Scalper1 News

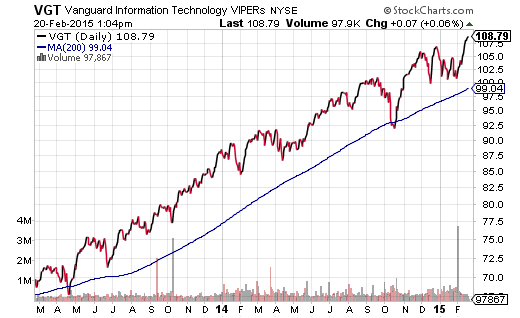

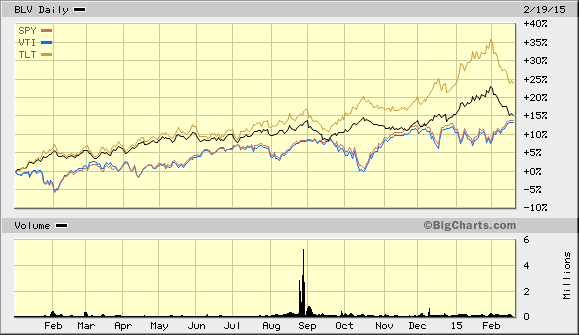

February has been a terrible month for the U.S. economy, but a wonderful month for U.S. stocks. Perhaps ironically, even as an institutional investor, I am not finding myself particularly bearish. On the contrary. I see opportunity to continue riding severely overvalued market-based securities higher. February has been a terrible month for the U.S. economy, but a wonderful month for U.S. stocks. Translation? Investors do not believe that the Federal Reserve will raise overnight lending rates during an economic slowdown. Just how abysmal have the data been so far? Personal spending, construction spending, factory orders, international trade, business inventories, wholesale inventories, consumer sentiment, retail sales and housing starts are just a few of the data points that fell short of expectations. Heck, the Citi Economic Surprise Index recently demonstrated that data points have missed analyst forecasts by the most in more than two years. Most blame the weakening U.S. situation on decelerating activity around the globe. Goldman Sachs has gone so far as to say that the global economy has entered a contraction phase, with six of its seven Global Leading Indicator (GLI) components worsening in February. The lone holdout? U.S. Initial Jobless Claims. Indeed, a low level of unemployment filings coupled with a consistent string of 200,000-plus net new jobs are the positives on the domestic scene. Yet even here, the employment rate as defined by labor force participation is under 63% – percentages that are typically associated with the 1970s. If millions upon millions of working-aged individuals did not give up the search for employment or “retire” since 1/1/2009, back when 66% of working-aged people had jobs, headline unemployment in the U.S. would be above 10.0%. (Naturally, 5.7% unemployment sounds better for those who want to believe that circumstances are much rosier than they really are.) Without question, the U.S. is not an island of self-sustaining expansion. As much as the media portray oil price declines as a windfall for stateside consumers, the slump across the entire commodity space (e.g., metals, agriculture, gas, etc.) communicates anemic demand. Equally troubling, none of the spectacular job gains have translated into significant wage growth in a way that price pressures might rise. (For what it is worth, Wal-Mart (NYSE: WMT ) did raise its wages above Federally mandated minimums for all of its low-earning employees.) Worse yet, depreciating currencies against the U.S. dollar have adversely affected the trade balance such that the Fed acknowledged the dollar’s rapid rise as a “persistent source of restraint” on exports. The Fed is not the only group that has expressed concern about dollar strength. Corporations have blamed the dollar for missing earnings targets, as well as used the currency to guide future earnings projections lower. And analysts have dramatically scaled back profit-per-share outlooks for the S&P 500 from nearly 8%-10% in November to 0%-2% here in February. What do lower earnings projections mean? In essence, the Forward 12-month P/E was the last remaining valuation technique that supported the reasonableness of the current price people are paying for the S&P 500. Not anymore. Cyclical, trailing 12-month and forward 12-month price-to earnings (P/E), price-to-sales (P/S), price-to-book (P/B) and price-to-cash flow (P/CF) all suggest S&P 500 overvaluation. In spite of the seemingly obvious concerns investors should have about U.S. equities, bearish