland and the Republic of Ireland on May 22, 1998 was the culmination of a long and arduous peace process, putting an end to the troubles which had plagued the region for countless decades. Once free of strife, Ireland began to restructure and develop a modern economy. Ireland has been an EU member since 1973 and Eurozone member since 1999. Ireland focused on building a ‘knowledge economy’, attracting foreign investment in technology, services and trade earning it the name ‘Celtic Tiger’. Unfortunately, and not unlike most advanced economies, Ireland suffered a severe banking crisis after the collapse of inflated property and credit markets in 2008. It became necessary for Ireland to apply for over $70 billion in IMF and ECB bailout loans. After years of austerity and restructuring, Ireland became the first Eurozone nation to exit the EU-IMF rescue program in 2013. The Emerald Island’s economy has since recovered to become the fastest growing economies in the EU, measuring a 4.8% pace in 2014 after a mere 0.2% in 2013. To put this in perspective the EU as a whole managed 0.8% GDP growth in 2014. It seems then that there exists a unique opportunity here, for an investor seeking to diversify a portfolio by careful selection of regional economies. Of over 70 ETFs filtered from using the Global/International Equities/Europe filter of the Seeking Alpha ETF Hub , only one specifically focuses on Ireland: the iShares MSCI Ireland Capped ETF (NYSEARCA: EIRL ) . According to the prospectus , its objective is to track the investment results of a broad based index, the MSCI 25/50 Ireland Capped Index, composed of mid, small and large cap Irish equities. The fund is passively managed. The MSCI 25/50 index capping methodology requires that no more than 25% of the fund’s assets are invested in a single issuer and that the sum of the weights of all issuers representing more than 5% of the fund should not exceed 50% of total assets. The fund itself is not large with 25 companies plus a cash position. The largest sector holdings are in Materials and Consumer Staples followed by Industrials and Financials and lastly Health Care and Consumer Discretionary. The combined Energy, IT and cash positions account for only 0.2816% of holdings. The fund is biased towards growth with over 65% of the portfolio invested in cyclic or cyclically sensitive sectors. (click to enlarge) (Data from iShares) Of fund’s ten heaviest weighted sectors, Materials account for about 36%; Industrials for 17%; Financials for 14% and Consumer Discretionary for 6%. This is somewhat offset defensively having Consumer Staples account for 21% and Health Care for 6%. Hence the fund has a strong cyclically sensitive bias among its heaviest weighted components, as well. (Data from iShares) Ireland’s consecutive yearly trade surplus demonstrates the importance of trade to the Emerald economy. Hence, the investor should take note of the major exports as well as major export partners. Ireland is global leader as a supplier of pharmaceuticals. In fact, over 50% of Ireland’s exports are pharmaceuticals, compounds, medical supplies or medical instruments. Ireland’s top trading partners are EU members, with the exception of Switzerland, Japan and the United States. (click to enlarge) In 2013, Forbes ranked Ireland number one in its list of best countries to establish business in out of 145 nations. Ireland’s main global attraction is its 12.5% corporate tax rate, pulling in major US high tech firm such as Google (NASDAQ: GOOG ), Amazon (NASDAQ: AMZN ), eBay (NASDAQ: EBAY ), LinkedIn (NYSE: LNKD ) and Facebook (NASDAQ: FB ). The list is just as impressive for the Pharmaceutical and Bio Tech giants such as Abbot Labs (NYSE: ABT ), Pfizer (NYSE: PFE ), Boston Scientific (NYSE: BSX ), Glaxo-Smith-Kline (NYSE: GSK ) and Allergan (NYSE: AGN ). (click to enlarge) (Data from iShares) The point of the matter is, Ireland’s success in transitioning from a strife torn agricultural economy into a globally leading knowledge economy was the result of sacrifice, compromise and a healthy dose of extremely innovative thinking. The investor should note that Ireland is a small economy, but nimble, thus maintains the ability to adjust, adapt and grow rapidly, as it has already proven with a 4.8% growth rate while global super-economies struggle with quantitative easing, high taxes and ‘new-normal’ growth rates. Hence, it is not unreasonable to conclude that as the US, and EU economies continue to recover over the next several years, it will bode well for the Irish economy. As mentioned, the fund has 25 holdings with net assets totaling $110,957,731 and trades on the NYSE under the symbol EIRL. The fund was launched in May of 2010. Some key facts are summarized in the table of the top ten holdings below: Key Facts: Number of Holdings Outstanding Shares Net Assets 20 Day Average Volume P/E Beta 12 Month Trailing Yield Premium/Discount Expense Ratio 25 2.8 million $110, 957,731 12,463 21.92 1.22 1.59% 1.12% 0.47% Top Ten Holding Summary: Company Sector Dividend Payout Ratio Beta EPS (Est.) P/E (NYSE: TTM ) Price/Cash Flow Market Cap (NYSE: MILL ) CRH ( OTCPK:CRHCF ) Materials 2.32% 79.04 1.46 0.79 34.17 17.63 $24,315 Kerry Group ( OTCPK:KRYAY ) Consumer Staples 0.65% 4.96 0.57 2.73 25.57 20.05 $13,486 Bank of Ireland (NYSE: IRE ) Financial 0.00% 0.00 2.97 0.02 18.56 15.79 $13,251 KingSpan Group ( OTC:KGSPY ) Materials 0.73% 26.03 0.90 0.61 36.52 25.97 $4,347 Glanbia ( OTCPK:GLAPY ) Consumer Staples 0.57% 22.21 0.64 0.49 38.86 28.10 $6,241 Icon (NASDAQ: ICLR ) Health Care 0.00 0.00 0.84 3.07 22.22 16.53 $4,539 Paddy Power ( OTCPK:PDYPD ) Consumer Discretionary 2.06% 51.41 0.35 2.97 27.58 18.72 $3,972 SMURFIT KAPPA GRP ( OTCPK:SMFKY ) Materials 1.98% 37.51 2.01 1.06 26.33 10.53 $7201 RYANAIR (NASDAQ: RYAAY ) Industrials 0.00% 0.00 0.96 3.38 21.74 13.73 $18,496 Grafton Group ( OTCPK:GROUY ) Industrials 1.17% 31.23 1.63 0.34 21.61 15.24 $1886 Averages 0.948% 25.239 0.579 1.233 27.316 18.229 $9773.4 (Data from Reuters) To be sure, there is a risk involved when investing in a smaller country focused ETF which is closely tied in with superpower economies. However, Ireland seems to have been extraordinarily successful at attracting fixed capital investment particularly of global corporate giants. (click to enlarge) (Data from iShares) Lastly, this is a lightly traded ETF, averaging fewer than 12,500 shares per trading session over 20 days. Below is a price chart with dividends. Hence, the iShares MSCI Ireland Capped ETF offers investors one of the few, if not the only way to invest in Ireland’s surprisingly fast growing economy, through a mostly unnoticed ETF. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Additional disclosure: CFDs, spreadbetting and FX can result in losses exceeding your initial deposit. They are not suitable for everyone, so please ensure you understand the risks. Seek independent financial advice if necessary. Nothing in this article should be considered a personal recommendation. It does not account for your personal circumstances or appetite for risk.