ONEOK: The 2016 Guidance Is Bullish

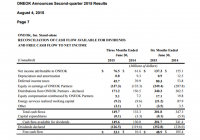

Summary ONEOK surges 15% after providing its 2016 financial guidance. Dividend is expected to be unchanged from 2015 levels. Free cash flow after dividends is expected to be ~$160 million. Though, ONEOK’s success largely depends on its MLP ONEOK Partners doing well. It is truly amazing just how much volatility there is in the midstream sector right now. Formerly steady stocks like ONEOK, Inc (NYSE: OKE ) have been eviscerated, down 44% since early October, following oil lower. Besides falling oil prices, ONEOK has been hurt by the troubles over at Kinder Morgan (NYSE: KMI ) which forced that company to lower its dividend . However, ONEOK recently surprised the markets by announcing plans to sustain its current dividend for 2016. The same holds true for ONEOK’s MLP ONEOK Partners (NYSE: OKS ). This sent shares of both stocks up 15%. Though, despite this news, the yield on both is still elevated at over 11%, indicating continued investor anxiety. OKE data by YCharts 2016 Outlook is looking strong Looking at ONEOK’s updated guidance, it appears not much will change versus 2015. Cash flow available for dividends is expected to come in at $675 million, or $3.22 per share, up 9% from 2015 estimates. Dividend payments are expected at $515 million, or $2.46 per share, flat from 2015 levels, leaving free cash flow of $160 million, or $0.76 per share. This would also result in a robust 1.3x dividend coverage ratio. Though, there is one major weak spot in ONEOK’s guidance–virtually all cash flow is coming from cash distributions from the LP and GP stakes in ONEOK Partners. If ONEOK Partners were to cut the distribution, ONEOK’s cash flows, and thus the dividend, would drop significantly. However, unlike KMI, ONEOK Partners is not relying on the equity markets to fund the capex budget in 2016. Furthermore, the MLP is projecting to fully cover its distribution in 2016. I’ll have more on ONEOK Partner’s 2016 outlook in a future article. The press release is also unclear as to how ONEOK’s free cash flow will be handled. The company noted that: “Free cash flow after dividends and cash on hand totaling approximately $250 million available to support ONEOK Partners” This implies that ONEOK will be contributing cash directly to its MLP. Earlier this year, ONEOK did help out the MLP by buying 21.5 million common units for $650 million. I would not be surprised if another capital infusion from ONEOK to ONEOK Partners is required next year. Though, I would imagine they would want to use something other than ONEOK Partner’s common equity given the high yield and low unit price. Conclusion While the 2016 outlook is undoubtedly good news for ONEOK, investors need to remember that the dividend is not set in stone. If ONEOK Partners fails to cover the distribution, ONEOK’s dividend will be at risk. Nevertheless, it appears things are not as dire for ONEOK as the stock price and 11% yield implies. I believe the stock will eventually recover to a more reasonable level. Though, short to medium term, the price action will likely be dominated by the general trend in oil as the midstream sector’s fundamentals have been ignored by the market. Disclaimer: The opinions in this article are for informational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned. Please do your own due diligence before making any investment decision.