sentiment in the American Association of Individual Investors (AAII) is at a meager 17.88%. According to Bespoke Research, there have been only five weeks of the last 300 where bearish sentiment was lower. Perhaps ironically, even as an institutional investor, I am not finding myself particularly bearish. On the contrary. I see opportunity to continue riding severely overvalued market-based securities higher; that is, there’s no reason to exit the central bank stimulus bubble when the world’s investors have so much faith in their policies. Overvaluation can beget irrational exuberance, and irrational exuberance can beget insane euphoria. It can go on for weeks, months or years. The only caveat? You have to realize the reality that asset prices have gone rogue, and that you will need an insurance plan for reducing risk when the inevitable blow-up transpires. My approach is threefold. First, hold the stock assets that continue to trend higher. Each needs to remain above a a significant trendline like a 200-day moving average; a downside breach should not last more than a couple of days. Some of my favorites? The Vanguard Dividend Appreciation ETF (NYSEARCA: VIG ), the Vanguard Mega Cap Growth ETF (NYSEARCA: MGK ), the Health Care Select Sect SPDR ETF (NYSEARCA: XLV ) and the Vanguard Information Technology ETF (NYSEARCA: VGT ). Additionally, add exposure to assets where you see value, as I have with the iShares Currency Hedged MSCI Germany ETF (NYSEARCA: HEWG ), or add exposure to where you’ve witnessed momentum, as I have with the PureFunds ISE Cyber Security ETF (NYSEARCA: HACK ). Second, recognize that the appeal of long-term U.S. bonds will not dissipate in a weakening global economy. Fits and starts? Sure. Yet long-term U.S treasury proxies yield more than comparable sovereign debt abroad. Buying the bond dips can be as lucrative as buying stocks when they pull back. What’s more, funds like the iShares 20+ Year Treasury Bond ETF (NYSEARCA: TLT ) and the Vanguard Long-Term Bond ETF (NYSEARCA: BLV ) have made more money over the last 15 months than ETFs like the SPDR S&P 500 Trust ETF (NYSEARCA: SPY ) or the Vanguard Total Stock Market ETF (NYSEARCA: VTI ). (Note: Readers know that I have been advocating exposure to longer-term maturities since December of 2013.) Third, there are a wide variety of things that could derail the respective rallies in stocks and bonds. Policy mistakes by one or more of the major central banks around the globe could cause an exodus. A monumental shift toward global acceleration in the worldwide economy would likely catch investors off guard. A decline in oil prices below the current line in the sand at $45 per barrel could cause hardship and/or civil unrest in export-dependent countries. A less-than-graceful exit from the eurozone by Greece (at some point in 2014) could affect the investing landscape. Even an unforeseen event(s) could take market-based securities for a ride where the price declines lead to bearish panic rather than bullish dip-buying opportunity. Disclosure: Gary Gordon, MS, CFP is the president of Pacific Park Financial, Inc., a Registered Investment Adviser with the SEC. Gary Gordon, Pacific Park Financial, Inc, and/or its clients may hold positions in the ETFs, mutual funds, and/or any investment asset mentioned above. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell or hold securities. At times, issuers of exchange-traded products compensate Pacific Park Financial, Inc. or its subsidiaries for advertising at the ETF Expert web site. ETF Expert content is created independently of any advertising relationships. Scalper1 News

