South Jersey Industries’ (SJI) CEO Michael Renna on Q2 2015 Results – Earnings Call Transcript

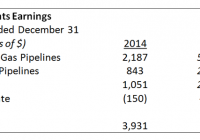

South Jersey Industries Inc. (NYSE: SJI ) Q2 2015 Results Earnings Conference Call August 7, 2015 11 AM ET Executives Ann Anthony – Treasurer Michael Renna – President & Chief Executive Officer Stephen Clark – Senior Vice President & Chief Financial Officer Jeffrey DuBois – Executive Vice President Marissa Travaline – Director Investor Relations Operator Good day, ladies and gentlemen, and welcome to the Q2 2015 South Jersey Industries Earnings Conference Call. My name is Scoda, and I’ll be your operator for today. At this time all participants are in listen-only mode. Later we will conduct a question-and-answer session. [Operator Instructions] I would now like to turn the conference over to your host for today, Ann Anthony, Treasurer. Please proceed. Ann Anthony Thank you. Good morning and welcome to the conference call for SJI’s second quarter fiscal 2015 results. I’m Ann Anthony, Treasurer for South Jersey Industries. And I’m joined today by members of our senior management team, including Mike Renna, President and CEO of SJI; Steve Clark, our CFO; Jeff DuBois, President of South Jersey Gas; and Marissa Travaline, our Director, overseeing Investor Relations. As you may know, we issued a news release this morning announcing the results we will be discussing on the call today. That release includes an in-depth review of earnings on both a GAAP and non-GAAP basis using our non-GAAP measure of Economic Earnings. This measure eliminates all unrealized gains and losses on commodity and on the ineffective portion of interest rate derivative transactions. It also adjusts for realized gains and losses attributed to hedges on inventory transactions and for the impact of transactions or contractual arrangements where the true economic impact will be realized in a future period. The news release is currently available on our website at www.sjindustries.com, in the Newsroom section. Throughout today’s call, we will be making references to future expectations, plans and opportunities for South Jersey Industries. These remarks constitute forward-looking statements for purposes of the Safe Harbor provisions under the Private Securities Litigation Reform Act of 1995. Actual future results may differ materially from those indicated by these statements as a result of various important factors, including those discussed in the company’s Form 10-K on file with the SEC. We assume no duty to update today’s statements should actual events differ from expectations. Also note that our 2014 numbers have been adjusted to reflect the impacts of the stock split that occurred on May 8. With that said, I’d like to turn the call over to our CFO, Steve Clark, to detail our year to date and second quarter 2015 results. Stephen Clark Thank you, Ann, good morning to everyone on the call and thanks for joining us. As we stated in the release, earnings were impacted by a write-down of our investment in cost associated with the central energy facility that previously served the former Revel property in Atlantic City. We’ve discussed on previous calls Revel’s bankruptcy and closing in mid-2014 in a long drawn-out sale process that was completed in April of this year. Since our central energy facility is the logical source of power for the Revel property, we anticipated that our contract provides heating, cooling and power to the facility would be renegotiated to some reduced level with the new owner. Unfortunately, the new owner has shown little to no interest in reopening Revel or striking a deal for energy services. While we remain ready to provide service to Revel, a lack of any recent and meaningful progress toward this new deal awarded the write down we took in the second quarter. This write down reflects our investment in central energy facility of Revel. It does not include the value of our cogeneration equipment located within the facility as we expect to be able to repurpose that equipment to serve better customers. Now, let’s review results. Year to date, economic earnings totaled $60.8 million. Excluding the year to date Revel related write down of $11.1 million, operating results would have reflected economic earnings of $71.9 million for the first half of 2015, as compared with $76.2 million for the first half of 2014.The remaining variance between These year over year periods largely reflects the significant contribution to economic earnings from our wholesale gas marketing business in the first quarter of 2014, which directly resulted from the Polar Vortex we experienced in the early part of the year. The variance also reflects a reduction in investment tax credits from solar development. First the second quarter, economic earnings totaled $1.9 million in 2015. Excluding the write down of $10.9 million for the quarter, operating results would have reflected economic earnings of $12.8 million as compared with $10 million in the second quarter of 2014. The biggest drivers of the quarterly improvement in operating results between 2014 and 2015 are contributions from our utility due to infrastructure investment and customer growth, as well as significantly improved performance from our wholesale commodity business. Actual economic earnings per share through June 30, 2015 were $0.89 as compared with $1.16 for the first six months of 2014. For the quarter, economic EPS totaled $0.03 as compared with $0.15 in the prior year period. Excluding the impact of the thermal facility write down, 2015 economic earnings per share would have totaled $0.19 for the year to date and $1.05 for the second quarter. Now, I will detail the results of specific areas of our business, noting those business lines or segments where the write down had a major impact on economic earnings. Within the utilities, South Jersey Gas’ net income for the first half of 2015 was up 15% at $47.8 million as compared with $41.5 million for the first half of 2014. For the quarter, utility net income was $5.2 million, significant