Is More Information Making Us Worse Investors?

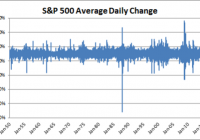

Study after study has shown that retail investors and professional money managers just aren’t very good at investing. And the primary cause of this poor performance is being overly active and incurring lots of unnecessary taxes and fees. The pros can’t control themselves because they have to impress their clients by trying to look active and “beat the market.” And the retail investor is prone to be short term because they know their financial lives are a series of short-term financial events in a long-term life. But an interesting thing appears to be occurring over the course of the last 65 years. Despite a preponderance of information and market access, we seem to be getting no better at investing AND the markets seem to be getting more volatile. If we look at the average daily change in the S&P 500, we can see a slight shift in the variance of the data over time: That’s not very clear, though. If we rearrange that chart, we can construct the average annualized standard deviation of the daily returns: This chart clearly shows that stock market volatility has increased over the last 65 years. There is almost certainly a multitude of causes here, but I don’t think it’s a coincidence that the 1980s and the era of new technology and market access has coincided with the explosion in higher volatility since then. This makes me wonder about two things: What does this say about information theory, economic theory and financial theory? What does this tell us about the current era of investing? What does this say about information theory, economic theory and financial theory? One would think that more information would make the markets behave more “efficiently.” And while we know that professional investors don’t beat the market consistently, we also know that the average holding time on stocks has cratered over the last 70 years, which means that investors, in the aggregate, are paying more in taxes and fees than they previously did. In fact, the average holding period is now consistent with a short-term capital gains rate which means the business of active investing has become a lucrative business for Uncle Sam! This means, by definition, that the post-fee and post-tax return on the aggregate of publicly-held stocks has to be lower than it was in 1940. This would seem to imply that easier access to markets and information has actually made us worse at investing. More information isn’t making us more rational or more efficient. It’s fueling our behavioral biases and short-term tendencies. Access to trading accounts combined with the 24-hour news cycle has become a behavioral nightmare for investors. And yet the vast majority of investors think that all of this information is making them smarter when the data shows that they’re not nearly as financially competent as they think. Contributing to this is all the new technologies. This includes discount brokerage firms, high-frequency trading, leveraged index funds, robo advisors, free trading applications, etc. All of these businesses feed off of our “get rich quick” mentality and/or give us access to markets in an unprecedented manner which fuels our behavioral biases in any number of ways. Further, investors haven’t been compensated for this added volatility. The average 3-year return on the S&P 500 is only marginally higher in the last 25 years than it is over the last 65 years. This shows how futile the idea of “risk” as “standard deviation” really is. In other words, the textbook model of the financial markets hasn’t at all reflected what one might have expected where more information makes markets more efficient, and more volatility compensates investors for what is considered more risk. Basically, modern financial theory doesn’t tell us much about modern financial reality. What Does This Tell us About the Modern Era of Investing? Nothing good. I’ve talked about the difficulty of managing time in one’s portfolio . This intertemporal conundrum is, by a wide margin, the most difficult concept to master in portfolio management. This is the problem of time in an investor’s portfolio. While we know we should be long term, we are inclined to be short term for any number of reasons. Threading that needle and finding the timeframe that makes the most sense for you is incredibly difficult. I’d venture to guess that investors in the 40s probably weren’t far off with their 7-year period. Sadly, what I seem to be finding is that more and more investors are veering in the direction of being ultra short term, hoping to make the quick risk-free buck. And in doing so, they’re falling victim to all of the behavioral biases that are driving this extremely short-term view which necessarily leads to poor performance.