Value And Momentum: A Beautiful Combination

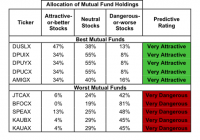

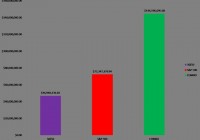

Asset allocation should be a dynamic process. Value-based asset allocation can serve as a long-term investment guide. Momentum can potentially add value by allowing tactical shifts. In our most recent articles, Diversification Is Not Sufficient and Value Based Asset Allocation , we documented two simple strategies for asset allocation. The strategies are based on two seemingly opposed factors, value and momentum. We illustrated in each article the historical results of following each strategy. Empirically, each demonstrated superior results to a static allocation approach. This article illustrates the benefits of combining the two strategies. The value-based asset allocation system (Value Allocator) is a robust enough system on its own to help you navigate the uncertain markets and avoid getting caught in the next crash. The problem is that the system is most likely behaviorally impossible to apply. Using momentum to complement the strategy is an important enhancement that provides participation in further growth and protection in the down markets. The momentum strategy appears to deliver the best results historically. However, we did not examine the impact of transaction costs (most likely negligible) and taxes (significant). We have no way to estimate the tax ramifications of any system as it is obviously only successfully analyzed at the individual level. The momentum-based strategy, because of the short-term gains, is most likely the least tax efficient. Momentum strategies are also difficult to follow year in and year out. Momentum trading does not always resemble the overall stock market. In fact, these types of strategies often look much different from the traditional stock indices like the Dow Jones Industrial or the S&P 500. Since the bottom in 2009, the Barclays CTA Index (a common benchmark for trend following) has been down in every year except for 2010 and 2014. The stock market has not had a negative year since 2008. Again, momentum strategies in isolation are extremely difficult to follow over a long period. In efforts to remain pragmatic, we have combined the value based strategy and a simple momentum strategy to provide a comprehensive asset-allocation system. From this point forward, we will reference the Value Allocator as the strategic component of our asset allocation, and the momentum strategy as our tactical overlay. The combination of the two strategies keeps an investor from moving the entire policy portfolio tactically and keeps a portion in a passive, strategic posture. The strategic component is based on the assumption that markets revert to the average. The problem is that mean reversion occurs over a period of seven to ten years. Valuations tell us very little about what is going to happen over the subsequent one to three years. Our strategic asset allocation process is based on long-term value and contrarian positioning. Tactical asset allocation is the process of taking positions in various investments based on short to intermediate term opportunities. Our tactical overlay is therefore based on reacting to the trend. This is an interesting relationship as the two strategies can offer up diametrically opposed recommendations. For instance, when the US stock market is overvalued, the Value Allocator would recommend rotating to a more conservative portfolio. At the same time, if the trend was positive but the market still overvalued, the tactical overlay would recommend overweighting. You can see the conflicts that can arise, and we assure you they have surfaced in the past. The Value Allocator-as illustrated in Value Based Asset Allocation -can rotate between 30 percent stocks and 70 percent bonds and 70 percent stocks and 30 percent bonds. The tactical portfolio is either 100 percent in stocks or 100 percent in the US 10-year Treasury bonds. The following matrix embodies all possible allocations when the two strategies are combined in equal proportions: Undervalued Market Overvalued Market Positive Trend 85% stocks /15% bonds 65% stocks/35% bonds Negative Trend 35% stocks /65% bonds 15% stocks /85% bonds The investor can have as little as 15 percent in stocks and as much as 85 percent. The wide range allows the investor to adapt to all market conditions, protecting when the odds are poor and growing when the odds favor return enhancement. Instead of fixing the allocation on a static portfolio, investors are allowed the flexibility to adapt their risk tolerance to the current environment. For instance, if the current market environment is undervalued, and the trend is positive, the environment is favorable for stocks. Thus, the investor would be positioned heavily in that asset class. (click to enlarge) The combination of the Value Allocator and momentum strategy outpaced the S&P 500 and fifty-fifty (stocks-bonds) benchmarks by a large degree. The advantage of the combination of these two strategies is quite clear. The worst loss the combination strategy experienced from 1972 to 2014 was 9 percent in 1974 when the market was down almost 26 percent. The Value Allocator, when analyzed in isolation, was down almost 18 percent during that same year. The momentum system added an extra layer of protection when the Value Allocator arrived early to the party. In addition to providing an extra layer of protection, the combination strategy provided growth that would have otherwise been missed during the late 1990s and from 2003 to 2007. The market stayed overvalued from 1990 until the beginning of 2009. If you had followed the Value Allocator during this period, you would have been disappointed. The combination strategy would have minimized the underperformance to the benchmark by keeping you at a higher equity position throughout the 1990s. In the chart depicted below, you can see the market outperform the combination strategy over this period. (click to enlarge) The market outperformance was only temporary, however, as the 50 percent decline from the peak in 2000 was largely avoided. In addition, instead of keeping the allocation conservative from 2003 to 2007, tactical positioning kept investors engaged in the markets. Following the Value Allocator alone from 2003 to 2007 would have had the investors conservatively positioned in 30 percent stocks and 70 percent bonds-largely missing the rebound from the tech wreck. The tactical component of the portfolio would have allowed investors to maintain 65 percent in stocks when the trend was positive, despite the overvalued conditions of the market. Astute investors would most likely diversify their strategic asset allocation with tactical positions. Value and momentum are two of the strongest factors of market returns, and their significance remains rather stable over time. Combining both value and momentum strategies in a disciplined fashion can create desirable investment results. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. Additional disclosure: HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE SHOWN. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL PERFORMANCE RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY ANY PARTICULAR TRADING PROGRAM. PAST RESULTS DO NOT GUARANTEE FUTURE RETURNS. HYPOTHETICAL PERFORMANCE FOR ILLUSTRATION PURPOSES ONLY.