increase over the second quarter of 2014 contribution of $3.8 million. This improvement reflects the benefits of last year’s rate case, our accelerated infrastructure programs and customer additions. Infrastructure investments under our accelerated programs totaled $28.7 million year-to-date and added an incremental $1.7 million of net income for the first half of 2015. With planned investments of nearly $65 million for 2015, our AIRP and SHARP programs will continue to reinforce our system for the replacement of bare steel and cast-iron gas main and the replacement of low pressure gas main with high pressure main along barrier islands. Also worth noting, we are moving forward again in our pipeline project to provide natural gas to the BL England electric generation station and enhance service reliability to customers in the southernmost portions of our operating territory. In May, South Jersey Gas filed an amendment to our 2013 project application still pending with the New Jersey Pinelands Commission. The amended application highlights the enhanced reliability and environmental benefits this project will provide customers across the region. We remain optimistic of the compelling benefits of this project to all residents in Southern New Jersey or ultimately result in its successful completion. Customer growth continues to be significant, up over 6,400 customers [or 1.8%] for the 12 month period ending June 30, 2015. On an annualized basis, these customers will be worth approximately $1.7 million of net income in future years. Our growth continues to benefit from strong conversion activity with nearly 2,800 new customers coming from conversions during the first half of 2015 and a target of 6,500 for the full year. I do want to point out that the collection of deferred gas cost from the winter of 2014 combined with the extremely cold winter this past year has resulted in high receivable balances as of the end of June, which in turn have resulted in higher receivable reserves of the utility. We boosted reserves by roughly $800,000 for the quarter or $500,000 after tax, reflect a situation that we will continue to monitor closely. Now, I’ll move over to the non-utility side of our business and discuss results from South Jersey Energy Services and South Jersey Energy Group. Energy Services largely reflects our energy production assets within Marina Energy and our energy project joint venture Energenic. Energy Group reflects our wholesale gas and retail gas and electric commodity business activities. The first six months of 2015, these non-utility businesses contributed a combined $13 million as compared with $34.7 million in 2014. Year over year variance stems from two major events, first being the previously noted write down of our central energy facility assets, second is the non-recurring benefit to our wholesale business realized from the Polar Vortex in the winter of 2014 that drove gas volatility and ultimately net income in the first quarter of that year. Reduction in solar ITC also played a smaller role in the year over year decline. In the second quarter of 2015, our non-utility businesses reflected a loss of $3.3 million as compared with economic earnings of $6.2 million in the prior year period. We will take a look at the other drivers of these results as I detail each of the business lines. Beginning with South Jersey Energy Services, this part of our business directly absorb the full write down noted previously. However, for the purpose of comparing operating results in the context of this discussion, I think it is more meaningful to [prevent] economic earnings that exclude the impacts of the write down, which amounted to $11.1 million for the first half of the year and $10.9 million for the second quarter. With this in mind, economic earnings for the first half of 2015 for South Jersey Energy Services, excluding the write down, were $15.7 million as compared with $20.8 million for the same period in 2014. For the quarter, results were $6.9 million as compared with $10.1 million for the second quarter of 2014. Lower levels of ITC recorded for both the 2015 year to date and second quarter periods accounted for the majority of the variance. First quarter 2014 Polar Vortex related performance in our wholesale gas marketing business and 2014 earnings from our energy facilities serving Revel were obviously not repeated. Excluding the impact of the write down, operating performance from our CHP business line reflected economic earnings of $2.6 million per year to date, as compared with economic earnings of $4.9 million in the first half of 2014. For the quarter, operating performance for this business produced economic earnings of $300,000 as compared with $1.5 million in the second quarter of 2014. In addition to legal costs incurred and income loss from operations at Revel, 2015 did not see a repeat of the benefits incurred from optimizing these assets, here I’m specifically talking about the energy production assets, around extreme gas price volatility that existed during the winter of 2014. Going forward, we expect our operating projects to be steady and positive contributors to economic earnings. Turning to renewables, our solar operating performance improved by nearly $400,000 year over year. This is reflected in our year to date solar economic earnings of $15.1 million, which included investment tax credits of $17.3 million as compared with the prior year economic earnings of $17.5 million, which contained ITC of $20.1 million. For the second quarter, solar contributed $7.2 million, including $7.1 million of ITC, as compared with $9.8 million that included $9.6 million of ITC in the prior year period. The increase in 2015 solar energy production, particularly in the second quarter, has not yet been fully recognized in earnings due to the timing of certification of renewable energy certificates, particularly as it relates to Massachusetts. That certification process can take up to six months. We expect to see those benefits in the second half of this year. We do expect to see improved operating