IPO Market Freeze In Q1 Hit Lowest Point Since Great Recession

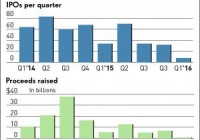

A chill that hit the IPO market in December turned into an all-out freeze in the first quarter, with the number of initial public offerings hitting a low not seen since the Great Recession of 2007-09. Just eight IPOs got out the door in Q1, down 76% from 34 in Q1 2015. That was the fewest IPOs since Q1 2009, which had just one. The $700 million in proceeds raised was the lowest total in 20 years, down 87% from the $5.5 billion raised in Q1 2015, according to Renaissance Capital, which manages two IPO-focused exchange traded funds . All eight IPOs were in the medical sector, and most of those only happened thanks to substantial buying of shares by existing shareholders and a reduction in the initial asking prices. Insider buying accounted for 67% of shares sold in the IPO of Editas Medicine ( EDIT ), and 48% at Corvus Pharmaceuticals ( CRVS ), for example. Recent trends provide hope that the IPO window will reopen in the second quarter, though the big names expected to be waiting for an opening — companies such as Uber and Snapchat — have been quiet on the IPO front. “While the IPO market has been frozen, we know it will open up again,” said Kathleen Smith, principal at Renaissance Capital. “There’s a buildup of companies waiting for the appropriate time to raise capital.” The primary cause of IPO droughts has always been weakness in the stock market. Markets started tanking in late December and bottomed in mid-February. The uptrend in market indexes could ease jitters and bring institutional investors — and companies — back to the IPO table. The IPO rebound will likely proceed slowly at first, as it did in 2009, Smith says, but she see signs some IPO icebreakers could hit the market in April or May. Companies that could debut include US Foods, the second-largest food-service distributor, which submitted an IPO filing in early February that could raise up to $1 billion. Another is MGM Growth Properties, a real-estate investment trust backed by MGM Resorts ( MGM ) that also could raise up to $1 billion, Renaissance estimates. But there’s no sign yet that any high-profile names will come forward soon to spark a heat wave. This week, Uber CEO Travis Kalanick said the ride-hailing company would wait as long as possible before coming public. It’s among a large number of private companies that have raised hundreds of millions, in some cases billions, of dollars, with estimated market valuations well above $1 billion. An IPO is about the only route for investors in those privately held companies to get a healthy return from those investments. The IPO chill has been worsened by the sickly performance of last year’s high-profile new offerings. Among them was Fitbit ( FIT ), the maker of wearable fitness devices. Fitbit had a heart-pounding start, with the stock jumping 48% on its first trading day June 18, pricing at 20 and closing above 29. Fitbit stock peaked at 51.90 in August, but now trades near 13. Box ( BOX ), the online storage service provider, had a similar story. It popped 66% on the first trading in January and closed at 24.73 on day one, which is still its peak. Box now trades near 12.50. Among all IPOs of 2015, their stocks are down 18% on average from their IPO price and down 28% after the first trading day, Renaissance says. The firm says the ultimate pace of the 2016 IPO market remains tough to call, yet it does expect some eye-catching IPOs to launch and deliver attractive returns to investors. Image provided by Shutterstock .