China, Greece And Volatility

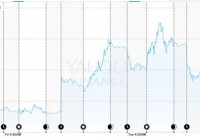

Summary VXX will benefit if backwardation appears long-term. The U.S. is more exposed to China than Greece. Risks to investing in volatility should be assessed. The last few weeks have had Greece front and center in most financial publication headlines. However, is Greece the main focus right now? In this article we will review the performance of the U.S. stock market, some European markets, and the Chinese stock market. To conclude, we will factor how this has and might affect U.S. volatility going forward. The U.S. Market has seen a sharp increase in volatility, which has been historically low. Below is a look at the DAX and FTSE over the same time period. Now, let’s look at the Chinese (and Hong Kong) stock market, again using the same time period. Despite major shocks to global markets, the U.S. market has shown pockets of resilience. Given the current risk, I see the U.S. as a safe haven. Just three months ago you had many touting the emerging markets because growth projections were better than those here at home. They are taking a much larger hit from this than U.S. stocks have. Earnings season is also right around the corner which could provide additional instability if guidance is weak. Assessment This is a classic, here is what we want you to focus on. The media coverage of the Greek drama has far outweighed the plunge in Chinese shares. Only now has China surfaced in headlines. Why? Because Greece is playing nice and is getting boring. Drama sells news, even if that drama isn’t the most important thing to be focusing on. The U.S. has much more exposure to China, than to Greece. Take a look below on the social media data from StockTwits. China doesn’t come close to the amount of interest from Greece. (click to enlarge) Chart created by Nathan Buehler using data from StockTwits.com. Volatility In this article we will focus on the iPath S&P 500 VIX Short-Term Futures ETN (NYSEARCA: VXX ). For two times the leverage you could also use the ProShares Ultra VIX Short-Term Futures ETF (NYSEARCA: UVXY ). VXX invests in second month futures that roll over to the front month and will benefit from backwardation and suffer from contango. For a video on those terms, click here . See below for the current term structure of the VIX. (click to enlarge) Vixcentral.com is my go-to place for futures. However, the website has experienced some problems over the last few weeks with some changes at the CBOE. I would recommend checking the CBOE term structure here if you have any trouble with the above site. Currently futures are in backwardation, which are not reflected on vixcentral, but are reflected on the CBOE link. Contango/Backwardation Despite the recent market rout, futures have struggled to make it to, and maintain positions in backwardation (which benefits VXX). See below: (click to enlarge) Conclusion I continue to believe that Greece will come to a solution with its creditors. A deadline of Sunday (July 12th) has been set to have a permanent agreement in place. Each Monday for the past two weeks has opened down significantly due to weekend events. It is possible that next Monday could be the same. At the end of the week we will hear from Fed chair Janet Yellen and the FOMC meeting minutes will be in focus. China, in my opinion, will level out but still face a lot of volatility. If the plunge continues I would expect some spillover to the U.S. markets. I continue to look for a better opportunity in the VIX futures. For the risk in this environment I would prefer to see a backwardation event from 5-10%, I just don’t know if it will get there. For now, the U.S. economy continues to appear stable and that is my best outlook for the VIX. I have traded in and out of most of my positions in options and the ETFs I mentioned in previous articles. I came out slightly ahead but disappointed in the overall performance. Such is life. I expect China to take center stage if the Greek drama dies down, and vice versa. News channels always need something to talk about. Please take time to assess your risk during periods of uncertainty. I have several articles available on risk assessment. VXX Outlook VXX will benefit from larger periods of backwardation. Backwardation reduces your risk of losses from time value decay. I would be more concerned with a drop off in volatility after this plays out. I have always been one to short volatility after a spike instead of chasing it up the hill. The boulder will eventually roll back down and run you over. I urge you to read up on my previous articles to understand what I am talking about. This is not an article to support buying VXX. I would currently suggest the opposite. I have begun a new volatility blog that will feature options strategies that will complement my Seeking Alpha articles. Check it out here . I also hope to add a personal finance and budgeting section in the near future. As always I appreciate you reading and wish you the best. Disclosure: I/we have no positions in any stocks mentioned, but may initiate a short position in UVXY, VXX over the next 72 hours. (More…) I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.