February has been a terrible month for the U.S. economy, but a wonderful month for U.S. stocks. Perhaps ironically, even as an institutional investor, I am not finding myself particularly bearish. On the contrary. I see opportunity to continue riding severely overvalued market-based securities higher. February has been a terrible month for the U.S. economy, but a wonderful month for U.S. stocks. Translation? Investors do not believe that the Federal Reserve will raise overnight lending rates during an economic slowdown. Just how abysmal have the data been so far? Personal spending, construction spending, factory orders, international trade, business inventories, wholesale inventories, consumer sentiment, retail sales and housing starts are just a few of the data points that fell short of expectations. Heck, the Citi Economic Surprise Index recently demonstrated that data points have missed analyst forecasts by the most in more than two years. Most blame the weakening U.S. situation on decelerating activity around the globe. Goldman Sachs has gone so far as to say that the global economy has entered a contraction phase, with six of its seven Global Leading Indicator (GLI) components worsening in February. The lone holdout? U.S. Initial Jobless Claims. Indeed, a low level of unemployment filings coupled with a consistent string of 200,000-plus net new jobs are the positives on the domestic scene. Yet even here, the employment rate as defined by labor force participation is under 63% – percentages that are typically associated with the 1970s. If millions upon millions of working-aged individuals did not give up the search for employment or “retire” since 1/1/2009, back when 66% of working-aged people had jobs, headline unemployment in the U.S. would be above 10.0%. (Naturally, 5.7% unemployment sounds better for those who want to believe that circumstances are much rosier than they really are.) Without question, the U.S. is not an island of self-sustaining expansion. As much as the media portray oil price declines as a windfall for stateside consumers, the slump across the entire commodity space (e.g., metals, agriculture, gas, etc.) communicates anemic demand. Equally troubling, none of the spectacular job gains have translated into significant wage growth in a way that price pressures might rise. (For what it is worth, Wal-Mart (NYSE: WMT ) did raise its wages above Federally mandated minimums for all of its low-earning employees.) Worse yet, depreciating currencies against the U.S. dollar have adversely affected the trade balance such that the Fed acknowledged the dollar’s rapid rise as a “persistent source of restraint” on exports. The Fed is not the only group that has expressed concern about dollar strength. Corporations have blamed the dollar for missing earnings targets, as well as used the currency to guide future earnings projections lower. And analysts have dramatically scaled back profit-per-share outlooks for the S&P 500 from nearly 8%-10% in November to 0%-2% here in February. What do lower earnings projections mean? In essence, the Forward 12-month P/E was the last remaining valuation technique that supported the reasonableness of the current price people are paying for the S&P 500. Not anymore. Cyclical, trailing 12-month and forward 12-month price-to earnings (P/E), price-to-sales (P/S), price-to-book (P/B) and price-to-cash flow (P/CF) all suggest S&P 500 overvaluation. In spite of the seemingly obvious concerns investors should have about U.S. equities, bearish sentiment in the American Association of Individual Investors (AAII) is at a meager 17.88%. According to Bespoke Research, there have been only five weeks of the last 300 where bearish sentiment was lower. Perhaps ironically, even as an institutional investor, I am not finding myself particularly bearish. On the contrary. I see opportunity to continue riding severely overvalued market-based securities higher; that is, there’s no reason to exit the central bank stimulus bubble when the world’s investors have so much faith in their policies. Overvaluation can beget irrational exuberance, and irrational exuberance can beget insane euphoria. It can go on for weeks, months or years. The only caveat? You have to realize the reality that asset prices have gone rogue, and that you will need an insurance plan for reducing risk when the inevitable blow-up transpires. My approach is threefold. First, hold the stock assets that continue to trend higher. Each needs to remain above a a significant trendline like a 200-day moving average; a downside breach should not last more than a couple of days. Some of my favorites? The Vanguard Dividend Appreciation ETF (NYSEARCA: VIG ), the Vanguard Mega Cap Growth ETF (NYSEARCA: MGK ), the Health Care Select Sect SPDR ETF (NYSEARCA: XLV ) and the Vanguard Information Technology ETF (NYSEARCA: VGT ). Additionally, add exposure to assets where you see value, as I have with the iShares Currency Hedged MSCI Germany ETF (NYSEARCA: HEWG ), or add exposure to where you’ve witnessed momentum, as I have with the PureFunds ISE Cyber Security ETF (NYSEARCA: HACK ). Second, recognize that the appeal of long-term U.S. bonds will not dissipate in a weakening global economy. Fits and starts? Sure. Yet long-term U.S treasury proxies yield more than comparable sovereign debt abroad. Buying the bond dips can be as lucrative as buying stocks when they pull back. What’s more, funds like the iShares 20+ Year Treasury Bond ETF (NYSEARCA: TLT ) and the Vanguard Long-Term Bond ETF (NYSEARCA: BLV ) have made more money over the last 15 months than ETFs like the SPDR S&P 500 Trust ETF (NYSEARCA: SPY ) or the Vanguard Total Stock Market ETF (NYSEARCA: VTI ). (Note: Readers know that I have been advocating exposure to longer-term maturities since December of 2013.) Third, there are a wide variety of things that could derail the respective rallies in stocks and bonds. Policy mistakes by one or more of the major central banks around the globe could cause an exodus. A monumental shift toward global acceleration in the worldwide economy would likely catch investors off guard. A decline in oil prices below the current line in the sand at $45 per barrel could cause hardship and/or civil unrest in export-dependent countries. A less-than-graceful exit from the eurozone by Greece (at some point in 2014) could affect the investing landscape. Even an unforeseen event(s) could take market-based securities for a ride where the price declines lead to bearish panic rather than bullish dip-buying opportunity. Disclosure: Gary Gordon, MS, CFP is the president of Pacific Park Financial, Inc., a Registered Investment Adviser with the SEC. Gary Gordon, Pacific Park Financial, Inc, and/or its clients may hold positions in the ETFs, mutual funds, and/or any investment asset mentioned above. The commentary does not constitute individualized investment advice. The opinions offered herein are not personalized recommendations to buy, sell or hold securities. At times, issuers of exchange-traded products compensate Pacific Park Financial, Inc. or its subsidiaries for advertising at the ETF Expert web site. ETF Expert content is created independently of any advertising relationships. Scalper1 News

Scalper1 News