Normal Doesn’t Exist

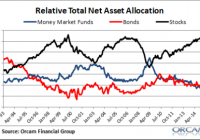

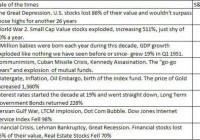

By Andy Hyer Michael Batnick on “waiting for normal:” These are not normal times investors are living in. The Fed has held short-term interest rates at zero for six years now, a policy experiment never seen before. This has many investors eager to see what happens if and when this returns to “normal.” One of the biggest psychological challenges of investing is that there is always something out of the norm. Take a look at the table below which highlights different times investors had to live through and the extreme performances that accompanied them. I wonder at what point would somebody would have described the times as normal. Next, have a look at the chart below, which shows the S&P 500 return by decade. You’ll notice absolutely no pattern. Understanding how different it always is should be a great reminder why no strategy will work in all market environments. Knowing the limitations to what you are doing- whatever you’re doing- is critical. The ability to stick with your plan during the bad times will determine if you’ll be around for the good ones. So what is an investor to do? I see a couple options: Employ some form of static asset allocation and hope for the best. 25% fixed income, 25% US equity, 25% international equity, and 25% alternatives, and rebalance annually. Employ some type of forecasting to try to be opportunistic in asset class exposure Employ some form of trend-following tactical approach to asset allocation The static allocation approach may ultimately perform okay over long periods of time, but will investors have the risk tolerance to continue with long stretches of an asset class being out of favor / going through severe drawdowns? Maybe. Maybe not. Chances are the forecasting approach will end very badly, as forecasting usually does. The third option makes much more sense to me. Simply systematically deal with trends as they unfold. This is the approach we use with our Global Macro separately managed account, which happens to be our most popular SMA strategy. Thank goodness we gave ourselves as much flexibility as we did with the way that this portfolio is constructed, because this decade has been entirely different from the last one. As one example, consider how well commodities performed in the last decade, compared to the trainwreck that they have been so far this decade. Normal doesn’t exist. A disciplined way to be flexible is the key to successfully navigating the ever-changing financial landscape. The relative strength strategy is NOT a guarantee. There may be times where all investments and strategies are unfavorable and depreciate in value. Share this article with a colleague