Ideas For An Ultra-Low Volatility Index Part VII

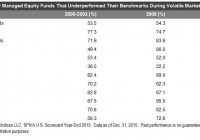

Here are the Ultra-Low Volatility Index strategy’s rules. Buy the PowerShares S&P 500 Low Volatility Portfolio ETF (NYSEARCA: SPLV ) with 80% of the dollar value of the portfolio. Buy the Direxion Daily 30-Year Treasury Bull 3x Shares ETF (NYSEARCA: TMF ) with 20% of the dollar value of the portfolio. Rebalance annually to maintain the 80%/20% dollar value split between the positions. The index is very Zen in its elegance. We are combining the S&P 500 Low Volatility ETF with a 3x leveraged exposure to long duration government bonds, which acts as an imperfect hedge. Because of the leverage inherent in TMF, we can allocate more capital to SPLV. In addition, it is not necessary to have margin exposure. Personally, I think most investors want a portfolio that will tread water, hold its own, and only drop slightly when markets are going crazy. Low drawdowns and ultra-low volatility enable an investor to hang on and to actually enjoy the possibilities of the long term. For too long, people have had the pain theory of investing pounded into their head . Or as I like to call, it “The Bill Ackman School For Kids Who Can’t Read Financial Statements Good And Wanna Learn To Do Other Stuff Good Too.” Many of these “special people” (and let me be clear, by “special” I mean reckless and dumb) believe that in order to enjoy a decent return, that they first must endure the pain of having positions move against them, in order to eventually triumph in a grand quest for the truth of their own genius, against all odds. The pain theory of investing sounds very heroic and glamorous, but in reality, a smooth ride allows investors to hold on to their positions in order to enjoy the benefits of the long term. Why get shaken out, when you can have a smoother ride? And the smoother ride, in this case, has a higher return across a full bull/bear market cycle. Here are the index’s results: (click to enlarge) Click to enlarge (click to enlarge) Click to enlarge I will be the first to admit that this strategy is not brilliant or original. It’s just solid blocking and tackling. The current trend towards complexity in the investment world is not just disturbing – it’s also not profitable. Recent blowups like Pershing Square ( OTCPK:PSHZF ) highlight the importance of protecting investor capital. Unfortunately, many managers have the misguided urge to prove their genius, rather than to make money and to protect investor capital. Remember, it’s not about pretending that you’re always right. It’s about making money. A good investor resists the urge to make it all about his own ego. He makes it about safeguarding investor capital. Like a good doctor, the first directive must be to “first, do no harm.” In future posts, we will examine ways to apply conservative risk control to portfolios in order to hedge or to move to cash during a simultaneous collapse in stocks and bonds. Thanks for reading. We feature even more impressive strategy indices in our subscription service. If this post was useful to you, consider giving it a try. Hypothetical performance results have many inherent limitations, some of which are described below. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown; in fact, there are frequently sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular trading program. One of the limitations of hypothetical performance results is that they are generally prepared with the benefit of hindsight. In addition, hypothetical trading does not involve financial risk, and no hypothetical trading record can completely account for the impact of financial risk of actual trading. For example, the ability to withstand losses or to adhere to a particular trading program in spite of trading losses are material points, which can also adversely affect actual trading results. There are numerous other factors related to the markets in general or to the implementation of any specific trading program, which cannot be fully accounted for in the preparation of hypothetical performance results and all which can adversely affect trading results. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.