performance through year end. We remain on track for full year SREC production of 135,000 SRECs. SREC values in New Jersey continue to strengthen, spot market price is now around $237. We also remain very active in the Massachusetts market, where SREC spot market values are closer to $465. For the first half of 2015, our landfills produced a loss totaling $2.3 million as compared with a loss of $2.2 million in the prior year period. However, the second quarter saw operating performance improve their reduced loss of $900,000 in 2015 as compared to a loss of $1.3 million for the second quarter of 2014. We remain optimistic that the operational initiatives implemented over the last two quarters will help drive continuing improvement for these projects. Turning to South Jersey Energy Group, the commodity segment of our business, the first half of the year reflected solid performance with economic earnings totaling $8.5 million as compared with $13.9 million for the first half of 2014. These results reflect a benefit price volatility associated with the 2014 Polar Vortex. As we told you to expect on previous calls, performance for this business improved significantly in the second quarter. This segment contributed $671,000 as compared to a loss of $4.3 million in the second quarter of 2014. With the declining drag from what’s profitable legacy marketing contracts that began rolling off at the end of March and the contributions from the two fuel management contracts that are currently active and with another pending to commence later this year, we expect continued improvements from this business throughout 2015. Finally, taking a look at the balance sheet, our equity-to-cap ratio was 43% at the end of the second quarter, as compared to 44% in the second quarter of 2014. We use our dividend reinvestment plan to issue equity and we’ll continue to do so in 2015 in support of our significant capital programs. We also [indiscernible] $300 million of deferred tax benefits related to our investments that we expect to realize between now and 2020 that will support our goal of delivering – delevering the balance sheet. At this time, I’ll turn the call over to Mike to discuss the forward view for our business. Michael Renna Thanks, Steve. Good morning. As Steve highlighted in his comments, the write down of our investment in the energy facilities serving Revel mitigated much of the positive performance for the quarter. I think most of the detail around that transaction is already been articulated here today, as well as within our earnings release and 10-Q filing. The one think I’d like to add is that we’re encouraged by what we see happening in Atlantic City, we look forward to the day when the former Revel property, part of the City’s broader success, but ultimately we decided that the best thing for our company is to look forward. Doing so will allow us to fully focus on strengthening the business lines that are the foundation of our growth. Businesses, that after backing out the impact of Revel, actually supported economic earnings per share growth 4% to 8% in 2015. In an emphasis on earnings quality, we look forward to continued strong performance in our utility, increase contributions from our commodity businesses, stable performance from our operating energy production assets. As we move forward, we do so with a model that emphasizes our regulated businesses and those areas of our non-regulated business. We have a demonstrated ability to compete and succeed. Most importantly, we will remain confident in our ability to deliver economic earnings of $150 million by 2020. I think focusing on earnings from operations provides a meaningful year over year comparison performance, while also highlighting the strong potential for our business overall. Year to date performance of our utility highlights the potential of South Jersey Gas, increase its contribution to SJI earnings from roughly 60% to 65% to upwards of 70% to 75% as we approach 2020. Significant customer growth fuelled by the compelling economics of natural gas as the heating fuel, we expect to add an incremental $11.8 million by 2020. Accelerated utility infrastructure investment is projected at nearly $350 million over the next five years, adding roughly $18 million in incremental net income by 2020. These initiatives combined with the benefits from new CNG infrastructure, the development of a reliability pipeline to serve BL England, construction of a liquefier at our Nat LNG storage site and a future rate case position our utility for an incremental net income contribution of roughly $13 million again by 2020. On the non-regulated side, strong margins in our commodity business, commencement of at least five new fuel management contracts and improving operating performance across our energy production assets support earnings contributions of $30 million to $40 million by 2020. Most importantly, this growth is targeted without reliance on investment tax credits from renewable projects, coming instead from expanded and improved performance across our core businesses. Finally, we expect our investment in the Penn East pipeline to contribute at least 10% of total net income by 2018. This fully subscribed pipeline is being driven by [climates] of more than 800,000 decatherms from regional utilities and utility affiliates, and is expected to be in service by late 2017. While there is certainly vocal opposition to some pipelines, including Penn East, we expect the overwhelming benefit will provide the region to ultimately overcome the opposition. Before we conclude, I’d like to highlight strategic priorities we shared during the second quarter’s AGA conference. As we work toward our goal of achieving $150 million in economic earnings by 2020, we’re committed to strengthening our balance sheet, maintaining a lot to moderate risk profile, perhaps most importantly improving quality of earnings to ensure that the foundation of our business is built on regulated, repeatable, and reliable income streams. Thank you. Now, I’ll turn the call back to the operator for Q&A.